Specialty Minerals Sector Pivots to EV and Semiconductor Materials as Regional Monopolies Command 36% Margins in FY2025

Date : 2026-04-11

Reading : 180

In FY2025, global mineral conglomerates (Imerys, MTI) and regional extraction leaders (US Lime, Taekyung BK) executed a severe strategic divergence to combat industrial stagnation and regulatory tightening. Driven by the structural atrophy of graphic paper and coal-fired utilities, multinational players deployed massive CAPEX into EV battery chains and PFAS remediation across Asia and Europe. Simultaneously, hyper-regional operators weaponized strict zoning laws and logistical constraints to capture unprecedented pricing power, with U.S. infrastructure demand propelling localized net margins to near-monopoly levels of 36%.

Financial Health & Operational Moats: The Unit Economics Divide

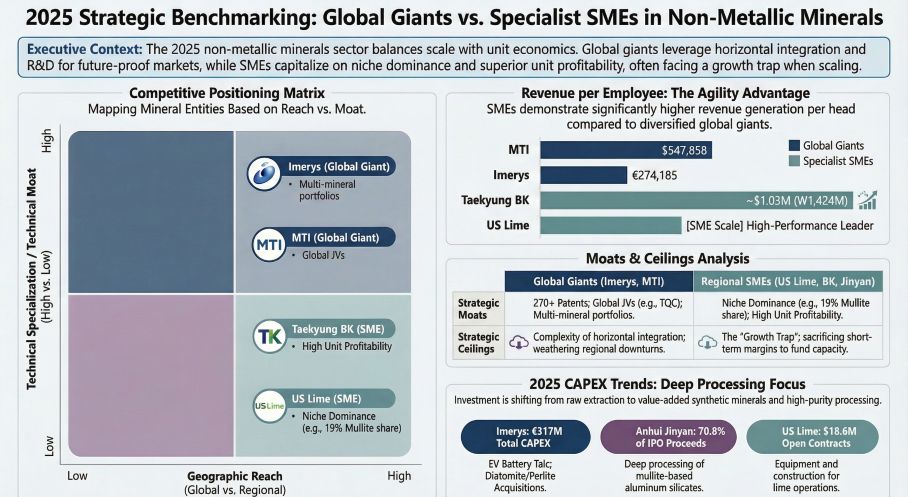

An analysis of FY2025 audit data exposes a definitive dichotomy between the burden of global scale and the extreme efficiency of localized asset moats. While global giants maintain aggregate market leadership, heavily concentrated regional players are demonstrating vastly superior unit economics.

United States Lime & Minerals (NASDAQ: USLM) posted an exceptional $1.077 million in revenue per employee alongside an anomalous 36.0% net margin. This profitability is not derived from advanced material science, but from a heavily fortified geographic moat. Strict EPA NESHAPs regulations and severe zoning restrictions virtually eliminate new entrants, while freight economics lock customers into a 400-mile delivery radius. Armed with zero debt and a $371.1 million cash buffer, USLM successfully utilized raw cost-pass-through mechanisms to extract a 5.6% average selling price increase, driven heavily by runaway data center construction.

Conversely, scale dilutes per-capita productivity for the multinationals. Imerys’ Solutions for Refractory, Abrasives & Construction (RAC) segment generated roughly $354,000 per employee—one-third of USLM’s output—reflecting the operational drag of managing 38 industrial sites across 15 countries. Meanwhile, Minerals Technologies Inc. (MTI) suffered a steep drop into unprofitability, posting an $18.4 million net loss. Despite MTI’s formidable structural lock-in via 10-to-15-year evergreen satellite Precipitated Calcium Carbonate (PCC) plant contracts, the firm suffered from temporary margin compression due to the contractual "time lag" between absorbing inflated energy costs and triggering price adjustments.

Mid-cap players faced an entirely different reality: the "growth trap." Anhui Jinyan Kaolin (HKEX) saw its net margin compress to 14.3% in 2025. This contraction was driven by unabsorbed fixed costs from its new 40,000-ton refractory mullite capacity expansion and tactical price reductions aimed at raw market penetration.

Figure Global Giants vs Specialist SMEs in Non-Metallic Minerals

Supply Chain Pivot: Retreating from Legacy Industrial Cycles

Supply Chain Pivot: Retreating from Legacy Industrial Cycles

Corporate capital allocation in 2025 signals a permanent retreat from historically stable sectors now facing terminal decline—specifically premium graphic paper and coal-fired flue gas desulfurization.

Global leaders are aggressively realigning CAPEX to serve the green mobility and semiconductor megatrends. Imerys executed a $192.2 million (€170 million) capital injection into high-purity carbon black and synthetic graphite for lithium-ion anodes, supplemented by a $48.6 million (€43 million) targeted expansion in Mainland China for automotive polymer lightweighting. Having fully divested its cyclical paper assets in 2024 to avoid inventory de-stocking risks, Imerys is successfully decoupling from legacy industrial drag.

MTI is orchestrating a similar pivot. Bypassing the shrinking paper filler market, MTI drove its Environmental & Infrastructure line to $270.2 million in revenue, leaning heavily into its FLUORO-SORB technology for high-margin PFAS water remediation.

Regional players lacking internal R&D bandwidth are leaning into debt-leveraged vertical integration. Taekyung BK utilized a $50.6 million (KRW 72.0 billion) facility loan for the accretive acquisition of Lion Chemtech, bypassing organic material development entirely to capture immediate downstream market share in artificial marble and synthetic wax.

HDIN Institutional Perspective: Regulatory Ceilings and Peak Divergence

The "dig-and-ship" commodity model is obsolete. HDIN Research assesses that high-grade geological endowment (e.g., USLM's >80-year Life of Mine at Love Hollow) is merely a prerequisite; proprietary thermal/chemical processing and regulatory arbitrage are the true margin multipliers.

Macroeconomic "ceilings"—most notably the EU Carbon Border Adjustment Mechanism (CBAM) and shifting U.S. tariff structures—are actively penalizing unhedged, carbon-intensive operators. Imerys demonstrated best-in-class risk mitigation, utilizing $221.6 million (€196.0 million) in nominal forward energy hedges to insulate its thermal operations, allowing its Graphite & Carbon segment to expand adjusted EBITDA margins by 5.4 percentage points.

However, systemic forensic risks are emerging among heavily regionalized Asian SMEs. We note significant deterioration in Accounts Receivable (AR) quality for Taekyung BK, whose Expected Credit Loss (ECL) rate spiked to 2.9% alongside heavy reliance on $18.38 million (KRW 26.12 billion) in related-party transactions. Investors must heavily scrutinize regional operators that lack the geographic diversification to absorb localized macroeconomic shocks, as these entities are structurally vulnerable to legacy capacity overhangs.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in raw corporate filing synthesis, forensic accounting, and macroeconomic supply chain analysis. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Unit Economics Divide

An analysis of FY2025 audit data exposes a definitive dichotomy between the burden of global scale and the extreme efficiency of localized asset moats. While global giants maintain aggregate market leadership, heavily concentrated regional players are demonstrating vastly superior unit economics.

United States Lime & Minerals (NASDAQ: USLM) posted an exceptional $1.077 million in revenue per employee alongside an anomalous 36.0% net margin. This profitability is not derived from advanced material science, but from a heavily fortified geographic moat. Strict EPA NESHAPs regulations and severe zoning restrictions virtually eliminate new entrants, while freight economics lock customers into a 400-mile delivery radius. Armed with zero debt and a $371.1 million cash buffer, USLM successfully utilized raw cost-pass-through mechanisms to extract a 5.6% average selling price increase, driven heavily by runaway data center construction.

Conversely, scale dilutes per-capita productivity for the multinationals. Imerys’ Solutions for Refractory, Abrasives & Construction (RAC) segment generated roughly $354,000 per employee—one-third of USLM’s output—reflecting the operational drag of managing 38 industrial sites across 15 countries. Meanwhile, Minerals Technologies Inc. (MTI) suffered a steep drop into unprofitability, posting an $18.4 million net loss. Despite MTI’s formidable structural lock-in via 10-to-15-year evergreen satellite Precipitated Calcium Carbonate (PCC) plant contracts, the firm suffered from temporary margin compression due to the contractual "time lag" between absorbing inflated energy costs and triggering price adjustments.

Mid-cap players faced an entirely different reality: the "growth trap." Anhui Jinyan Kaolin (HKEX) saw its net margin compress to 14.3% in 2025. This contraction was driven by unabsorbed fixed costs from its new 40,000-ton refractory mullite capacity expansion and tactical price reductions aimed at raw market penetration.

Figure Global Giants vs Specialist SMEs in Non-Metallic Minerals

Supply Chain Pivot: Retreating from Legacy Industrial CyclesCorporate capital allocation in 2025 signals a permanent retreat from historically stable sectors now facing terminal decline—specifically premium graphic paper and coal-fired flue gas desulfurization.

Global leaders are aggressively realigning CAPEX to serve the green mobility and semiconductor megatrends. Imerys executed a $192.2 million (€170 million) capital injection into high-purity carbon black and synthetic graphite for lithium-ion anodes, supplemented by a $48.6 million (€43 million) targeted expansion in Mainland China for automotive polymer lightweighting. Having fully divested its cyclical paper assets in 2024 to avoid inventory de-stocking risks, Imerys is successfully decoupling from legacy industrial drag.

MTI is orchestrating a similar pivot. Bypassing the shrinking paper filler market, MTI drove its Environmental & Infrastructure line to $270.2 million in revenue, leaning heavily into its FLUORO-SORB technology for high-margin PFAS water remediation.

Regional players lacking internal R&D bandwidth are leaning into debt-leveraged vertical integration. Taekyung BK utilized a $50.6 million (KRW 72.0 billion) facility loan for the accretive acquisition of Lion Chemtech, bypassing organic material development entirely to capture immediate downstream market share in artificial marble and synthetic wax.

HDIN Institutional Perspective: Regulatory Ceilings and Peak Divergence

The "dig-and-ship" commodity model is obsolete. HDIN Research assesses that high-grade geological endowment (e.g., USLM's >80-year Life of Mine at Love Hollow) is merely a prerequisite; proprietary thermal/chemical processing and regulatory arbitrage are the true margin multipliers.

Macroeconomic "ceilings"—most notably the EU Carbon Border Adjustment Mechanism (CBAM) and shifting U.S. tariff structures—are actively penalizing unhedged, carbon-intensive operators. Imerys demonstrated best-in-class risk mitigation, utilizing $221.6 million (€196.0 million) in nominal forward energy hedges to insulate its thermal operations, allowing its Graphite & Carbon segment to expand adjusted EBITDA margins by 5.4 percentage points.

However, systemic forensic risks are emerging among heavily regionalized Asian SMEs. We note significant deterioration in Accounts Receivable (AR) quality for Taekyung BK, whose Expected Credit Loss (ECL) rate spiked to 2.9% alongside heavy reliance on $18.38 million (KRW 26.12 billion) in related-party transactions. Investors must heavily scrutinize regional operators that lack the geographic diversification to absorb localized macroeconomic shocks, as these entities are structurally vulnerable to legacy capacity overhangs.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in raw corporate filing synthesis, forensic accounting, and macroeconomic supply chain analysis. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.