European Battery Value Chains Diverge: IBU-tec Abandons Legacy Scale for 355% EBITDA Surge Amid PowerCo Mega-Deal

Date : 2026-04-11

Reading : 102

In FY2025, German advanced materials manufacturer IBU-tec and Volkswagen subsidiary PowerCo SE consolidated a localized European battery supply chain, driving a structural margin expansion that offsets IBU-tec's 12% revenue contraction. By aggressively phasing out material-intensive glass coating operations at its Weimar and BNT facilities, IBU-tec capitalized on strict EU Battery Regulation mandates, self-funding a transition to high-margin Lithium Iron Phosphate (LFP) production and achieving a net cash position ahead of its 2028 Bitterfeld mega-site launch.

Financial Health & Operational Moats: The Economics of Intentional Contraction

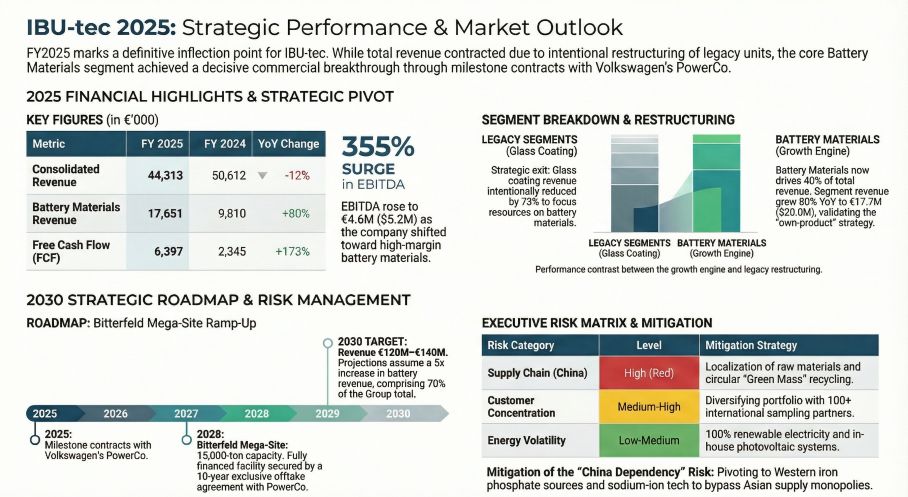

A superficial scan of IBU-tec’s FY2025 top-line metrics—a 12% consolidated revenue contraction to $50.10 million—suggests a victim of the broader European industrial slump. However, forensic analysis reveals a masterclass in structural realignment. The company executed a deliberate sacrifice of top-line scale to secure bottom-line durability.

By drastically downsizing the tin-heavy, low-margin Glass Coating segment within its BNT GmbH subsidiary (which plummeted 73% YoY), IBU-tec arrested the severe margin compression afflicting the broader German specialty chemicals sector. Consequently, the cost of materials ratio plummeted from 55.5% to 38.8%. This raw material pivot, combined with an 80% YoY surge in high-margin Battery Materials revenue ($19.96 million), catalyzed a 355% EBITDA explosion to $5.24 million (10.5% margin).

Rather than relying on risky accretive acquisitions to mask legacy decay, IBU-tec leveraged superior investment efficiency. Operating Cash Flow (OCF) surged 55% to $16.38 million. This hyper-efficient cash generation fully funded $11.13 million in gross CapEx—primarily dedicated to the upcoming Bitterfeld expansion—without triggering external debt dependencies. After systematically eliminating bank liabilities down to $3.38 million, against a cash reserve of $3.52 million, the firm now operates in a Net Cash position, entirely insulating its 2026-2028 expansion runway from European capital market volatility.

Figure IBU-tec 2025: Strategic Performance & Market Outlook

Supply Chain Pivot & Vertical Integration: Weaponizing Regulation

Supply Chain Pivot & Vertical Integration: Weaponizing Regulation

IBU-tec’s supply chain maneuvering in 2025 is directly engineered to exploit the geopolitical fracture between Western OEMs and Chinese LFP dominators (who currently control 98% of the global market). The EU Critical Raw Materials Act (CRMA) and the 2027 Digital Battery Passport mandate have transformed IBU-tec's localized production from a niche premium to an existential regulatory requirement for European automakers avoiding strict import tariffs.

To future-proof this moat, IBU-tec has initiated strict inventory de-stocking of legacy assets—evidenced by a $1.18 million write-down of older LFP materials—while simultaneously locking in forward capacity. The Weimar site is currently scaling transitional capacities of 3,300 tons, acting as a bridge to the 15,000-ton Bitterfeld mega-site, backed by a 10-year exclusive off-take agreement with PowerCo starting in 2028.

Crucially, the company is securing its upstream flank via aggressive vertical integration into circular economies. To hedge against critical mineral scarcity, IBU-tec successfully completed pilot trials with GRS Batterien Service GmbH to process LFP "black mass" into reusable "Green Mass." Paired with a newly constructed cathode foil recycling center in partnership with Hosokawa Alpine, IBU-tec is internalizing its secondary raw material streams.

Technological Readiness: Engineering Out the "Criticality"

While European chemical operators struggle to implement effective cost-pass-through mechanisms amid high natural gas prices, IBU-tec is bypassing the cost base entirely through material substitution.

The firm’s IP commercialization accelerated aggressively in 2025. The industrial-scale launch of IBUvolt® LMFP Gen0 directly targets the solid-state and NMC-blend battery markets. Furthermore, its proprietary dry-coating optimized LFP materials deliver a 40% lower carbon footprint than Asian counterparts, actively saving roughly one ton of CO2 per EV.

More disruptive is the advancement of Sodium-ion alternatives. The company's Sodium Manganese Oxide (NMO) and Sodium Iron Pyrophosphate (NFPP) materials—currently scaling with partners like UniverCell, Jungheinrich, and Wanhua Chemical Group—entirely engineer out lithium and cobalt dependencies, effectively rendering standard CRMA supply bottlenecks obsolete.

HDIN Institutional Perspective

IBU-tec’s FY2025 audit signals a definitive cyclical trough for traditional, volume-driven European chemical tolling and the inception of an IP-centric supercycle for localized battery materials.

While the broader German chemical industry idles at a toxic 70% capacity utilization rate, IBU-tec has artificially constructed a near-monopoly ring-fenced by EU protectionism. However, this aggressive repositioning carries severe concentration risks. The company’s 2030 projection—targeting $135–$158 million in revenue with 70% derived from batteries—is overwhelmingly anchored to a single node: Volkswagen's PowerCo. Should EV demand targets falter or the Bitterfeld JDA encounter operational friction, IBU-tec lacks the legacy chemical volumes to cushion the blow.

Ultimately, IBU-tec has transitioned from a resilient service provider to an apex supplier in the European electrification grid. Investors must track the scheduled 2026 operational launch of Bitterfeld’s advanced spray towers as the definitive leading indicator of its 2028 industrial-scale capabilities.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-dive corporate filing analysis, supply chain deconstruction, and macroeconomic strategic forecasting for global equities.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Economics of Intentional Contraction

A superficial scan of IBU-tec’s FY2025 top-line metrics—a 12% consolidated revenue contraction to $50.10 million—suggests a victim of the broader European industrial slump. However, forensic analysis reveals a masterclass in structural realignment. The company executed a deliberate sacrifice of top-line scale to secure bottom-line durability.

By drastically downsizing the tin-heavy, low-margin Glass Coating segment within its BNT GmbH subsidiary (which plummeted 73% YoY), IBU-tec arrested the severe margin compression afflicting the broader German specialty chemicals sector. Consequently, the cost of materials ratio plummeted from 55.5% to 38.8%. This raw material pivot, combined with an 80% YoY surge in high-margin Battery Materials revenue ($19.96 million), catalyzed a 355% EBITDA explosion to $5.24 million (10.5% margin).

Rather than relying on risky accretive acquisitions to mask legacy decay, IBU-tec leveraged superior investment efficiency. Operating Cash Flow (OCF) surged 55% to $16.38 million. This hyper-efficient cash generation fully funded $11.13 million in gross CapEx—primarily dedicated to the upcoming Bitterfeld expansion—without triggering external debt dependencies. After systematically eliminating bank liabilities down to $3.38 million, against a cash reserve of $3.52 million, the firm now operates in a Net Cash position, entirely insulating its 2026-2028 expansion runway from European capital market volatility.

Figure IBU-tec 2025: Strategic Performance & Market Outlook

Supply Chain Pivot & Vertical Integration: Weaponizing RegulationIBU-tec’s supply chain maneuvering in 2025 is directly engineered to exploit the geopolitical fracture between Western OEMs and Chinese LFP dominators (who currently control 98% of the global market). The EU Critical Raw Materials Act (CRMA) and the 2027 Digital Battery Passport mandate have transformed IBU-tec's localized production from a niche premium to an existential regulatory requirement for European automakers avoiding strict import tariffs.

To future-proof this moat, IBU-tec has initiated strict inventory de-stocking of legacy assets—evidenced by a $1.18 million write-down of older LFP materials—while simultaneously locking in forward capacity. The Weimar site is currently scaling transitional capacities of 3,300 tons, acting as a bridge to the 15,000-ton Bitterfeld mega-site, backed by a 10-year exclusive off-take agreement with PowerCo starting in 2028.

Crucially, the company is securing its upstream flank via aggressive vertical integration into circular economies. To hedge against critical mineral scarcity, IBU-tec successfully completed pilot trials with GRS Batterien Service GmbH to process LFP "black mass" into reusable "Green Mass." Paired with a newly constructed cathode foil recycling center in partnership with Hosokawa Alpine, IBU-tec is internalizing its secondary raw material streams.

Technological Readiness: Engineering Out the "Criticality"

While European chemical operators struggle to implement effective cost-pass-through mechanisms amid high natural gas prices, IBU-tec is bypassing the cost base entirely through material substitution.

The firm’s IP commercialization accelerated aggressively in 2025. The industrial-scale launch of IBUvolt® LMFP Gen0 directly targets the solid-state and NMC-blend battery markets. Furthermore, its proprietary dry-coating optimized LFP materials deliver a 40% lower carbon footprint than Asian counterparts, actively saving roughly one ton of CO2 per EV.

More disruptive is the advancement of Sodium-ion alternatives. The company's Sodium Manganese Oxide (NMO) and Sodium Iron Pyrophosphate (NFPP) materials—currently scaling with partners like UniverCell, Jungheinrich, and Wanhua Chemical Group—entirely engineer out lithium and cobalt dependencies, effectively rendering standard CRMA supply bottlenecks obsolete.

HDIN Institutional Perspective

IBU-tec’s FY2025 audit signals a definitive cyclical trough for traditional, volume-driven European chemical tolling and the inception of an IP-centric supercycle for localized battery materials.

While the broader German chemical industry idles at a toxic 70% capacity utilization rate, IBU-tec has artificially constructed a near-monopoly ring-fenced by EU protectionism. However, this aggressive repositioning carries severe concentration risks. The company’s 2030 projection—targeting $135–$158 million in revenue with 70% derived from batteries—is overwhelmingly anchored to a single node: Volkswagen's PowerCo. Should EV demand targets falter or the Bitterfeld JDA encounter operational friction, IBU-tec lacks the legacy chemical volumes to cushion the blow.

Ultimately, IBU-tec has transitioned from a resilient service provider to an apex supplier in the European electrification grid. Investors must track the scheduled 2026 operational launch of Bitterfeld’s advanced spray towers as the definitive leading indicator of its 2028 industrial-scale capabilities.

Presentation download:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional-grade market intelligence, specializing in deep-dive corporate filing analysis, supply chain deconstruction, and macroeconomic strategic forecasting for global equities.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*