Tencent (HKG: 0700) Consolidates AI Dominance as 'Hunyuan 3.0' Deployment Drives 45% EBITDA Margin Expansion in FY2025 Audit

Date : 2026-04-11

Reading : 152

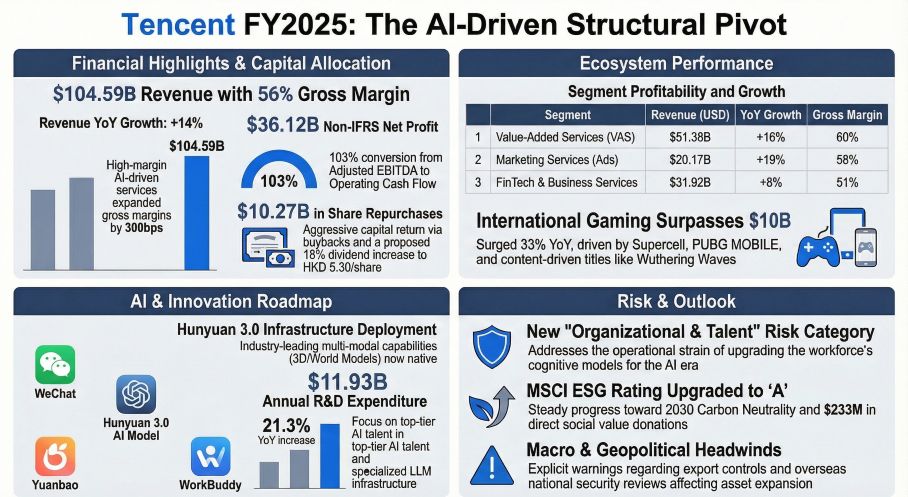

Shenzhen-based Tencent Holdings (HKG: 0700) executed a structural pivot in FY2025, transitioning from consumer traffic monetization to an AI-subsidized enterprise ecosystem. Driven by the commercialization of its Hunyuan 3.0 foundational model across cloud infrastructure and target advertising, the conglomerate reported a 14% year-over-year revenue increase to $104.59 billion. By capping ad-loads while maximizing AI-driven unit pricing, and breaching the $10 billion threshold in international gaming, management generated $48.38 billion in operating cash flow. This liquidity was aggressively deployed, including $10.27 billion in share repurchases, systematically shrinking the equity base to drive accretive long-term ROIC.

Financial Health & Operational Moats: Structural Operating Leverage and Capital Allocation

Tencent’s FY2025 architecture demonstrates a textbook execution of structural operating leverage. While top-line revenue expanded 14%, gross profit surged 21% to $58.80 billion, and Adjusted EBITDA margins expanded by 300 basis points to 45%. This profit delta confirms a highly favorable revenue mix shift toward zero-marginal-cost, high-leverage business units.

The underlying quality of earnings is exceptional. Operating Cash Flow (OCF) reached $48.38 billion, translating to an OCF-to-Adjusted EBITDA conversion rate exceeding 103%. This metric proves the core business is an unburdened cash engine, free from aggressive working capital accruals.

Crucially, the historically low-margin FinTech and Business Services (FBS) segment—which generated $31.92 billion—recorded a massive 400 basis point gross margin accretion, landing at 51%. This inflection point was catalyzed by scaled profitability within Tencent Cloud, driven by enterprise demand for Platform-as-a-Service (PaaS) and merchant technology service take-rates stemming from rising Gross Merchandise Value (GMV) inside closed-loop Weixin Shops. Management has effectively ring-fenced the balance sheet from venture volatility, recognizing $7.48 billion in long-term strategic net fair value gains (FVOCI) that bypass the P&L, while utilizing core operational cash to fund aggressive shareholder return mechanisms.

Figure Tencent FY2025: The Al-Driven Structural Pivot

Supply Chain Pivot: AI Compute CAPEX Replaces Channel Distribution Frictions

Supply Chain Pivot: AI Compute CAPEX Replaces Channel Distribution Frictions

A granular decomposition of Tencent's cost of revenues ($45.80 billion) reveals a bifurcated supply chain dynamic. The company exercises absolute pricing power over standard distribution channels; transaction and channel costs rose a mere 1.1% to $18.97 billion, proving the WeChat/Mini Program ecosystem successfully bypasses third-party distribution tolls.

However, the supply chain bottleneck has definitively shifted upstream toward heavy computing infrastructure and premium intellectual property. Capital allocation for server hosting and bandwidth surged 21.0% to $4.45 billion. This operational expenditure is directly tethered to the deployment of the Hunyuan 3.0 Large Language Model (LLM) and its multi-modal 3D generation capabilities.

Furthermore, as geopolitical friction triggers export controls and localized data sovereignty mandates, Tencent is accelerating the decentralization of its physical footprint. To mitigate cross-border data transfer liabilities, the company is routing heavy R&D and server infrastructure through Wholly Foreign-Owned Enterprises (WFOEs) stationed in strategic hubs like the Guian New Area and Yizheng data centers, treating regulatory compliance as a permanently rising fixed-cost anchor.

HDIN Institutional Perspective: The Margin Illusion and The 'Evergreen' Cash Engine

Linear models will misprice Tencent as a mature domestic social network facing demographic headwinds and regulatory ceilings. Our read of the FY2025 audit suggests the opposite: Tencent is operating with the unit economics of a B2B SaaS giant masked within a consumer gaming conglomerate.

The market has historically undervalued Tencent's disciplined ad-tech strategy. By deploying the "Tencent Ads AIM+" intelligent delivery matrix, the Marketing Services segment grew 19% to $20.17 billion and expanded gross margins to 58%—all while deliberately keeping ad-load rates suppressed below industry averages. This is not traffic harvesting; it is AI-driven cost-pass-through monetization based on conversion certainty.

Simultaneously, the gaming portfolio has decoupled from domestic consumption reliance. International games revenue spiked 33% YoY to $10.77 billion, anchored by Supercell titles, *PUBG MOBILE*, and new pipeline catalysts like *Wuthering Waves* and *Delta Force*.

Unlike Western mega-caps burning speculative cash on theoretical AI applications, Tencent’s $11.93 billion R&D expenditure (11.4% R&D intensity) is self-funded in real-time by immediate commercial yields in target advertising and enterprise cloud. Armed with a $14.91 billion net cash position and an impenetrable ecosystem moat, Tencent possesses the unleveraged balance sheet elasticity required to monopolize the next cyclical phase of AI-native infrastructure without diluting shareholder equity.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier independent market intelligence and strategic advisory firm. We specialize in deep-dive fundamental analysis, delivering institutional-grade insights into global equities, supply chain dynamics, and macroeconomic shifts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: Structural Operating Leverage and Capital Allocation

Tencent’s FY2025 architecture demonstrates a textbook execution of structural operating leverage. While top-line revenue expanded 14%, gross profit surged 21% to $58.80 billion, and Adjusted EBITDA margins expanded by 300 basis points to 45%. This profit delta confirms a highly favorable revenue mix shift toward zero-marginal-cost, high-leverage business units.

The underlying quality of earnings is exceptional. Operating Cash Flow (OCF) reached $48.38 billion, translating to an OCF-to-Adjusted EBITDA conversion rate exceeding 103%. This metric proves the core business is an unburdened cash engine, free from aggressive working capital accruals.

Crucially, the historically low-margin FinTech and Business Services (FBS) segment—which generated $31.92 billion—recorded a massive 400 basis point gross margin accretion, landing at 51%. This inflection point was catalyzed by scaled profitability within Tencent Cloud, driven by enterprise demand for Platform-as-a-Service (PaaS) and merchant technology service take-rates stemming from rising Gross Merchandise Value (GMV) inside closed-loop Weixin Shops. Management has effectively ring-fenced the balance sheet from venture volatility, recognizing $7.48 billion in long-term strategic net fair value gains (FVOCI) that bypass the P&L, while utilizing core operational cash to fund aggressive shareholder return mechanisms.

Figure Tencent FY2025: The Al-Driven Structural Pivot

Supply Chain Pivot: AI Compute CAPEX Replaces Channel Distribution FrictionsA granular decomposition of Tencent's cost of revenues ($45.80 billion) reveals a bifurcated supply chain dynamic. The company exercises absolute pricing power over standard distribution channels; transaction and channel costs rose a mere 1.1% to $18.97 billion, proving the WeChat/Mini Program ecosystem successfully bypasses third-party distribution tolls.

However, the supply chain bottleneck has definitively shifted upstream toward heavy computing infrastructure and premium intellectual property. Capital allocation for server hosting and bandwidth surged 21.0% to $4.45 billion. This operational expenditure is directly tethered to the deployment of the Hunyuan 3.0 Large Language Model (LLM) and its multi-modal 3D generation capabilities.

Furthermore, as geopolitical friction triggers export controls and localized data sovereignty mandates, Tencent is accelerating the decentralization of its physical footprint. To mitigate cross-border data transfer liabilities, the company is routing heavy R&D and server infrastructure through Wholly Foreign-Owned Enterprises (WFOEs) stationed in strategic hubs like the Guian New Area and Yizheng data centers, treating regulatory compliance as a permanently rising fixed-cost anchor.

HDIN Institutional Perspective: The Margin Illusion and The 'Evergreen' Cash Engine

Linear models will misprice Tencent as a mature domestic social network facing demographic headwinds and regulatory ceilings. Our read of the FY2025 audit suggests the opposite: Tencent is operating with the unit economics of a B2B SaaS giant masked within a consumer gaming conglomerate.

The market has historically undervalued Tencent's disciplined ad-tech strategy. By deploying the "Tencent Ads AIM+" intelligent delivery matrix, the Marketing Services segment grew 19% to $20.17 billion and expanded gross margins to 58%—all while deliberately keeping ad-load rates suppressed below industry averages. This is not traffic harvesting; it is AI-driven cost-pass-through monetization based on conversion certainty.

Simultaneously, the gaming portfolio has decoupled from domestic consumption reliance. International games revenue spiked 33% YoY to $10.77 billion, anchored by Supercell titles, *PUBG MOBILE*, and new pipeline catalysts like *Wuthering Waves* and *Delta Force*.

Unlike Western mega-caps burning speculative cash on theoretical AI applications, Tencent’s $11.93 billion R&D expenditure (11.4% R&D intensity) is self-funded in real-time by immediate commercial yields in target advertising and enterprise cloud. Armed with a $14.91 billion net cash position and an impenetrable ecosystem moat, Tencent possesses the unleveraged balance sheet elasticity required to monopolize the next cyclical phase of AI-native infrastructure without diluting shareholder equity.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier independent market intelligence and strategic advisory firm. We specialize in deep-dive fundamental analysis, delivering institutional-grade insights into global equities, supply chain dynamics, and macroeconomic shifts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.