Global Logistics Integrators See Diverging Margins: NYSE: UPS and SZSE: 002352 Extract Peak Yields Amid B2C Volume Contraction

Date : 2026-04-11

Reading : 376

Based on FY2025 corporate audits, the top six global logistics integrators—UPS, FedEx, DHL, SF Holding, La Poste, and CJ Logistics—are aggressively executing structural deleveraging and AI-driven capacity rationalization across bifurcated global supply chains. To defend operating margins against acute wage inflation and stagnant industrial demand, industry leaders are ruthlessly shedding commoditized B2C e-commerce volume. The strategic pivot centers entirely on accretive acquisitions in high-yield healthcare logistics and massive investments in labor-displacing automation, signaling a permanent end to the era of pure volume-driven growth.

Financial Health & Operational Moats: The Yield Optimization Playbook

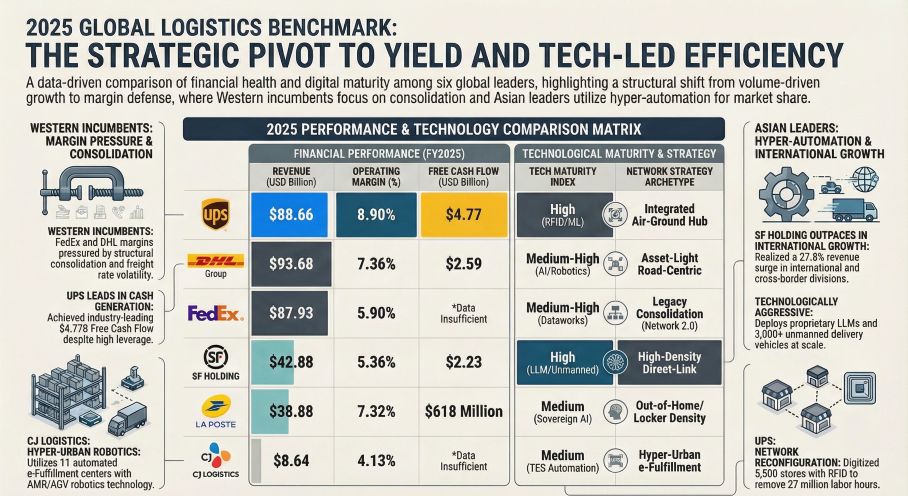

The 2025 cycle forces a brutal separation between operators extracting higher yields from fixed networks and those suffocating under legacy structural redundancies.

UPS (NYSE: UPS) demonstrates peerless operational leverage, posting an 8.9% operating margin ($7.87 billion operating profit) despite broader macroeconomic headwinds. This margin defense was not accidental; it is the direct result of extreme yield management. By intentionally purging 50% of its low-yielding volume from its largest e-commerce client and externalizing low-margin "Ground Saver" residential deliveries to the USPS, UPS manufactured a textbook cost-pass-through mechanism. The freed network capacity was immediately redirected into high-yield segments, supported by the accretive acquisitions of Frigo-Trans and Andlauer Healthcare Group (AHG), pushing UPS’s healthcare run-rate past $11 billion.

Conversely, FedEx (NYSE: FDX) sits at a 5.9% operating margin, currently absorbing $756 million in restructuring drag as it executes "Network 2.0" to physically consolidate 1,250 overlapping legacy facilities. While FedEx maintains a highly conservative balance sheet (73.3% Debt-to-Equity), its reliance on Mark-to-Market (MTM) pension accounting and continuous "business optimization" adjustments obscures the underlying volatility of its core operations. Meanwhile, European incumbents like DHL Group (ETR: DHL) are deliberately masking the cash-drain of inorganic growth by swapping standard Free Cash Flow KPIs for "FCF excluding M&A" starting in 2026—a clear red flag for structural cash constraints.

Figure 2025 GLOBAL LOGISTICS BENCHMARK

Supply Chain Pivot: Geopolitical Fragmentation & Asset-Light Defenses

Supply Chain Pivot: Geopolitical Fragmentation & Asset-Light Defenses

As global manufacturing enters a prolonged phase of inventory de-stocking and supply chain regionalization, operators are completely restructuring their capital asset allocations. The elimination of de minimis customs exemptions and escalating US-China tariffs have shattered traditional transpacific volume models.

In response, SF Holding (SZSE: 002352) is capitalizing on "China Plus One" dynamics. By weaponizing its Ezhou Cargo Hub and a fleet of 111 aircraft, SF is underwriting the capacity export of Chinese enterprises into Southeast Asia and Europe, driving a staggering 27.8% growth in international cross-border revenue.

Western integrators are taking defensive postures. FedEx and UPS are permanently retiring their aging Boeing MD-11 fleets to stem capital bleeding and right-size capacity. In Europe, DHL Group is aggressively mitigating exposure to industrial macro-credit shocks and the draconian EU ReFuelEU mandates (requiring a 2% Sustainable Aviation Fuel blend starting in 2025) by leaning heavily on an asset-light model. Of DHL's €2.46 billion Express CAPEX, a massive €1.58 billion was channeled into Right-of-Use (RoU) leases, insulating its balance sheet from stranded physical assets.

Technology & CAPEX: Structural Automation Over Physical Capacity

Capital expenditure is no longer allocated to fleet expansion; it is aggressively funneled into labor-displacing digital architecture. The logistics cycle demands vertical integration of physical nodes and predictive data to counter structural wage inflation.

SF Holding stands as the most technologically aggressive operator, actively deploying its proprietary "Fengzhi" vertical large language model (consuming 10 billion tokens daily) and fielding nearly 3,000 Level-4 unmanned delivery vehicles. This transition from pilot to commercial scale structurally strips out driver wage inflation and reverse logistics costs. Western incumbents are utilizing an "incrementally adaptive" approach. UPS is deploying $2.4 billion in 2026 tech CAPEX strictly to digitize its physical workflows—rolling out RFID "Smart Package" sensing across 5,500 retail locations to eliminate manual scanning bottlenecks. This enabled UPS to structurally remove 27 million labor hours from its P&L in 2025.

HDIN Institutional Perspective: Navigating the Cyclical Trough

We assess that the global logistics sector has hit a definitive cyclical trough regarding base volume growth. The divergence between U.S. network deleveraging and Asian hyper-density automation confirms that the traditional global hub-and-spoke hegemony is fracturing.

Going forward, true market moats will not be measured by physical vehicle counts, but by end-to-end data visibility and specialized sector dominance. Operators tied to strict public service mandates or fractured cross-border subsidiaries face severe downside risk. La Poste’s alarming 5.2x Net Debt/EBITDA leverage ratio (exacerbated by a $1.1 billion uncompensated public service deficit) and CJ Logistics' (KRX: 000120) rampant off-balance-sheet contagion risk via cross-subsidiary payment guarantees highlight the fragility of operators lacking pricing power. The ultimate secular winners through 2026 will be those that ruthlessly enforce facility consolidation, pass through labor inflation via dynamic pricing algorithms, and monopolize the resilient, high-margin healthcare cold-chain.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic advisory and equity intelligence firm delivering institutional-grade analysis on global supply chains, industrial macros, and capital markets. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Yield Optimization Playbook

The 2025 cycle forces a brutal separation between operators extracting higher yields from fixed networks and those suffocating under legacy structural redundancies.

UPS (NYSE: UPS) demonstrates peerless operational leverage, posting an 8.9% operating margin ($7.87 billion operating profit) despite broader macroeconomic headwinds. This margin defense was not accidental; it is the direct result of extreme yield management. By intentionally purging 50% of its low-yielding volume from its largest e-commerce client and externalizing low-margin "Ground Saver" residential deliveries to the USPS, UPS manufactured a textbook cost-pass-through mechanism. The freed network capacity was immediately redirected into high-yield segments, supported by the accretive acquisitions of Frigo-Trans and Andlauer Healthcare Group (AHG), pushing UPS’s healthcare run-rate past $11 billion.

Conversely, FedEx (NYSE: FDX) sits at a 5.9% operating margin, currently absorbing $756 million in restructuring drag as it executes "Network 2.0" to physically consolidate 1,250 overlapping legacy facilities. While FedEx maintains a highly conservative balance sheet (73.3% Debt-to-Equity), its reliance on Mark-to-Market (MTM) pension accounting and continuous "business optimization" adjustments obscures the underlying volatility of its core operations. Meanwhile, European incumbents like DHL Group (ETR: DHL) are deliberately masking the cash-drain of inorganic growth by swapping standard Free Cash Flow KPIs for "FCF excluding M&A" starting in 2026—a clear red flag for structural cash constraints.

Figure 2025 GLOBAL LOGISTICS BENCHMARK

Supply Chain Pivot: Geopolitical Fragmentation & Asset-Light DefensesAs global manufacturing enters a prolonged phase of inventory de-stocking and supply chain regionalization, operators are completely restructuring their capital asset allocations. The elimination of de minimis customs exemptions and escalating US-China tariffs have shattered traditional transpacific volume models.

In response, SF Holding (SZSE: 002352) is capitalizing on "China Plus One" dynamics. By weaponizing its Ezhou Cargo Hub and a fleet of 111 aircraft, SF is underwriting the capacity export of Chinese enterprises into Southeast Asia and Europe, driving a staggering 27.8% growth in international cross-border revenue.

Western integrators are taking defensive postures. FedEx and UPS are permanently retiring their aging Boeing MD-11 fleets to stem capital bleeding and right-size capacity. In Europe, DHL Group is aggressively mitigating exposure to industrial macro-credit shocks and the draconian EU ReFuelEU mandates (requiring a 2% Sustainable Aviation Fuel blend starting in 2025) by leaning heavily on an asset-light model. Of DHL's €2.46 billion Express CAPEX, a massive €1.58 billion was channeled into Right-of-Use (RoU) leases, insulating its balance sheet from stranded physical assets.

Technology & CAPEX: Structural Automation Over Physical Capacity

Capital expenditure is no longer allocated to fleet expansion; it is aggressively funneled into labor-displacing digital architecture. The logistics cycle demands vertical integration of physical nodes and predictive data to counter structural wage inflation.

SF Holding stands as the most technologically aggressive operator, actively deploying its proprietary "Fengzhi" vertical large language model (consuming 10 billion tokens daily) and fielding nearly 3,000 Level-4 unmanned delivery vehicles. This transition from pilot to commercial scale structurally strips out driver wage inflation and reverse logistics costs. Western incumbents are utilizing an "incrementally adaptive" approach. UPS is deploying $2.4 billion in 2026 tech CAPEX strictly to digitize its physical workflows—rolling out RFID "Smart Package" sensing across 5,500 retail locations to eliminate manual scanning bottlenecks. This enabled UPS to structurally remove 27 million labor hours from its P&L in 2025.

HDIN Institutional Perspective: Navigating the Cyclical Trough

We assess that the global logistics sector has hit a definitive cyclical trough regarding base volume growth. The divergence between U.S. network deleveraging and Asian hyper-density automation confirms that the traditional global hub-and-spoke hegemony is fracturing.

Going forward, true market moats will not be measured by physical vehicle counts, but by end-to-end data visibility and specialized sector dominance. Operators tied to strict public service mandates or fractured cross-border subsidiaries face severe downside risk. La Poste’s alarming 5.2x Net Debt/EBITDA leverage ratio (exacerbated by a $1.1 billion uncompensated public service deficit) and CJ Logistics' (KRX: 000120) rampant off-balance-sheet contagion risk via cross-subsidiary payment guarantees highlight the fragility of operators lacking pricing power. The ultimate secular winners through 2026 will be those that ruthlessly enforce facility consolidation, pass through labor inflation via dynamic pricing algorithms, and monopolize the resilient, high-margin healthcare cold-chain.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic advisory and equity intelligence firm delivering institutional-grade analysis on global supply chains, industrial macros, and capital markets. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.