Global Sportswear Giants See Diverging Margins: Lululemon and ANTA Defy Sector Compression with ~20% Operating Margins Amid FY2025 Macro Headwinds

Date : 2026-04-11

Reading : 324

During the FY2025 audit cycle, global sportswear leaders (NYSE: NKE, FRA: ADS, NASDAQ: LULU, HKG: 2020) experienced a severe structural realignment across the North American, EMEA, and Greater China markets. Driven by a rigid macroeconomic ceiling on discretionary spending, volatile geopolitical tariffs, and bloated wholesale channels, legacy brands suffered acute margin compression. In contrast, agile players leveraging Direct-to-Consumer (DTC) ecosystems and algorithmic demand-pull models executed precise inventory de-stocking, effectively defining the new profitability frontier for the broader consumer discretionary sector.

Financial Health & Operational Moats: The Cost of the "Bullwhip"

A forensic analysis of FY2025 capital deployment and profitability uncovers a stark divergence in operational efficiency, fundamentally separating DTC-native ecosystems from wholesale-dependent legacy models.

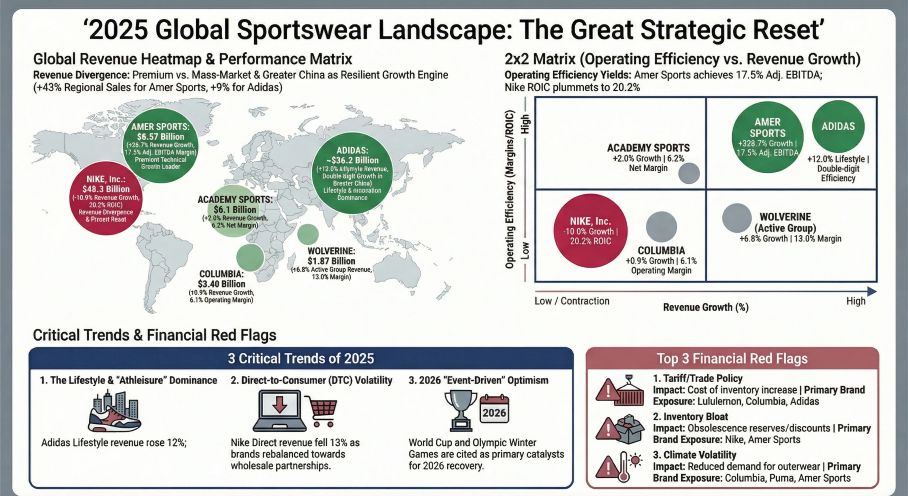

Figure 2025 Global Sportswear Landscape: The Great Strategic Reset

The Efficiency Frontier vs. Margin Compression

The Efficiency Frontier vs. Margin Compression

Lululemon (NASDAQ: LULU) and ANTA Sports (HKG: 2020) have fortified structural pricing moats, capturing sector-leading operating margins of 19.9% and 23.8%, respectively. Lululemon’s near-pure DTC model (generating 89.8% of revenue natively) effectively immunized its core product margins—reaching 76.4% in Mainland China—against the promotional discounting that ravaged the sector. Furthermore, ANTA's execution of accretive acquisitions (notably DESCENTE and MAIA ACTIVE) has allowed it to monopolize high-margin, premium technical niches across Asia.

Conversely, legacy wholesale heavyweights suffered severe margin compression. NIKE, Inc. (NYSE: NKE) posted an 8.2% operating margin, penalized by a 190-basis-point drop in gross margin directly attributable to massive inventory obsolescence reserves and forced wholesale liquidations. PUMA SE (ETR: PUM) hit the bottom of the efficiency frontier, absorbing a massive 13.1% revenue contraction and negative operating margins (-4.9%) as it deliberately withdrew inventory from off-price channels to salvage brand equity.

Audit Integrity & Financial Red Flags

HDIN desk analysts note multiple critical audit warnings across the sector that signal internal distress. Amer Sports (NYSE: AS) received an adverse opinion from independent auditor KPMG regarding a material weakness in internal controls over financial reporting, fundamentally elevating its risk profile. Adidas (FRA: ADS) exhibited a severe earnings-to-cash mismatch: despite reporting $1.51 billion in net income, its net operating cash flow (OCF) registered a mere $849.1 million (a 0.56x OCF-to-Net-Income ratio), signaling aggressive revenue recognition against a bloated $6.59 billion ending inventory. Meanwhile, Columbia Sportswear (NASDAQ: COLM) recognized $29 million in intangible asset impairments for its prAna and Mountain Hardwear units, indicating permanent value destruction in historical buyouts.

Supply Chain Pivot: Tariff Realities and The Regulatory Ceiling

Geopolitical friction and ESG mandates are no longer peripheral risk factors; they are absolute determinants of CapEx allocation and supply chain viability.

De-Risking and Geographic Reallocation

The industry remains overwhelmingly reliant on Asian off-shoring, but the tactical architectures are shifting. Adidas is executing a localized "de-risking" strategy, distributing its multi-country origin risk across Vietnam (27%), Indonesia (18%), and China (16%) while prioritizing local-for-local manufacturing to bypass customs bottlenecks. PUMA similarly commands 95% of its production volume in Asia but actively shifted US-bound manufacturing out of China to dodge UFLPA and tariff crossfire.

Conversely, Wolverine World Wide (NYSE: WWW) acknowledges severe vulnerability due to its reliance on third-party Asia-Pacific manufacturers without meaningful vertical integration, making trade disruptions prohibitively expensive.

The Failure of Cost-Pass-Through Mechanisms

To combat inflation and import duties, brands attempted to leverage cost-pass-through mechanisms, but consumer elasticity has snapped. Columbia Sportswear explicitly cited that tariff-induced price hikes are actively suppressing unit demand among U.S. middle-income consumers. To secure their cost of capital, brands are being forced to absorb higher compliance OpEx tied to Science Based Targets initiative (SBTi) mandates and Scope 3 carbon decoupling, shifting capital away from traditional marketing into supply chain traceability.

HDIN Institutional Perspective: AI Operationalization and The End of the Legacy Model

The 2025 data confirms that the historical playbook—relying on mass wholesale distribution and legacy athletic endorsements—is dead. NIKE’s Jordan brand suffered a 16% revenue decline, exposing deep fatigue in heritage positioning. In its place, brands like Adidas and PUMA are capturing the Gen Z wallet via hyper-targeted cultural revivals (Samba/Terrace franchises) and mental-health-conscious messaging, successfully moving away from pure performance marketing.

However, the most profound structural shift is the bifurcation in digital transformation. Western market leaders treat Artificial Intelligence primarily as a defensive risk factor—citing fears of IP infringement or cybersecurity vulnerabilities in their 10-K filings. In stark contrast, ANTA Sports has deeply operationalized AI. Through its "AI365" framework and "Linglong" large model, ANTA generated over $1.25 billion in AI-assisted product orders and drove a 20% increase in conversion rates via algorithmic private-domain CRM targeting.

This asymmetry signals a permanent cyclical trough for companies clinging to push-based manufacturing. The ultimate survivors of the 2026 fiscal cycle will not be those with the highest human capital efficiency (a metric where Nike currently excels but fails to translate to bottom-line profit), but those that utilize algorithmic demand-pull ecosystems to maintain full-price sell-through.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic intelligence and corporate finance advisory firm delivering institutional-grade market analysis. We specialize in MECE-driven forensic accounting, supply chain vulnerability, and global macro-strategy evaluation. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of the "Bullwhip"

A forensic analysis of FY2025 capital deployment and profitability uncovers a stark divergence in operational efficiency, fundamentally separating DTC-native ecosystems from wholesale-dependent legacy models.

Figure 2025 Global Sportswear Landscape: The Great Strategic Reset

The Efficiency Frontier vs. Margin CompressionLululemon (NASDAQ: LULU) and ANTA Sports (HKG: 2020) have fortified structural pricing moats, capturing sector-leading operating margins of 19.9% and 23.8%, respectively. Lululemon’s near-pure DTC model (generating 89.8% of revenue natively) effectively immunized its core product margins—reaching 76.4% in Mainland China—against the promotional discounting that ravaged the sector. Furthermore, ANTA's execution of accretive acquisitions (notably DESCENTE and MAIA ACTIVE) has allowed it to monopolize high-margin, premium technical niches across Asia.

Conversely, legacy wholesale heavyweights suffered severe margin compression. NIKE, Inc. (NYSE: NKE) posted an 8.2% operating margin, penalized by a 190-basis-point drop in gross margin directly attributable to massive inventory obsolescence reserves and forced wholesale liquidations. PUMA SE (ETR: PUM) hit the bottom of the efficiency frontier, absorbing a massive 13.1% revenue contraction and negative operating margins (-4.9%) as it deliberately withdrew inventory from off-price channels to salvage brand equity.

Audit Integrity & Financial Red Flags

HDIN desk analysts note multiple critical audit warnings across the sector that signal internal distress. Amer Sports (NYSE: AS) received an adverse opinion from independent auditor KPMG regarding a material weakness in internal controls over financial reporting, fundamentally elevating its risk profile. Adidas (FRA: ADS) exhibited a severe earnings-to-cash mismatch: despite reporting $1.51 billion in net income, its net operating cash flow (OCF) registered a mere $849.1 million (a 0.56x OCF-to-Net-Income ratio), signaling aggressive revenue recognition against a bloated $6.59 billion ending inventory. Meanwhile, Columbia Sportswear (NASDAQ: COLM) recognized $29 million in intangible asset impairments for its prAna and Mountain Hardwear units, indicating permanent value destruction in historical buyouts.

Supply Chain Pivot: Tariff Realities and The Regulatory Ceiling

Geopolitical friction and ESG mandates are no longer peripheral risk factors; they are absolute determinants of CapEx allocation and supply chain viability.

De-Risking and Geographic Reallocation

The industry remains overwhelmingly reliant on Asian off-shoring, but the tactical architectures are shifting. Adidas is executing a localized "de-risking" strategy, distributing its multi-country origin risk across Vietnam (27%), Indonesia (18%), and China (16%) while prioritizing local-for-local manufacturing to bypass customs bottlenecks. PUMA similarly commands 95% of its production volume in Asia but actively shifted US-bound manufacturing out of China to dodge UFLPA and tariff crossfire.

Conversely, Wolverine World Wide (NYSE: WWW) acknowledges severe vulnerability due to its reliance on third-party Asia-Pacific manufacturers without meaningful vertical integration, making trade disruptions prohibitively expensive.

The Failure of Cost-Pass-Through Mechanisms

To combat inflation and import duties, brands attempted to leverage cost-pass-through mechanisms, but consumer elasticity has snapped. Columbia Sportswear explicitly cited that tariff-induced price hikes are actively suppressing unit demand among U.S. middle-income consumers. To secure their cost of capital, brands are being forced to absorb higher compliance OpEx tied to Science Based Targets initiative (SBTi) mandates and Scope 3 carbon decoupling, shifting capital away from traditional marketing into supply chain traceability.

HDIN Institutional Perspective: AI Operationalization and The End of the Legacy Model

The 2025 data confirms that the historical playbook—relying on mass wholesale distribution and legacy athletic endorsements—is dead. NIKE’s Jordan brand suffered a 16% revenue decline, exposing deep fatigue in heritage positioning. In its place, brands like Adidas and PUMA are capturing the Gen Z wallet via hyper-targeted cultural revivals (Samba/Terrace franchises) and mental-health-conscious messaging, successfully moving away from pure performance marketing.

However, the most profound structural shift is the bifurcation in digital transformation. Western market leaders treat Artificial Intelligence primarily as a defensive risk factor—citing fears of IP infringement or cybersecurity vulnerabilities in their 10-K filings. In stark contrast, ANTA Sports has deeply operationalized AI. Through its "AI365" framework and "Linglong" large model, ANTA generated over $1.25 billion in AI-assisted product orders and drove a 20% increase in conversion rates via algorithmic private-domain CRM targeting.

This asymmetry signals a permanent cyclical trough for companies clinging to push-based manufacturing. The ultimate survivors of the 2026 fiscal cycle will not be those with the highest human capital efficiency (a metric where Nike currently excels but fails to translate to bottom-line profit), but those that utilize algorithmic demand-pull ecosystems to maintain full-price sell-through.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic intelligence and corporate finance advisory firm delivering institutional-grade market analysis. We specialize in MECE-driven forensic accounting, supply chain vulnerability, and global macro-strategy evaluation. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*