PropTech Ecosystems Pivot to Edge AI Hardware as SIMPPLE Posts 188% Robotics Surge in FY2025 Audit

Date : 2026-04-13

Reading : 138

SIMPPLE LTD engineered a 57% top-line recovery to $4.52 million in FY2025, driven entirely by an aggressive pivot toward robotics hardware that masked a severe 34% contraction in its high-margin software segment. Operating from its Singapore headquarters with supply chain anchor points in China, the facility management firm is aggressively scaling its AI ecosystem to combat regional labor shortages. However, escalating capital requirements, margin compression, and reliance on high-interest private debt reveal a highly cash-consumptive transition phase ahead of its strategic global expansion and $5 million April 2026 public offering.

Financial Health & Operational Moats: The Cost of Hardware Integration

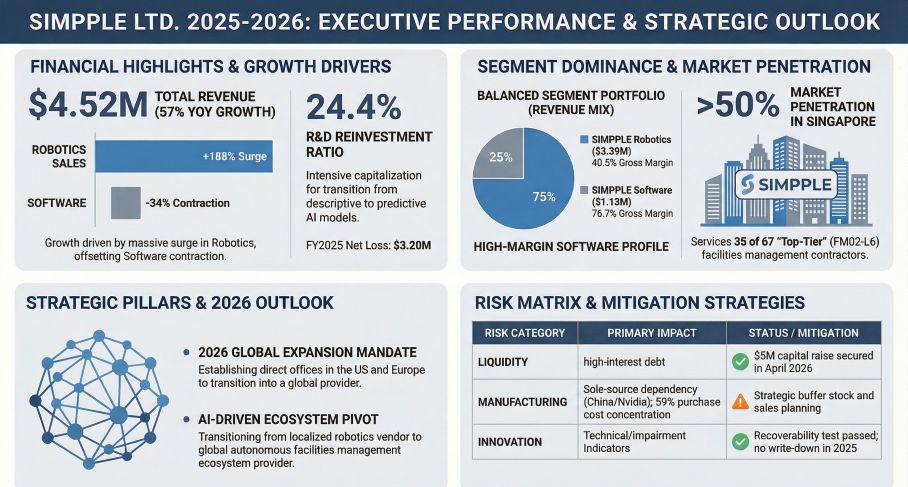

SIMPPLE’s FY2025 financial disclosures reveal a structural divergence in its revenue quality. Total revenue climbed to $4.52 million (S$5.91 million), but the underlying composition exposes significant margin compression. The company’s "Star" segment—SIMPPLE Robotics—surged 188% year-over-year to $3.39 million, fueled by adoption of Cenobot and Gausium models. Conversely, its "Cash Cow" SIMPPLE Software segment, positioned as a sticky, high-margin SaaS platform, contracted by 34% to $1.13 million.

This horizontal divergence exacted a heavy toll on profitability. Overall gross margins compressed by 10.3 percentage points to 49.6%. The company is trading the 76.7% gross margins of its software suite for the 40.5% margins of its hardware distribution.

Yet, the operational moat lies in high switching costs and infrastructure embedding. SIMPPLE’s proprietary "Gemini" robot exemplifies this vertical integration, fusing a modular security and digital concierge head onto third-party scrubbing bases. The firm is reinvesting heavily into this ecosystem, capitalizing $1.11 million in software development costs—effectively injecting 24.4% of total top-line revenue back into R&D. While this builds a formidable IP portfolio (including patent 10202203801Q for autonomous dispatch), the capitalization defers immediate P&L impact, highlighting that the core A.I. engine remains in a highly active, capital-intensive training phase.

Figure SIMPPLE LTD 2025-2026: EXECUTIVE PERFORMANCE & STRATEGIC OUTLOOK

Supply Chain Pivot: The Geopolitics of Outsourced Robotics

Supply Chain Pivot: The Geopolitics of Outsourced Robotics

SIMPPLE operates an asset-light framework that heavily centralizes its physical supply chain risk. The company does not manufacture its own hardware, relying on an outsourced network anchored by two primary Chinese OEMs: Shanghai Gaoxian Automation Technology Development Co., Ltd. (Gausium) and Hangzhou Cape of Good Hope Robots Co., Ltd. (Cenobots). In FY2025, these two entities commanded 59% of SIMPPLE’s total purchase and subcontractor costs.

Crucially, SIMPPLE relies on sole-source dependencies for advanced intelligence, explicitly requiring Nvidia Xavier AI edge computing chips to power its Cenobot fleet. This concentrated exposure leaves the firm highly vulnerable to cross-border logistics frictions and semiconductor embargoes.

To mitigate these shocks and support its 2026 mandate to open direct offices in the United States and Europe, the company is avoiding standard inventory de-stocking protocols. Instead, management is deliberately operating at a lower inventory velocity (3.7x turnover, equating to roughly 98.6 Days Sales of Inventory), stockpiling extensive demonstration units. While this acts as a buffer against escalating freight charges, it ties up critical working capital during a period of strained liquidity.

Corporate Governance: Shadow Treasuries and C-Suite Transitions

An audit of the company’s capital structure exposes significant principal-agent friction. The company’s Debt-to-Equity ratio spiked from 21.3% in 2024 to 79.2% in 2025. Strikingly, interest expenses exploded by 1,345% year-over-year due to the utilization of private debt carrying 12% to 36% annualized interest rates.

Simultaneously, the firm operates with a high degree of related-party entanglement. WIS Holdings Pte. Ltd.—affiliated with beneficial owner Mr. Poo Chong Hee—functions simultaneously as a primary revenue generator, unsecured lender, and historical debt guarantor. This shadow-treasury dynamic complicates the objective independence of the board, compounded by a transitional corporate culture. The abrupt January 2026 resignation of CEO Norman Schroeder to lead the divested Australian subsidiary, replaced by Co-founder Pat Kah Kit Daryl as Acting CEO, underscores an internal environment aggressively prioritizing cost optimization and restructuring over stable continuity.

HDIN Institutional Perspective

SIMPPLE’s FY2025 performance is a bellwether for the broader PropTech and facility management sector. The cycle of deploying pure-play software has hit a ceiling; asset owners now demand integrated hardware execution. However, SIMPPLE’s financial architecture illustrates that this transition is aggressively cash-consumptive. Cost-pass-through mechanisms are currently failing to offset the margin dilution inherent in physical robotics deployment.

The firm’s roadmap for 2026 relies on establishing joint ventures (like its European alliance with Evolve Consulting ApS) and executing accretive acquisitions of regional distributors to capture market share. But the structural reliance on Chinese hardware combined with U.S. and European expansion targets presents a bifurcated geopolitical tightrope. The $5 million raised in April 2026 secures near-term going-concern viability, but long-term institutional backing will require a stabilization of the SaaS revenue contraction to prove the ecosystem is genuinely sticky, rather than just a sophisticated hardware distribution channel.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About Us: About HDIN Research (www.hdinresearch.com).

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Cost of Hardware Integration

SIMPPLE’s FY2025 financial disclosures reveal a structural divergence in its revenue quality. Total revenue climbed to $4.52 million (S$5.91 million), but the underlying composition exposes significant margin compression. The company’s "Star" segment—SIMPPLE Robotics—surged 188% year-over-year to $3.39 million, fueled by adoption of Cenobot and Gausium models. Conversely, its "Cash Cow" SIMPPLE Software segment, positioned as a sticky, high-margin SaaS platform, contracted by 34% to $1.13 million.

This horizontal divergence exacted a heavy toll on profitability. Overall gross margins compressed by 10.3 percentage points to 49.6%. The company is trading the 76.7% gross margins of its software suite for the 40.5% margins of its hardware distribution.

Yet, the operational moat lies in high switching costs and infrastructure embedding. SIMPPLE’s proprietary "Gemini" robot exemplifies this vertical integration, fusing a modular security and digital concierge head onto third-party scrubbing bases. The firm is reinvesting heavily into this ecosystem, capitalizing $1.11 million in software development costs—effectively injecting 24.4% of total top-line revenue back into R&D. While this builds a formidable IP portfolio (including patent 10202203801Q for autonomous dispatch), the capitalization defers immediate P&L impact, highlighting that the core A.I. engine remains in a highly active, capital-intensive training phase.

Figure SIMPPLE LTD 2025-2026: EXECUTIVE PERFORMANCE & STRATEGIC OUTLOOK

Supply Chain Pivot: The Geopolitics of Outsourced RoboticsSIMPPLE operates an asset-light framework that heavily centralizes its physical supply chain risk. The company does not manufacture its own hardware, relying on an outsourced network anchored by two primary Chinese OEMs: Shanghai Gaoxian Automation Technology Development Co., Ltd. (Gausium) and Hangzhou Cape of Good Hope Robots Co., Ltd. (Cenobots). In FY2025, these two entities commanded 59% of SIMPPLE’s total purchase and subcontractor costs.

Crucially, SIMPPLE relies on sole-source dependencies for advanced intelligence, explicitly requiring Nvidia Xavier AI edge computing chips to power its Cenobot fleet. This concentrated exposure leaves the firm highly vulnerable to cross-border logistics frictions and semiconductor embargoes.

To mitigate these shocks and support its 2026 mandate to open direct offices in the United States and Europe, the company is avoiding standard inventory de-stocking protocols. Instead, management is deliberately operating at a lower inventory velocity (3.7x turnover, equating to roughly 98.6 Days Sales of Inventory), stockpiling extensive demonstration units. While this acts as a buffer against escalating freight charges, it ties up critical working capital during a period of strained liquidity.

Corporate Governance: Shadow Treasuries and C-Suite Transitions

An audit of the company’s capital structure exposes significant principal-agent friction. The company’s Debt-to-Equity ratio spiked from 21.3% in 2024 to 79.2% in 2025. Strikingly, interest expenses exploded by 1,345% year-over-year due to the utilization of private debt carrying 12% to 36% annualized interest rates.

Simultaneously, the firm operates with a high degree of related-party entanglement. WIS Holdings Pte. Ltd.—affiliated with beneficial owner Mr. Poo Chong Hee—functions simultaneously as a primary revenue generator, unsecured lender, and historical debt guarantor. This shadow-treasury dynamic complicates the objective independence of the board, compounded by a transitional corporate culture. The abrupt January 2026 resignation of CEO Norman Schroeder to lead the divested Australian subsidiary, replaced by Co-founder Pat Kah Kit Daryl as Acting CEO, underscores an internal environment aggressively prioritizing cost optimization and restructuring over stable continuity.

HDIN Institutional Perspective

SIMPPLE’s FY2025 performance is a bellwether for the broader PropTech and facility management sector. The cycle of deploying pure-play software has hit a ceiling; asset owners now demand integrated hardware execution. However, SIMPPLE’s financial architecture illustrates that this transition is aggressively cash-consumptive. Cost-pass-through mechanisms are currently failing to offset the margin dilution inherent in physical robotics deployment.

The firm’s roadmap for 2026 relies on establishing joint ventures (like its European alliance with Evolve Consulting ApS) and executing accretive acquisitions of regional distributors to capture market share. But the structural reliance on Chinese hardware combined with U.S. and European expansion targets presents a bifurcated geopolitical tightrope. The $5 million raised in April 2026 secures near-term going-concern viability, but long-term institutional backing will require a stabilization of the SaaS revenue contraction to prove the ecosystem is genuinely sticky, rather than just a sophisticated hardware distribution channel.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About Us: About HDIN Research (www.hdinresearch.com).

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.