Deepexi (1384.HK) Pivots to Agentic AI as FastAGI Revenue Surges 181.5% Amid Structural Receivables Drag

Date : 2026-04-14

Reading : 305

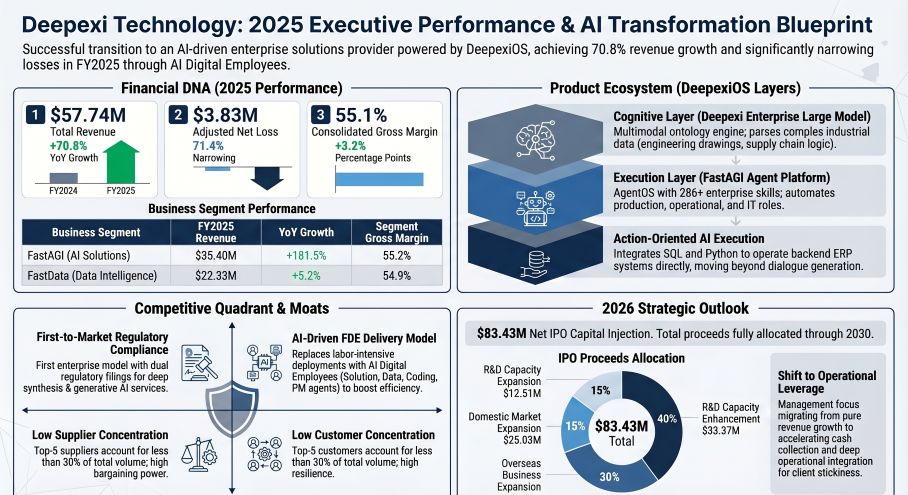

Deepexi Technology Co., Ltd. (1384.HK) reported a 70.8% top-line expansion to $57.74 million in FY2025, driven by a violent structural pivot toward enterprise AI in the Chinese B2B software market. The hyper-growth is anchored by its FastAGI unit, which cannibalized legacy data integration pipelines to deliver 61.3% of total revenue. While aggressive internal labor automation expanded gross margins to 55.1%, severe working capital bottlenecks and geopolitical hardware dependencies threaten to pressure near-term liquidity despite an $83.43 million IPO injection.

Financial Health & Operational Moats: The Labor Arbitrage Play

Deepexi’s FY2025 audit reveals a company actively transitioning away from labor-intensive project deployments toward AI-driven operational leverage. The legacy FastData segment stagnated at a 5.2% growth rate ($22.33 million), while the FastAGI Enterprise AI Solutions unit exploded by 181.5% to $35.40 million.

The "So What": This top-line rotation masks a deeper structural labor arbitrage. Deepexi expanded consolidated gross margins from 51.9% to 55.1% not through pricing power, but by deploying internal proprietary AI digital employees (FastAGI agents) to co-pilot its Forward Deployed Engineers (FDEs). By automating data governance, coding, and project management workflows, per capita productivity accelerated to $124,440 across its 464-person workforce.

Furthermore, earnings quality remains highly conservative. The headline statutory net loss of $130.03 million is a phantom accounting artifact, heavily distorted by a $102.28 million non-cash fair value loss on pre-IPO preferred shares and a 4,040% surge in Stock-Based Compensation ($16.04 million). Stripping out these frictions, the adjusted net loss narrowed by 71.4% to a mere $3.83 million. The company enforces strict R&D expensing—funneling $14.98 million entirely through the P&L—eliminating the risk of future intangible asset impairment and securing a pristine, debt-to-asset profile of 23.4% post-IPO.

Figure Deepexi Technology: 2025 Executive Performance & Al Transformation Blueprint

Supply Chain Pivot: Hybrid Infrastructure & The Silicon Ceiling

Supply Chain Pivot: Hybrid Infrastructure & The Silicon Ceiling

Deepexi operates a decentralized procurement matrix, with top-five supplier concentration strictly capped below 30%. However, management is executing a distinct hybrid compute infrastructure pivot. While OPEX for third-party cloud services surged to support Supervised Fine-Tuning (SFT) and multimodal ontology modeling, the company simultaneously aggressively scaled its physical AI server CAPEX, driving Property, Plant, and Equipment (PPE) up 77.1%.

This dual-track sourcing highlights a systemic vulnerability. While Deepexi plans to deploy $33.37 million of its IPO proceeds toward software R&D through 2030, no amount of internal capital allocation can bypass international export control laws. The company's reliance on open-source foundation models combined with an escalating need for heavy compute power exposes it directly to macro-geopolitical silicon embargoes. If physical hardware access tightens, management's ability to maintain its enterprise large model capabilities will be severely bottlenecked. Management has earmarked 5% of IPO funds for potential accretive acquisitions, likely targeting localized compute or data annotation assets to hedge this exposure.

HDIN Institutional Perspective: The "SaaS" Illusion and Working Capital Drag

Despite the market's attempt to value Deepexi as a cloud subscription proxy, the balance sheet permanently dispels the SaaS illusion. Contract Liabilities (deferred revenue) sit at an anemic $0.85 million—just 1.5% of total sales. Deepexi recognizes 98.1% of its revenue at a point-in-time upon project delivery, relying on deep operational integration (DeepexiOS) rather than financial subscription lock-in.

The fundamental risk to the equity story is not margin compression, but a severe working capital drag. In FY2025, operating cash burn widened to $27.67 million as Trade Receivables surged 85.0% to $42.80 million, materially outpacing the 70.8% revenue growth. While a 32.9% drop in inventory (unbilled contract fulfillment costs) signals legitimate project acceptance and milestone de-stocking, backend cash collections are significantly lagging. If Deepexi’s "Leads to Cash" (LTC) internal management systems fail to shorten Days Sales Outstanding (DSO), this receivables trap will force the company to prematurely drain its $99.53 million liquidity buffer to self-fund future deployments.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides institutional-grade market intelligence and forensic equity analysis. Visit us at www.hdinresearch.com for deeper cuts into global supply chains, macroeconomic pivots, and enterprise technology audits.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Labor Arbitrage Play

Deepexi’s FY2025 audit reveals a company actively transitioning away from labor-intensive project deployments toward AI-driven operational leverage. The legacy FastData segment stagnated at a 5.2% growth rate ($22.33 million), while the FastAGI Enterprise AI Solutions unit exploded by 181.5% to $35.40 million.

The "So What": This top-line rotation masks a deeper structural labor arbitrage. Deepexi expanded consolidated gross margins from 51.9% to 55.1% not through pricing power, but by deploying internal proprietary AI digital employees (FastAGI agents) to co-pilot its Forward Deployed Engineers (FDEs). By automating data governance, coding, and project management workflows, per capita productivity accelerated to $124,440 across its 464-person workforce.

Furthermore, earnings quality remains highly conservative. The headline statutory net loss of $130.03 million is a phantom accounting artifact, heavily distorted by a $102.28 million non-cash fair value loss on pre-IPO preferred shares and a 4,040% surge in Stock-Based Compensation ($16.04 million). Stripping out these frictions, the adjusted net loss narrowed by 71.4% to a mere $3.83 million. The company enforces strict R&D expensing—funneling $14.98 million entirely through the P&L—eliminating the risk of future intangible asset impairment and securing a pristine, debt-to-asset profile of 23.4% post-IPO.

Figure Deepexi Technology: 2025 Executive Performance & Al Transformation Blueprint

Supply Chain Pivot: Hybrid Infrastructure & The Silicon CeilingDeepexi operates a decentralized procurement matrix, with top-five supplier concentration strictly capped below 30%. However, management is executing a distinct hybrid compute infrastructure pivot. While OPEX for third-party cloud services surged to support Supervised Fine-Tuning (SFT) and multimodal ontology modeling, the company simultaneously aggressively scaled its physical AI server CAPEX, driving Property, Plant, and Equipment (PPE) up 77.1%.

This dual-track sourcing highlights a systemic vulnerability. While Deepexi plans to deploy $33.37 million of its IPO proceeds toward software R&D through 2030, no amount of internal capital allocation can bypass international export control laws. The company's reliance on open-source foundation models combined with an escalating need for heavy compute power exposes it directly to macro-geopolitical silicon embargoes. If physical hardware access tightens, management's ability to maintain its enterprise large model capabilities will be severely bottlenecked. Management has earmarked 5% of IPO funds for potential accretive acquisitions, likely targeting localized compute or data annotation assets to hedge this exposure.

HDIN Institutional Perspective: The "SaaS" Illusion and Working Capital Drag

Despite the market's attempt to value Deepexi as a cloud subscription proxy, the balance sheet permanently dispels the SaaS illusion. Contract Liabilities (deferred revenue) sit at an anemic $0.85 million—just 1.5% of total sales. Deepexi recognizes 98.1% of its revenue at a point-in-time upon project delivery, relying on deep operational integration (DeepexiOS) rather than financial subscription lock-in.

The fundamental risk to the equity story is not margin compression, but a severe working capital drag. In FY2025, operating cash burn widened to $27.67 million as Trade Receivables surged 85.0% to $42.80 million, materially outpacing the 70.8% revenue growth. While a 32.9% drop in inventory (unbilled contract fulfillment costs) signals legitimate project acceptance and milestone de-stocking, backend cash collections are significantly lagging. If Deepexi’s "Leads to Cash" (LTC) internal management systems fail to shorten Days Sales Outstanding (DSO), this receivables trap will force the company to prematurely drain its $99.53 million liquidity buffer to self-fund future deployments.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides institutional-grade market intelligence and forensic equity analysis. Visit us at www.hdinresearch.com for deeper cuts into global supply chains, macroeconomic pivots, and enterprise technology audits.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*