Life Sciences Giants See Diverging Margins: Thermo Fisher and 10x Genomics Offset 39% Hardware Contraction via Consumable-Driven Recurring Revenue

Date : 2026-04-14

Reading : 257

In FY2025, global life sciences corporations—anchored by Thermo Fisher (NYSE: TMO), Illumina (NASDAQ: ILMN), and 10x Genomics (NASDAQ: TXG)—executed a structural pivot away from capital equipment sales toward high-margin consumables across North America and Europe. Confronting severe U.S. CAPEX freezes and geopolitical decoupling in the Asia-Pacific region, executives utilized strategic instrument placement programs (SIPP) and reagent rentals to force cost-pass-through mechanisms. This transition definitively insulates gross margins against prolonged sales cycles, fundamentally reshaping the sector's financial architecture from hardware-centric vulnerabilities to absolute ecosystem lock-in.

Financial Health & Operational Moats: Hacking the Replacement Cycle

The 2025 audit cycle confirms a brutal macroeconomic filter: discretionary academic and basic research budgets have collapsed, while translational diagnostics and biomanufacturing remain highly inelastic. To survive systemic margin compression, sector leaders have abandoned traditional capital expenditure (CAPEX) reliance, "hacking" the hardware replacement cycle through intense workflow entrenchment.

10x Genomics (NASDAQ: TXG) provides the starkest proxy for this shift. Despite a catastrophic 39% year-over-year plunge in instrument revenue down to $56.8 million, the company salvaged its top line as high-margin spatial and single-cell consumables ballooned to represent 78.9% of total revenue. Similarly, Thermo Fisher Scientific (NYSE: TMO) absorbed a $7.30 billion instrument drag by harvesting $37.25 billion in recurring consumable and service revenues.

However, beneath this resilient surface, working capital dynamics flag impending distress for mid-tier players. Days Sales Outstanding (DSO) expansion is accelerating—Waters Corporation (NYSE: WAT) extended to 84 days, and Agilent Technologies (NYSE: A) to 72 days—signaling relaxed credit terms to pull forward sales. Furthermore, the specter of inventory de-stocking has triggered auditor interventions. Illumina’s massive $564 million net inventory balance was explicitly designated as a Critical Audit Matter (CAM), requiring subjective management judgments regarding obsolescence in an environment defined by rapid product lifecycle turnover.

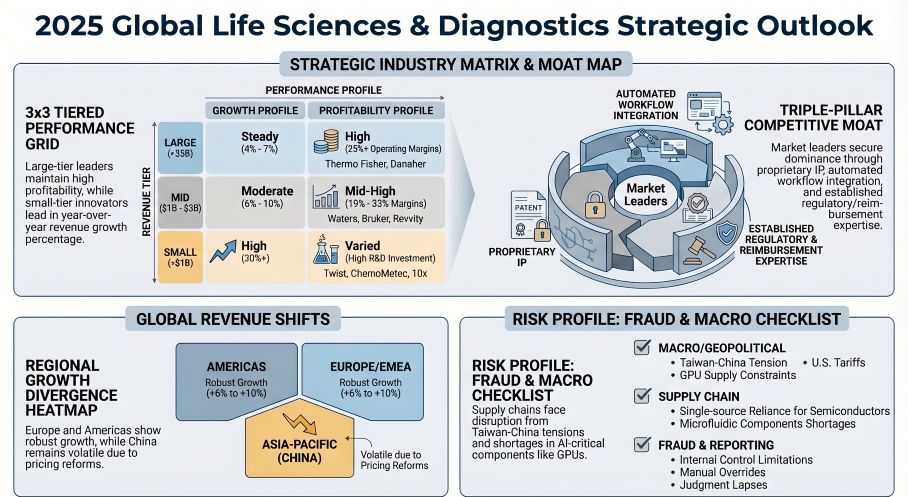

Figure 2025 Global Life Sciences & Diagnostics Strategic Outlook

Supply Chain Pivot: Geopolitical Decoupling and Manufacturing Bifurcation

Supply Chain Pivot: Geopolitical Decoupling and Manufacturing Bifurcation

The reality of the 2026 U.S. BIOSECURE Act and persistent trade tariffs has shattered the illusion of a unified global supply chain. Life sciences firms are actively executing a bifurcated manufacturing strategy: aggressive vertical integration for intellectual property-sensitive consumables, offset by the wholesale outsourcing of complex hardware to contract manufacturers like STRATEC and Hamilton Company.

Geopolitical decoupling is no longer theoretical; it is visible in hard capital reallocation. Following its inclusion on China's "List of Unreliable Entities," Illumina’s Greater China revenue contracted by $65 million, forcing immediate alterations to its Singapore-to-China importation pathways. In direct response to U.S. export controls on high-parameter flow cytometers, Cytek Biosciences (NASDAQ: CTKB) bypassed its Fremont, USA, and Wuxi, China nodes, spinning up a new manufacturing facility in Singapore in March 2025.

To optimize fixed overhead absorption, Tecan Group executed a strategic divestiture of its Morgan Hill, U.S. precision machining capacities, relocating nodes to Vietnam. Conversely, Roche (SWX: ROG) committed to a $50 billion localization initiative over five years to fortify its U.S. diagnostic manufacturing footprint. Meanwhile, domestic Chinese players like Zhejiang Tailin Bioengineering are weaponizing academic collaborations (e.g., Zhejiang University) to drive import substitution in TOC analyzers, securing customized structural parts via localized vendor lock-ins.

HDIN Institutional Perspective: The Demise of Wet-Lab Biology

The FCF-to-Net Income divergence across the sector reveals the true cost of maintaining these competitive moats. Danaher Corporation (NYSE: DHR) reported $3.60 billion in net earnings but generated a massive $7.49 billion in operating cash flow—a delta driven by $1.69 billion in intangible amortization stemming from serial, accretive acquisitions like Cytiva and Abcam. True earnings power in this sector is now dictated by cash conversion algorithms, not GAAP net income.

More critically, a forensic analysis of industry-wide human capital allocation signals a fundamental technological paradigm shift. The next three-year product cycle will not be driven by wet-lab biological discoveries, but by deterministic software engineering. Companies are disproportionately slashing fundamental R&D headcounts while heavily staffing commercial software deployment. ChemoMetec openly conceded its transition away from classical biology toward automation engineering to scale its XcytoMatic platforms.

The integration of artificial intelligence—evidenced by Revvity’s (NYSE: RVTY) Phenologic.AI and PacBio’s (NASDAQ: PACB) machine-learning data layers—transforms laboratory instruments from passive measurement tools into predictive data ecosystems. By leveraging SIPP models and reagent rentals (such as those utilized by Bio-Rad and Seer), manufacturers are successfully subsidizing hardware to extract perpetual software and consumable rents, entirely circumventing the small-cap biotech funding drought.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic intelligence and equity research firm delivering institutional-grade financial analysis and market foresight. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Hacking the Replacement Cycle

The 2025 audit cycle confirms a brutal macroeconomic filter: discretionary academic and basic research budgets have collapsed, while translational diagnostics and biomanufacturing remain highly inelastic. To survive systemic margin compression, sector leaders have abandoned traditional capital expenditure (CAPEX) reliance, "hacking" the hardware replacement cycle through intense workflow entrenchment.

10x Genomics (NASDAQ: TXG) provides the starkest proxy for this shift. Despite a catastrophic 39% year-over-year plunge in instrument revenue down to $56.8 million, the company salvaged its top line as high-margin spatial and single-cell consumables ballooned to represent 78.9% of total revenue. Similarly, Thermo Fisher Scientific (NYSE: TMO) absorbed a $7.30 billion instrument drag by harvesting $37.25 billion in recurring consumable and service revenues.

However, beneath this resilient surface, working capital dynamics flag impending distress for mid-tier players. Days Sales Outstanding (DSO) expansion is accelerating—Waters Corporation (NYSE: WAT) extended to 84 days, and Agilent Technologies (NYSE: A) to 72 days—signaling relaxed credit terms to pull forward sales. Furthermore, the specter of inventory de-stocking has triggered auditor interventions. Illumina’s massive $564 million net inventory balance was explicitly designated as a Critical Audit Matter (CAM), requiring subjective management judgments regarding obsolescence in an environment defined by rapid product lifecycle turnover.

Figure 2025 Global Life Sciences & Diagnostics Strategic Outlook

Supply Chain Pivot: Geopolitical Decoupling and Manufacturing BifurcationThe reality of the 2026 U.S. BIOSECURE Act and persistent trade tariffs has shattered the illusion of a unified global supply chain. Life sciences firms are actively executing a bifurcated manufacturing strategy: aggressive vertical integration for intellectual property-sensitive consumables, offset by the wholesale outsourcing of complex hardware to contract manufacturers like STRATEC and Hamilton Company.

Geopolitical decoupling is no longer theoretical; it is visible in hard capital reallocation. Following its inclusion on China's "List of Unreliable Entities," Illumina’s Greater China revenue contracted by $65 million, forcing immediate alterations to its Singapore-to-China importation pathways. In direct response to U.S. export controls on high-parameter flow cytometers, Cytek Biosciences (NASDAQ: CTKB) bypassed its Fremont, USA, and Wuxi, China nodes, spinning up a new manufacturing facility in Singapore in March 2025.

To optimize fixed overhead absorption, Tecan Group executed a strategic divestiture of its Morgan Hill, U.S. precision machining capacities, relocating nodes to Vietnam. Conversely, Roche (SWX: ROG) committed to a $50 billion localization initiative over five years to fortify its U.S. diagnostic manufacturing footprint. Meanwhile, domestic Chinese players like Zhejiang Tailin Bioengineering are weaponizing academic collaborations (e.g., Zhejiang University) to drive import substitution in TOC analyzers, securing customized structural parts via localized vendor lock-ins.

HDIN Institutional Perspective: The Demise of Wet-Lab Biology

The FCF-to-Net Income divergence across the sector reveals the true cost of maintaining these competitive moats. Danaher Corporation (NYSE: DHR) reported $3.60 billion in net earnings but generated a massive $7.49 billion in operating cash flow—a delta driven by $1.69 billion in intangible amortization stemming from serial, accretive acquisitions like Cytiva and Abcam. True earnings power in this sector is now dictated by cash conversion algorithms, not GAAP net income.

More critically, a forensic analysis of industry-wide human capital allocation signals a fundamental technological paradigm shift. The next three-year product cycle will not be driven by wet-lab biological discoveries, but by deterministic software engineering. Companies are disproportionately slashing fundamental R&D headcounts while heavily staffing commercial software deployment. ChemoMetec openly conceded its transition away from classical biology toward automation engineering to scale its XcytoMatic platforms.

The integration of artificial intelligence—evidenced by Revvity’s (NYSE: RVTY) Phenologic.AI and PacBio’s (NASDAQ: PACB) machine-learning data layers—transforms laboratory instruments from passive measurement tools into predictive data ecosystems. By leveraging SIPP models and reagent rentals (such as those utilized by Bio-Rad and Seer), manufacturers are successfully subsidizing hardware to extract perpetual software and consumable rents, entirely circumventing the small-cap biotech funding drought.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic intelligence and equity research firm delivering institutional-grade financial analysis and market foresight. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*