Strategic Headline: Hill & Smith (LSE: HILS) Transatlantic Divergence Drives 26.7% ROIC Amid UK Margin Compression

Date : 2026-04-14

Reading : 71

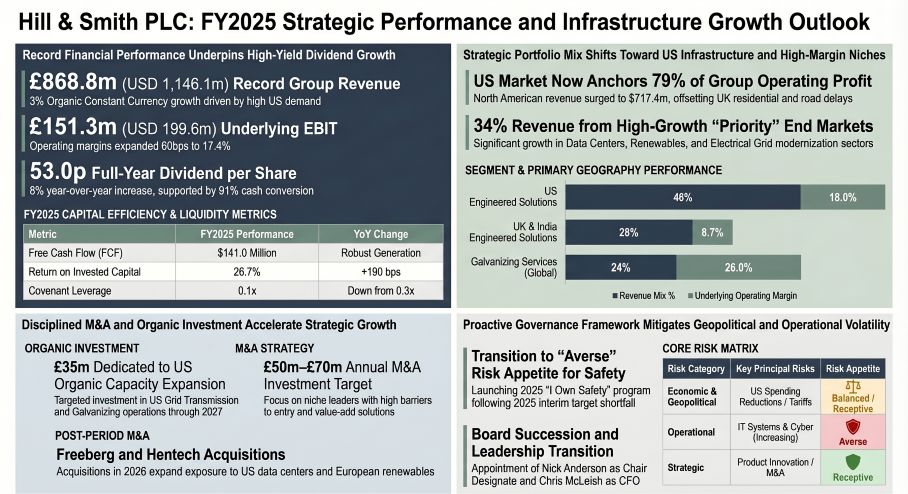

In its FY2025 audit, infrastructure manufacturing specialist Hill & Smith PLC capitalized on a structural super-cycle in North American electrical transmission and data center construction to deliver a 26.7% Return on Invested Capital (ROIC). By executing a ruthless geographic pivot away from a stagnant UK public works sector, the Group drove a 91% cash conversion rate and expanded underlying operating margins to 17.4%. This transatlantic divergence underscores a strategic transition from cyclical steel galvanizing toward high-margin, IP-protected utility solutions, effectively insulating the balance sheet from delayed UK government spending and localized demand troughs.

Financial Health & Operational Moats

Hill & Smith’s FY2025 financial architecture is defined by an aggressive shift toward premium-yielding assets, pushing its covenant Net Debt to EBITDA down to a highly conservative 0.1x. The Group generated USD 1,146.1 million in reported revenue, but the underlying narrative lies in the margin expansion driven by its US portfolio. The US Engineered Solutions segment posted an 18.0% operating margin, while US Galvanizing reached a peak of 26.0%.

This profitability is heavily fortified by structural cost-pass-through mechanisms. Because the Group’s engineered components—such as 'StormStrong' composite utility poles—represent a negligible fraction of the total system cost for multi-billion-dollar utility upgrades and AI data centers, customer price elasticity is virtually nonexistent. Consequently, the Group bypassed global raw material volatility (zinc and steel) without sacrificing volume.

Capital allocation followed a dual-track strategy. The integration of the 2024 bolt-ons (Whitlow Electric, Trident, FM Stainless) proved to be highly accretive acquisitions, accelerating exposure to the US Southeast and structural grid hardening. Conversely, management demonstrated a ruthless approach to underperforming units, swallowing a USD 17.94 million impairment to write off National Signal’s legacy off-grid solar operations, signaling a clear exit from commoditized, high-competition tech markets in favor of defensible, hard-asset infrastructure niches.

Figure Hill & Smith PLC: FY2025 Strategic Performance and Infrastructure Growth Qutlook

Supply Chain Pivot & Capital Allocation

Supply Chain Pivot & Capital Allocation

Unlike global manufacturing peers paralyzed by procurement bottlenecks, Hill & Smith recorded an active working capital optimization phase. The Group reduced closing debtor days to 59 and tightened inventory days to 69. This active inventory de-stocking was achieved while Cost of Sales remained fundamentally flat at USD 679.78 million, pointing to highly precise demand forecasting rather than defensive stockpiling.

To mitigate geopolitical disruption, the Group enforced strict dual-sourcing mandates while simultaneously monetizing the macro trend of US onshoring. The physical manufacturing footprint is actively migrating to support this localized demand. Management committed USD 46.17 million over the 2026-2027 cycle strictly for organic capacity expansion within the US network. Operational milestones include the activation of a USD 9.89 million fabrication plant in Waggaman, Louisiana for large-scale engineered supports, and the strategic consolidation of its Texas message-board operations into the La Mirada, California hub. Post-period acquisitions in March 2026—specifically Escondido-based Freeberg Industrial Fabrication for USD 36.0 million—further solidify this localized vertical integration strategy.

HDIN Institutional Perspective

The underlying catalyst for Hill & Smith’s current valuation multiplier is its conscious uncoupling from the UK government’s infrastructure timeline. The delays in the UK Government’s Road Investment Strategy 3 (RIS3) and persistent local authority budget deficits triggered acute margin compression across the UK & India Engineered Solutions segment, dragging its margin down to 8.7%. However, the localized autonomy of Hill & Smith's operating model quarantined this weakness.

From an institutional standpoint, the Group is effectively utilizing the cash flow generated by its legacy UK operations to fund aggressive Capex deployment in the US electrical and semiconductor ecosystems. Furthermore, the installation of "smart burners" and waste heat recovery systems in its Galvanizing plants drove a 19% reduction in Scope 1 and 2 emissions, ensuring alignment with 2030 sustainability benchmarks without sacrificing heavy-industrial output. While the Board must address a localized governance shortfall—female representation dropped to 25% following recent executive departures—the overarching strategy is airtight. By aligning its core M&A engine with structural megatrends (grid modernization, liquid natural gas, gigafactories) rather than cyclical residential construction, Hill & Smith has engineered a resilient, cycle-agnostic growth platform.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, corporate filings deconstruction, and macroeconomic supply chain tracking. We deliver alpha-generating insights to asset managers, private equity stakeholders, and corporate development teams globally. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats

Hill & Smith’s FY2025 financial architecture is defined by an aggressive shift toward premium-yielding assets, pushing its covenant Net Debt to EBITDA down to a highly conservative 0.1x. The Group generated USD 1,146.1 million in reported revenue, but the underlying narrative lies in the margin expansion driven by its US portfolio. The US Engineered Solutions segment posted an 18.0% operating margin, while US Galvanizing reached a peak of 26.0%.

This profitability is heavily fortified by structural cost-pass-through mechanisms. Because the Group’s engineered components—such as 'StormStrong' composite utility poles—represent a negligible fraction of the total system cost for multi-billion-dollar utility upgrades and AI data centers, customer price elasticity is virtually nonexistent. Consequently, the Group bypassed global raw material volatility (zinc and steel) without sacrificing volume.

Capital allocation followed a dual-track strategy. The integration of the 2024 bolt-ons (Whitlow Electric, Trident, FM Stainless) proved to be highly accretive acquisitions, accelerating exposure to the US Southeast and structural grid hardening. Conversely, management demonstrated a ruthless approach to underperforming units, swallowing a USD 17.94 million impairment to write off National Signal’s legacy off-grid solar operations, signaling a clear exit from commoditized, high-competition tech markets in favor of defensible, hard-asset infrastructure niches.

Figure Hill & Smith PLC: FY2025 Strategic Performance and Infrastructure Growth Qutlook

Supply Chain Pivot & Capital AllocationUnlike global manufacturing peers paralyzed by procurement bottlenecks, Hill & Smith recorded an active working capital optimization phase. The Group reduced closing debtor days to 59 and tightened inventory days to 69. This active inventory de-stocking was achieved while Cost of Sales remained fundamentally flat at USD 679.78 million, pointing to highly precise demand forecasting rather than defensive stockpiling.

To mitigate geopolitical disruption, the Group enforced strict dual-sourcing mandates while simultaneously monetizing the macro trend of US onshoring. The physical manufacturing footprint is actively migrating to support this localized demand. Management committed USD 46.17 million over the 2026-2027 cycle strictly for organic capacity expansion within the US network. Operational milestones include the activation of a USD 9.89 million fabrication plant in Waggaman, Louisiana for large-scale engineered supports, and the strategic consolidation of its Texas message-board operations into the La Mirada, California hub. Post-period acquisitions in March 2026—specifically Escondido-based Freeberg Industrial Fabrication for USD 36.0 million—further solidify this localized vertical integration strategy.

HDIN Institutional Perspective

The underlying catalyst for Hill & Smith’s current valuation multiplier is its conscious uncoupling from the UK government’s infrastructure timeline. The delays in the UK Government’s Road Investment Strategy 3 (RIS3) and persistent local authority budget deficits triggered acute margin compression across the UK & India Engineered Solutions segment, dragging its margin down to 8.7%. However, the localized autonomy of Hill & Smith's operating model quarantined this weakness.

From an institutional standpoint, the Group is effectively utilizing the cash flow generated by its legacy UK operations to fund aggressive Capex deployment in the US electrical and semiconductor ecosystems. Furthermore, the installation of "smart burners" and waste heat recovery systems in its Galvanizing plants drove a 19% reduction in Scope 1 and 2 emissions, ensuring alignment with 2030 sustainability benchmarks without sacrificing heavy-industrial output. While the Board must address a localized governance shortfall—female representation dropped to 25% following recent executive departures—the overarching strategy is airtight. By aligning its core M&A engine with structural megatrends (grid modernization, liquid natural gas, gigafactories) rather than cyclical residential construction, Hill & Smith has engineered a resilient, cycle-agnostic growth platform.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, corporate filings deconstruction, and macroeconomic supply chain tracking. We deliver alpha-generating insights to asset managers, private equity stakeholders, and corporate development teams globally. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*