Global Mobility Platforms Pivot to "Asset-Right" Autonomous Networks as Rental Duopoly Posts Massive EV Impairments

Date : 2026-04-15

Reading : 488

In the FY2025 reporting cycle, global mobility giants including Uber (NYSE: UBER), DiDi Global (OTC: DDIY), Hertz (NASDAQ: HTZ), and Avis (NASDAQ: CAR) revealed a structural divergence in capital allocation across US and APAC markets. While asset-light tech platforms achieved historic free cash flow via AI-driven dispatch algorithms and strategic third-party autonomous partnerships, traditional fleet operators suffered severe margin compression. This polarization was triggered by a systemic miscalculation of electric vehicle (EV) residual values, forcing massive non-cash impairments and fundamentally altering how the industry finances and depreciates its rolling assets.

Financial Health & Operational Moats: The Valuation Allowance Trap

The 2025 mobility landscape presents a masterclass in reading past headline GAAP net income. We are observing a severe divergence between actual Free Cash Flow (FCF) generation and highly engineered tax benefits that mask underlying unit economics.

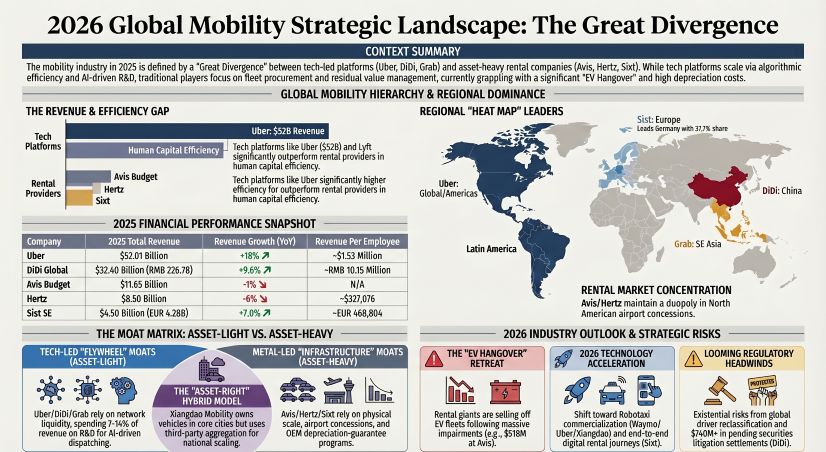

Both Uber and Lyft (NASDAQ: LYFT) triggered massive, non-cash accounting releases that artificially inflated 2025 earnings. Lyft reported $2.84 billion in net income, fundamentally driven by a $2.9 billion tax benefit from releasing a valuation allowance on U.S. deferred tax assets. Uber executed an identical maneuver, claiming a $5.0 billion income tax benefit tied to deferred tax assets in the Netherlands. However, looking at operating cash, Uber exhibits a formidable moat: it generated $9.76 billion in FCF against a mere $336 million in physical property and equipment purchases. Its scale acts as a massive cost-pass-through mechanism, insulating it from underlying fleet depreciation.

Conversely, the traditional rental sector is experiencing catastrophic negative leverage. Hertz posted a negative Adjusted Corporate EBITDA of $(339) million on $8.50 billion in revenue, driven by a 17% spike in SG&A against a 6% revenue contraction. Hertz's negative FCF is a direct result of capital drag: $10.18 billion in vehicle expenditures significantly outpaced its $8.08 billion in disposal proceeds. Meanwhile, Avis utilized subjective deferred revenue "breakage" calculations regarding customer loyalty points to strategically pull revenue forward, an accounting maneuver that warrants strict auditor scrutiny.

Figure 2026 Global Mobility Strategic Landscape

Supply Chain Pivot: Inventory De-stocking and EV Residual Collapse

Supply Chain Pivot: Inventory De-stocking and EV Residual Collapse

The defining supply chain pivot of 2025 is the violent inventory de-stocking of electric vehicles by legacy rental operators, highlighting a systemic vulnerability in residual value modeling.

Avis and Hertz fundamentally misjudged the depreciation curve of their EV fleets. To staunch the bleeding, Avis recorded a $518 million impairment charge in late 2025 to accelerate the disposal of its U.S. EV fleet, exposing the fragility of its "risk" vehicle procurement strategy. Hertz similarly absorbed $223 million in incremental net depreciation to aggressively purge EVs, reducing them to less than 10% of its U.S. operating fleet. The rental duopoly is now aggressively retreating to the safety of OEM "program" vehicles—where manufacturers guarantee the depreciation rate—which accounted for 26% of Hertz's 2025 purchases and 16% of Avis's active fleet.

In stark contrast, APAC operators are utilizing vertical integration and dynamic actuarial adjustments to mitigate fleet risk. Lotte Rental managed residual exposure by extending the estimated useful life of its auto rental assets from 5 years to 7 years—lowering 2025 depreciation expenses by 6.8 billion KRW—and pushing off-lease inventory through its proprietary Anseong Auto Auction. This closed-loop cycle enables Lotte to feed highly profitable B2C retail and export markets, fundamentally insulating its margins from external wholesale auction volatility.

The "Asset-Right" Autonomous Roadmap

The collective action in mobility R&D has shifted aggressively from cash-burning, in-house full-stack development to "Asset-Right" autonomous partnerships. Companies blending deep proprietary AI integration with targeted capital expenditures are winning the tech-led efficiency race.

* The Aggregator Model: Uber and Lyft rely heavily on Waymo to deploy autonomous networks. While Uber's $52 billion data monopoly attracts third-party robotaxi networks without the heavy R&D CAPEX, Lyft is uniquely vulnerable. Lacking proprietary technology, if third-party AVs scale slower than expected, Lyft's reliance on manual driver incentives (which drove an 11% increase in its 2025 cost of revenue) will result in terminal margin compression.

* The Hybrid Ecosystem: Xiangdao Mobility (backed by SAIC Motor) exemplifies optimal capital efficiency. By outsourcing vehicle manufacturing to SAIC and L4 algorithms to Momenta, Xiangdao focuses purely on dispatch logic. This allowed them to secure an autonomous driving pilot license in Shanghai in July 2025 with zero in-vehicle safety operators, actively feeding traditional human ride-hailing data into Momenta's L4 training models.

* The Algorithmic Super-App: DiDi Global continues to absorb massive direct R&D, deploying its proprietary L4 software via its Voyager subsidiary and partnering with GAC Aion for mass production. Coupled with its generative AI LLMs—which automated complex dispute resolutions and slashed driver onboarding times by 95%—DiDi expanded gross margins while servicing over 6.7 million registered EVs.

HDIN Institutional Perspective

From an institutional standpoint, the mobility sector has hit a structural inflection point where physical metal is becoming a liability and digital code is the ultimate moat. The U.S. regulatory environment, particularly the July 2025 One Big Beautiful Bill Act (OBBBA) which eliminated federal EV tax credits, abruptly destroyed the fleet acquisition economics for rental operators. This exogenous shock forced the mass impairments we are currently witnessing.

Moving forward into 2026, we anticipate operators like Grab (NASDAQ: GRAB) will pursue accretive acquisitions—similar to its $55 million minority stake in remote-driving company Vay—to navigate fragmented regulatory ceilings in Southeast Asia. For legacy rentals, the failure to upgrade legacy IT systems and shift toward asset-light network utilization presents an existential business continuity risk. The market will aggressively discount any operator holding un-hedged, physical EV risk on its balance sheet.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis. For more actionable insights on macroeconomic trends and sector-specific deep dives, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Valuation Allowance Trap

The 2025 mobility landscape presents a masterclass in reading past headline GAAP net income. We are observing a severe divergence between actual Free Cash Flow (FCF) generation and highly engineered tax benefits that mask underlying unit economics.

Both Uber and Lyft (NASDAQ: LYFT) triggered massive, non-cash accounting releases that artificially inflated 2025 earnings. Lyft reported $2.84 billion in net income, fundamentally driven by a $2.9 billion tax benefit from releasing a valuation allowance on U.S. deferred tax assets. Uber executed an identical maneuver, claiming a $5.0 billion income tax benefit tied to deferred tax assets in the Netherlands. However, looking at operating cash, Uber exhibits a formidable moat: it generated $9.76 billion in FCF against a mere $336 million in physical property and equipment purchases. Its scale acts as a massive cost-pass-through mechanism, insulating it from underlying fleet depreciation.

Conversely, the traditional rental sector is experiencing catastrophic negative leverage. Hertz posted a negative Adjusted Corporate EBITDA of $(339) million on $8.50 billion in revenue, driven by a 17% spike in SG&A against a 6% revenue contraction. Hertz's negative FCF is a direct result of capital drag: $10.18 billion in vehicle expenditures significantly outpaced its $8.08 billion in disposal proceeds. Meanwhile, Avis utilized subjective deferred revenue "breakage" calculations regarding customer loyalty points to strategically pull revenue forward, an accounting maneuver that warrants strict auditor scrutiny.

Figure 2026 Global Mobility Strategic Landscape

Supply Chain Pivot: Inventory De-stocking and EV Residual CollapseThe defining supply chain pivot of 2025 is the violent inventory de-stocking of electric vehicles by legacy rental operators, highlighting a systemic vulnerability in residual value modeling.

Avis and Hertz fundamentally misjudged the depreciation curve of their EV fleets. To staunch the bleeding, Avis recorded a $518 million impairment charge in late 2025 to accelerate the disposal of its U.S. EV fleet, exposing the fragility of its "risk" vehicle procurement strategy. Hertz similarly absorbed $223 million in incremental net depreciation to aggressively purge EVs, reducing them to less than 10% of its U.S. operating fleet. The rental duopoly is now aggressively retreating to the safety of OEM "program" vehicles—where manufacturers guarantee the depreciation rate—which accounted for 26% of Hertz's 2025 purchases and 16% of Avis's active fleet.

In stark contrast, APAC operators are utilizing vertical integration and dynamic actuarial adjustments to mitigate fleet risk. Lotte Rental managed residual exposure by extending the estimated useful life of its auto rental assets from 5 years to 7 years—lowering 2025 depreciation expenses by 6.8 billion KRW—and pushing off-lease inventory through its proprietary Anseong Auto Auction. This closed-loop cycle enables Lotte to feed highly profitable B2C retail and export markets, fundamentally insulating its margins from external wholesale auction volatility.

The "Asset-Right" Autonomous Roadmap

The collective action in mobility R&D has shifted aggressively from cash-burning, in-house full-stack development to "Asset-Right" autonomous partnerships. Companies blending deep proprietary AI integration with targeted capital expenditures are winning the tech-led efficiency race.

* The Aggregator Model: Uber and Lyft rely heavily on Waymo to deploy autonomous networks. While Uber's $52 billion data monopoly attracts third-party robotaxi networks without the heavy R&D CAPEX, Lyft is uniquely vulnerable. Lacking proprietary technology, if third-party AVs scale slower than expected, Lyft's reliance on manual driver incentives (which drove an 11% increase in its 2025 cost of revenue) will result in terminal margin compression.

* The Hybrid Ecosystem: Xiangdao Mobility (backed by SAIC Motor) exemplifies optimal capital efficiency. By outsourcing vehicle manufacturing to SAIC and L4 algorithms to Momenta, Xiangdao focuses purely on dispatch logic. This allowed them to secure an autonomous driving pilot license in Shanghai in July 2025 with zero in-vehicle safety operators, actively feeding traditional human ride-hailing data into Momenta's L4 training models.

* The Algorithmic Super-App: DiDi Global continues to absorb massive direct R&D, deploying its proprietary L4 software via its Voyager subsidiary and partnering with GAC Aion for mass production. Coupled with its generative AI LLMs—which automated complex dispute resolutions and slashed driver onboarding times by 95%—DiDi expanded gross margins while servicing over 6.7 million registered EVs.

HDIN Institutional Perspective

From an institutional standpoint, the mobility sector has hit a structural inflection point where physical metal is becoming a liability and digital code is the ultimate moat. The U.S. regulatory environment, particularly the July 2025 One Big Beautiful Bill Act (OBBBA) which eliminated federal EV tax credits, abruptly destroyed the fleet acquisition economics for rental operators. This exogenous shock forced the mass impairments we are currently witnessing.

Moving forward into 2026, we anticipate operators like Grab (NASDAQ: GRAB) will pursue accretive acquisitions—similar to its $55 million minority stake in remote-driving company Vay—to navigate fragmented regulatory ceilings in Southeast Asia. For legacy rentals, the failure to upgrade legacy IT systems and shift toward asset-light network utilization presents an existential business continuity risk. The market will aggressively discount any operator holding un-hedged, physical EV risk on its balance sheet.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis. For more actionable insights on macroeconomic trends and sector-specific deep dives, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*