Energy Storage Sector Hits Deflationary Trough: Global Integrators Pivot to AI-Software Moats Amid 31% Hardware Price Collapse

Date : 2026-04-15

Reading : 866

Following the FY2025 audit cycle, tier-one Energy Storage System (ESS) manufacturers and global integrators (CATL, Tesla, Fluence) are executing a structural pivot away from commoditized hardware capacity. In response to a brutal 31% YoY deflation in global battery prices and the geopolitical shock of the U.S. OBBBA legislation, these entities are deploying heavy capital into asset-light AI trading platforms, closed-loop recycling infrastructure, and localized supply chains. This margin-protective strategy aims to capture recurring grid-arbitrage revenues while insulating operations from severe inventory devaluation and tariff volatility.

Financial Health & Operational Moats: Navigating the "Volume-Price Divergence"

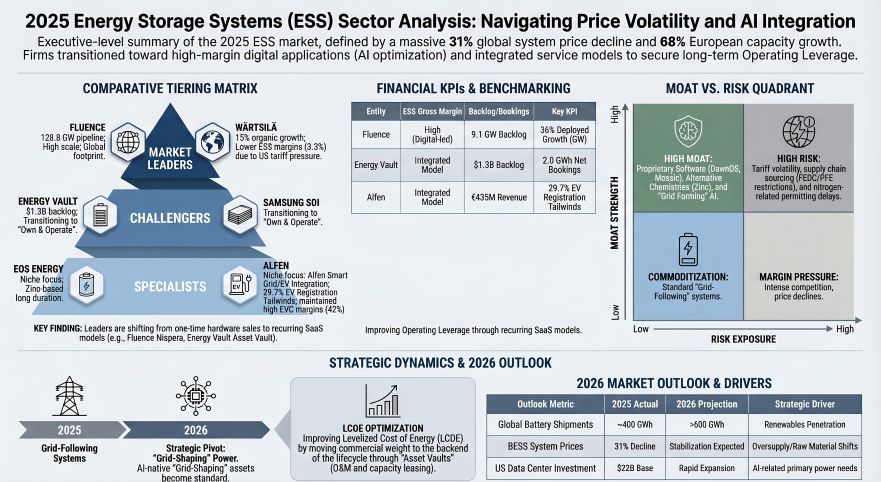

The FY2025 filings reveal an industry trapped in a stark volume-price divergence. While AI data centers and grid modernization have pushed utility-scale deployment past 200 GWh, the 31% collapse in Battery Energy Storage System (BESS) pricing has triggered severe margin compression across the sector.

Operating leverage is heavily bifurcated. Scale giants like Tesla (NASDAQ: TSLA) and CATL (SZSE: 300750) maintained fortress balance sheets, delivering ESS gross margins of 29.8% and 26.71%, respectively. Tesla’s margins expanded directly due to automated throughput at its Shanghai Megafactory and localized procurement buffering tariff shocks. CATL leveraged its $3.08 billion R&D expenditure—strictly maintaining a 0% R&D capitalization rate—to rapidly launch the 9MWh "TENER Stack," securing a 30% unit-area density premium over mid-tier competitors.

Conversely, emerging Long-Duration Energy Storage (LDES) developers like ESS Inc. (NYSE: GWH) and Eos Energy (NASDAQ: EOSE) are marooned in the commercial "valley of death." Reporting catastrophic gross margins of -1748% and -125.9% respectively, these hardware innovators suffer from severe diseconomies of scale and an inability to enforce cost-pass-through mechanisms in a deflationary tape.

The most alarming distress signal flashes from the mid-tier cell integrators. Pylontech (SHA: 688063) reported a massive 120.31% YoY surge in inventory, flagging acute write-down risks as aggressive inventory de-stocking cycles fail to keep pace with plummeting spot lithium prices. Simultaneously, Clou Electronics (SZSE: 002121) faces an elongated cash conversion cycle, with Accounts Receivable ballooning to 32% of total revenue, exposing the firm to critical bad debt risks amidst macroeconomic tightening.

Figure 2025 Energy Storage Systems (ESS) Sector Analysis: Navigating Price Volatility and Al Integration

Supply Chain Pivot: OBBBA Compliance and the End of Borderless Procurement

Supply Chain Pivot: OBBBA Compliance and the End of Borderless Procurement

The passage of the July 2025 U.S. "One Big Beautiful Bill Act" (OBBBA) effectively shattered the illusion of a borderless clean energy supply chain. By aggressively modifying the Inflation Reduction Act (IRA) and introducing rigid Prohibited Foreign Entity (PFE) and FEOC restrictions, Western integrators are rapidly domesticating procurement to secure Investment Tax Credits (ITCs) and Advanced Manufacturing Production Credits (AMPC).

To circumvent U.S. Section 301 tariffs, asset-light integrators such as Fluence (NASDAQ: FLNC) and Energy Vault (NYSE: NRGV) are systematically regionalizing their assembly. Energy Vault’s strategic agreement to source U.S.-manufactured sodium-ion from Peak Energy exemplifies the compliance-driven shift. Eos Energy is capitalizing on this geopolitical friction by moving to a 100% U.S.-sourced zinc supply chain, explicitly targeting the IRA Domestic Content Bonus to artificially lower its Levelized Cost of Energy (LCOE).

In response, CATL is bypassing Western trade barriers entirely through vertical integration and closed-loop material sovereignty. The Chinese giant directed heavy CapEx into its Yichang Brunp Integrated Battery Material Industrial Park (USD 2.30 billion CapEx), recycling a verified 210,000 tons of waste batteries in FY2025 to extract 24,000 tons of regenerated lithium salts. This physical asset base provides CATL with a verified, carbon-neutral supply chain that effectively nullifies regional trace-mineral embargoes.

HDIN Institutional Perspective: The Software Arbitrage Cycle

HDIN Research assesses that the ESS sector has decoupled from the passive, mandate-driven "Renewable + Storage" attachments of the early 2020s. We are entering the Software Arbitrage Cycle. Hardware is increasingly treated as a low-margin loss leader designed to capture high-margin, sticky SaaS contracts and Virtual Power Plant (VPP) operations.

Pure integrators are commanding peak human capital efficiency. Energy Vault generated $1.37 million in revenue per employee in FY2025 by shifting its Go-To-Market strategy from hardware sales to "Own & Operate" asset control. By deploying the *Vault-Bidder* AI platform, the company autonomous trades energy on wholesale markets. Similarly, Fluence’s *Mosaic* platform drove its Services Assets Under Management (AUM) up 30.2% YoY to 5.6 GW.

These digital applications carry near-zero marginal costs, structurally elevating long-term gross margins. The ultimate competitive moat in 2026 will not be defined by incremental improvements in lithium-ion density, but by the algorithmic capability to extract maximum financial yield from grid volatility. Companies lacking an AI-driven Energy Management System (EMS) will either face hostile, accretive acquisitions by established IPPs or complete insolvency.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global provider of strategic market intelligence, institutional equity research, and macroeconomic forecasting. Delivering unvarnished truths and rigorous financial stress testing, our analysts equip institutional investors with the data architecture required to navigate complex geopolitical and technological transitions. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Navigating the "Volume-Price Divergence"

The FY2025 filings reveal an industry trapped in a stark volume-price divergence. While AI data centers and grid modernization have pushed utility-scale deployment past 200 GWh, the 31% collapse in Battery Energy Storage System (BESS) pricing has triggered severe margin compression across the sector.

Operating leverage is heavily bifurcated. Scale giants like Tesla (NASDAQ: TSLA) and CATL (SZSE: 300750) maintained fortress balance sheets, delivering ESS gross margins of 29.8% and 26.71%, respectively. Tesla’s margins expanded directly due to automated throughput at its Shanghai Megafactory and localized procurement buffering tariff shocks. CATL leveraged its $3.08 billion R&D expenditure—strictly maintaining a 0% R&D capitalization rate—to rapidly launch the 9MWh "TENER Stack," securing a 30% unit-area density premium over mid-tier competitors.

Conversely, emerging Long-Duration Energy Storage (LDES) developers like ESS Inc. (NYSE: GWH) and Eos Energy (NASDAQ: EOSE) are marooned in the commercial "valley of death." Reporting catastrophic gross margins of -1748% and -125.9% respectively, these hardware innovators suffer from severe diseconomies of scale and an inability to enforce cost-pass-through mechanisms in a deflationary tape.

The most alarming distress signal flashes from the mid-tier cell integrators. Pylontech (SHA: 688063) reported a massive 120.31% YoY surge in inventory, flagging acute write-down risks as aggressive inventory de-stocking cycles fail to keep pace with plummeting spot lithium prices. Simultaneously, Clou Electronics (SZSE: 002121) faces an elongated cash conversion cycle, with Accounts Receivable ballooning to 32% of total revenue, exposing the firm to critical bad debt risks amidst macroeconomic tightening.

Figure 2025 Energy Storage Systems (ESS) Sector Analysis: Navigating Price Volatility and Al Integration

Supply Chain Pivot: OBBBA Compliance and the End of Borderless ProcurementThe passage of the July 2025 U.S. "One Big Beautiful Bill Act" (OBBBA) effectively shattered the illusion of a borderless clean energy supply chain. By aggressively modifying the Inflation Reduction Act (IRA) and introducing rigid Prohibited Foreign Entity (PFE) and FEOC restrictions, Western integrators are rapidly domesticating procurement to secure Investment Tax Credits (ITCs) and Advanced Manufacturing Production Credits (AMPC).

To circumvent U.S. Section 301 tariffs, asset-light integrators such as Fluence (NASDAQ: FLNC) and Energy Vault (NYSE: NRGV) are systematically regionalizing their assembly. Energy Vault’s strategic agreement to source U.S.-manufactured sodium-ion from Peak Energy exemplifies the compliance-driven shift. Eos Energy is capitalizing on this geopolitical friction by moving to a 100% U.S.-sourced zinc supply chain, explicitly targeting the IRA Domestic Content Bonus to artificially lower its Levelized Cost of Energy (LCOE).

In response, CATL is bypassing Western trade barriers entirely through vertical integration and closed-loop material sovereignty. The Chinese giant directed heavy CapEx into its Yichang Brunp Integrated Battery Material Industrial Park (USD 2.30 billion CapEx), recycling a verified 210,000 tons of waste batteries in FY2025 to extract 24,000 tons of regenerated lithium salts. This physical asset base provides CATL with a verified, carbon-neutral supply chain that effectively nullifies regional trace-mineral embargoes.

HDIN Institutional Perspective: The Software Arbitrage Cycle

HDIN Research assesses that the ESS sector has decoupled from the passive, mandate-driven "Renewable + Storage" attachments of the early 2020s. We are entering the Software Arbitrage Cycle. Hardware is increasingly treated as a low-margin loss leader designed to capture high-margin, sticky SaaS contracts and Virtual Power Plant (VPP) operations.

Pure integrators are commanding peak human capital efficiency. Energy Vault generated $1.37 million in revenue per employee in FY2025 by shifting its Go-To-Market strategy from hardware sales to "Own & Operate" asset control. By deploying the *Vault-Bidder* AI platform, the company autonomous trades energy on wholesale markets. Similarly, Fluence’s *Mosaic* platform drove its Services Assets Under Management (AUM) up 30.2% YoY to 5.6 GW.

These digital applications carry near-zero marginal costs, structurally elevating long-term gross margins. The ultimate competitive moat in 2026 will not be defined by incremental improvements in lithium-ion density, but by the algorithmic capability to extract maximum financial yield from grid volatility. Companies lacking an AI-driven Energy Management System (EMS) will either face hostile, accretive acquisitions by established IPPs or complete insolvency.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global provider of strategic market intelligence, institutional equity research, and macroeconomic forecasting. Delivering unvarnished truths and rigorous financial stress testing, our analysts equip institutional investors with the data architecture required to navigate complex geopolitical and technological transitions. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*