Bus Titans Pivot to Software-Defined Ecosystems as Daimler and Volvo Target 13% Services CAGR Amid $565M ZEV Infrastructure Realignment

Date : 2026-04-15

Reading : 221

In the FY2025 audit cycle, global commercial vehicle OEMs (Daimler Truck, Volvo Group, TRATON SE, IVECO, and Yutong) are aggressively recalibrating capital expenditures from pure-play hardware manufacturing toward high-margin Fleet-as-a-Service (FaaS) ecosystems. Driven by severe regulatory policy ceilings in the US and Europe, Western incumbents are executing multi-billion-dollar joint ventures to de-risk localized supply chains, while Chinese OEMs pivot to emerging markets to offset domestic cyclicality. This structural shift effectively permanently decouples terminal enterprise value from cyclical hardware procurement, moving the sector toward a recurring-revenue, Software-Defined Vehicle (SDV) operational model.

Financial Health & Operational Moats: The Quality of Earnings Divergence

An audit of the FY2025 cohort reveals a stark divergence between top-line reporting and actual cash conversion, separating true operational moats from aggressive accounting.

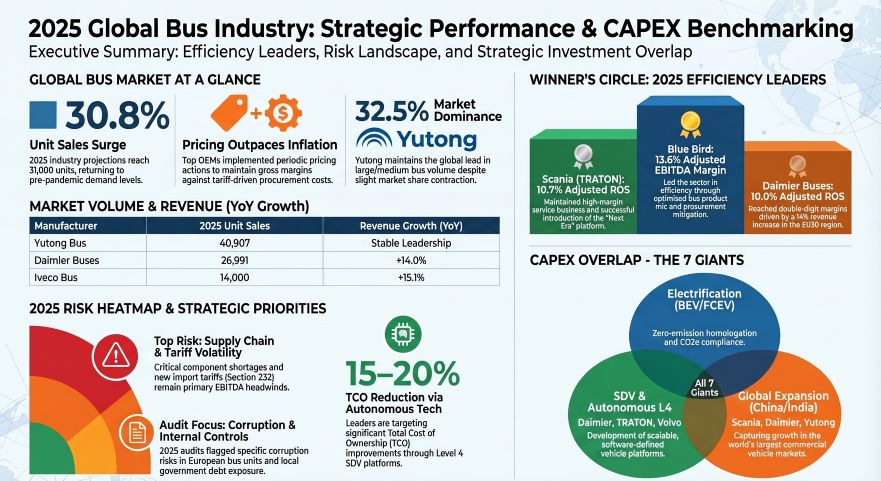

Daimler Truck (ETR: DTG) executed a masterclass in human capital productivity, generating an industry-leading $541,440 per employee. By aggressively utilizing cost-pass-through mechanisms and maintaining strict pricing discipline, Daimler defended its 4.12% net margin despite volume compression in North American and European delivery cycles. Conversely, IVECO Group (BIT: IVG) demonstrated the cohort’s most resilient profit quality; despite a sector-low 2.15% net profit margin, IVECO posted an exceptional Operating Cash Flow to Net Income (OCF/NI) ratio of 3.84x. This cash-backed earnings profile underscores highly conservative working capital management and an efficient restructuring of its FPT Industrial division.

However, severe red flags emerged in the East. Yutong Bus (SHA: 600066) reported an industry-leading 13.41% net profit margin, fueled by a 38.87% YoY surge in overseas sales. Yet, its OCF collapsed by 55.67%, resulting in a precarious 0.58x OCF/NI ratio. The "So What" here is critical: Yutong’s aggressive export pivot to emerging markets (e.g., Kazakhstan, Ethiopia) is generating substantial paper profits but trapping liquid cash in surging overseas receivables and uncollected inventory. Similarly, TRATON SE (ETR: 8TRA) posted a 0.58x ratio, confirming structural inventory de-stocking issues and weak incoming orders at its International Motors and VWTB brands.

Figure 2025 Clobal Bus industry: Strategic Performance & CAPEX Benchmarking

Supply Chain Pivot: Localized Capacity and ZEV Asset Recalibration

Supply Chain Pivot: Localized Capacity and ZEV Asset Recalibration

The 2025 supply chain narrative is defined by the dismantling of globalized procurement in favor of localized, vertically integrated capacity. Faced with U.S. Section 232 tariffs and European geopolitical volatility, Western OEMs executed aggressive CapEx recalibrations.

Due to a macro-level under-investment in power grids and subsidized charging infrastructure, early Battery Electric Vehicle (BEV) capacity has become a financial liability. Volvo Group (STO: VOLV-B) was forced to recognize a $459 million (SEK 4.5 billion) negative operating impact to write down stranded BEV assets, while Daimler Truck recorded a $246 million derecognition of capitalized development costs. TRATON similarly terminated a Class 8 BEV project at International Motors, resulting in a $113 million impairment.

To share the capital burden of the zero-emission transition, incumbents are abandoning unilateral R&D in favor of highly accretive joint ventures. Daimler, Cummins, and PACCAR launched the *Amplify Cell Technologies* JV to onshore battery production in the US. In Europe, TRATON internalized module manufacturing via a $282.65 million injection into its Nuremberg facility. In contrast, Volvo divested its 70% stake in Chinese construction equipment maker SDLG for $810 million, deliberately shrinking emerging-market exposure to redeploy capital into high-margin mature market fortifications, including a new heavy-duty plant in Mexico.

Expanding the Moat: Software-Defined Vehicles and Fleet-as-a-Service

The ultimate competitive moat in 2025 is no longer mechanical engineering—it is the operational lock-in of the Software-Defined Vehicle (SDV). Hardware margins face permanent compression, forcing OEMs to capture the Total Cost of Ownership (TCO) via recurring service revenues.

Volvo and Daimler explicitly engineered a high-switching-cost ecosystem via their *Coretura* joint venture. By developing an open, standardized commercial operating system, they are establishing the "iOS of commercial trucking." Once fleet operators integrate enterprise resource planning (ERP) and telemetry with the Coretura OS, the operational friction of switching to a non-compliant OEM becomes prohibitively high. This digital monetization is highly lucrative: Volvo’s services division generated SEK 124 billion ($12.64 billion) in 2025, securing a 13% CAGR over five years and acting as a primary earnings stabilizer against a 5% drop in vehicle deliveries.

Simultaneously, mid-cap players are leveraging Fleet-as-a-Service (FaaS) to bypass the high capital hurdles of electric transit. Blue Bird Corp (NASDAQ: BLBD) launched the *Clean Bus Solutions* JV with Generate Capital to offer municipalities turnkey operations—bundling the physical bus, proprietary charging hardware, and financing into a single operational expenditure (OpEx) contract. By owning the depot infrastructure, Blue Bird completely insulates itself from competitor churn.

HDIN Institutional Perspective: The Policy Ceiling Trough

From a macroeconomic standpoint, the commercial vehicle sector has officially hit a cyclical "Policy Ceiling." In Europe, Regulation 2024/1610 (mandating 45% CO2 reductions by 2030 or severe $4,805 per gram penalties) acts as a hard cap on internal combustion margin expansion. In North America, the politicization of EPA grants—where Blue Bird saw Clean School Bus Program win-rates dilute from 21.7% to 15.3% as funding structures shifted—proves that reliance on government CapEx subsidies is an unsustainable growth model.

The strategic takeaway for institutional capital is clear: pure-play electric vehicle hardware manufacturing is a commoditized, low-margin trap. The terminal winners of the 2026–2030 cycle will be OEMs like Volvo and Daimler that strategically extend highly profitable multi-fuel legacy platforms to finance the $565 million *Milence* charging JV and the *Coretura* software stack. By the time infrastructure parity is achieved, these incumbents will have monopolized the data networks and physical charging corridors, reducing hardware assemblers to low-margin ecosystem participants.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and institutional advisory firm. We specialize in deep-dive financial audits, supply chain forensics, and geopolitical macro-analysis for the industrials and mobility sectors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Quality of Earnings Divergence

An audit of the FY2025 cohort reveals a stark divergence between top-line reporting and actual cash conversion, separating true operational moats from aggressive accounting.

Daimler Truck (ETR: DTG) executed a masterclass in human capital productivity, generating an industry-leading $541,440 per employee. By aggressively utilizing cost-pass-through mechanisms and maintaining strict pricing discipline, Daimler defended its 4.12% net margin despite volume compression in North American and European delivery cycles. Conversely, IVECO Group (BIT: IVG) demonstrated the cohort’s most resilient profit quality; despite a sector-low 2.15% net profit margin, IVECO posted an exceptional Operating Cash Flow to Net Income (OCF/NI) ratio of 3.84x. This cash-backed earnings profile underscores highly conservative working capital management and an efficient restructuring of its FPT Industrial division.

However, severe red flags emerged in the East. Yutong Bus (SHA: 600066) reported an industry-leading 13.41% net profit margin, fueled by a 38.87% YoY surge in overseas sales. Yet, its OCF collapsed by 55.67%, resulting in a precarious 0.58x OCF/NI ratio. The "So What" here is critical: Yutong’s aggressive export pivot to emerging markets (e.g., Kazakhstan, Ethiopia) is generating substantial paper profits but trapping liquid cash in surging overseas receivables and uncollected inventory. Similarly, TRATON SE (ETR: 8TRA) posted a 0.58x ratio, confirming structural inventory de-stocking issues and weak incoming orders at its International Motors and VWTB brands.

Figure 2025 Clobal Bus industry: Strategic Performance & CAPEX Benchmarking

Supply Chain Pivot: Localized Capacity and ZEV Asset RecalibrationThe 2025 supply chain narrative is defined by the dismantling of globalized procurement in favor of localized, vertically integrated capacity. Faced with U.S. Section 232 tariffs and European geopolitical volatility, Western OEMs executed aggressive CapEx recalibrations.

Due to a macro-level under-investment in power grids and subsidized charging infrastructure, early Battery Electric Vehicle (BEV) capacity has become a financial liability. Volvo Group (STO: VOLV-B) was forced to recognize a $459 million (SEK 4.5 billion) negative operating impact to write down stranded BEV assets, while Daimler Truck recorded a $246 million derecognition of capitalized development costs. TRATON similarly terminated a Class 8 BEV project at International Motors, resulting in a $113 million impairment.

To share the capital burden of the zero-emission transition, incumbents are abandoning unilateral R&D in favor of highly accretive joint ventures. Daimler, Cummins, and PACCAR launched the *Amplify Cell Technologies* JV to onshore battery production in the US. In Europe, TRATON internalized module manufacturing via a $282.65 million injection into its Nuremberg facility. In contrast, Volvo divested its 70% stake in Chinese construction equipment maker SDLG for $810 million, deliberately shrinking emerging-market exposure to redeploy capital into high-margin mature market fortifications, including a new heavy-duty plant in Mexico.

Expanding the Moat: Software-Defined Vehicles and Fleet-as-a-Service

The ultimate competitive moat in 2025 is no longer mechanical engineering—it is the operational lock-in of the Software-Defined Vehicle (SDV). Hardware margins face permanent compression, forcing OEMs to capture the Total Cost of Ownership (TCO) via recurring service revenues.

Volvo and Daimler explicitly engineered a high-switching-cost ecosystem via their *Coretura* joint venture. By developing an open, standardized commercial operating system, they are establishing the "iOS of commercial trucking." Once fleet operators integrate enterprise resource planning (ERP) and telemetry with the Coretura OS, the operational friction of switching to a non-compliant OEM becomes prohibitively high. This digital monetization is highly lucrative: Volvo’s services division generated SEK 124 billion ($12.64 billion) in 2025, securing a 13% CAGR over five years and acting as a primary earnings stabilizer against a 5% drop in vehicle deliveries.

Simultaneously, mid-cap players are leveraging Fleet-as-a-Service (FaaS) to bypass the high capital hurdles of electric transit. Blue Bird Corp (NASDAQ: BLBD) launched the *Clean Bus Solutions* JV with Generate Capital to offer municipalities turnkey operations—bundling the physical bus, proprietary charging hardware, and financing into a single operational expenditure (OpEx) contract. By owning the depot infrastructure, Blue Bird completely insulates itself from competitor churn.

HDIN Institutional Perspective: The Policy Ceiling Trough

From a macroeconomic standpoint, the commercial vehicle sector has officially hit a cyclical "Policy Ceiling." In Europe, Regulation 2024/1610 (mandating 45% CO2 reductions by 2030 or severe $4,805 per gram penalties) acts as a hard cap on internal combustion margin expansion. In North America, the politicization of EPA grants—where Blue Bird saw Clean School Bus Program win-rates dilute from 21.7% to 15.3% as funding structures shifted—proves that reliance on government CapEx subsidies is an unsustainable growth model.

The strategic takeaway for institutional capital is clear: pure-play electric vehicle hardware manufacturing is a commoditized, low-margin trap. The terminal winners of the 2026–2030 cycle will be OEMs like Volvo and Daimler that strategically extend highly profitable multi-fuel legacy platforms to finance the $565 million *Milence* charging JV and the *Coretura* software stack. By the time infrastructure parity is achieved, these incumbents will have monopolized the data networks and physical charging corridors, reducing hardware assemblers to low-margin ecosystem participants.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and institutional advisory firm. We specialize in deep-dive financial audits, supply chain forensics, and geopolitical macro-analysis for the industrials and mobility sectors. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*