Heavy Engine Giants Pivot to AI Data Center Power as Top 5 Players Absorb Multi-Billion Regulatory Friction

Date : 2026-04-15

Reading : 245

Global heavy equipment manufacturers (NYSE: CAT, NYSE: CMI, STO: VOLV-B) are aggressively reallocating FY2025 CapEx from cyclical freight trucking into stationary power generation across North America and Europe. Driven by explosive AI infrastructure demands and punitive internal combustion emissions frameworks, OEMs are executing a structural supply chain pivot. By nearshoring manufacturing and leveraging cost-pass-through mechanisms to offset "Green Steel" inflation, these industrial giants are insulating their operating margins against escalating tariff threats and severe macroeconomic volatility ahead of 2026.

Financial Health & Operational Moats: The Data Center 'Alpha' and Cash Conversion

The commercial vehicle and heavy machinery industries are inherently cyclical, but the 2025 audit cycle reveals a definitive decoupling strategy: the servitization of business models and an aggressive pivot toward hyperscale data center infrastructure.

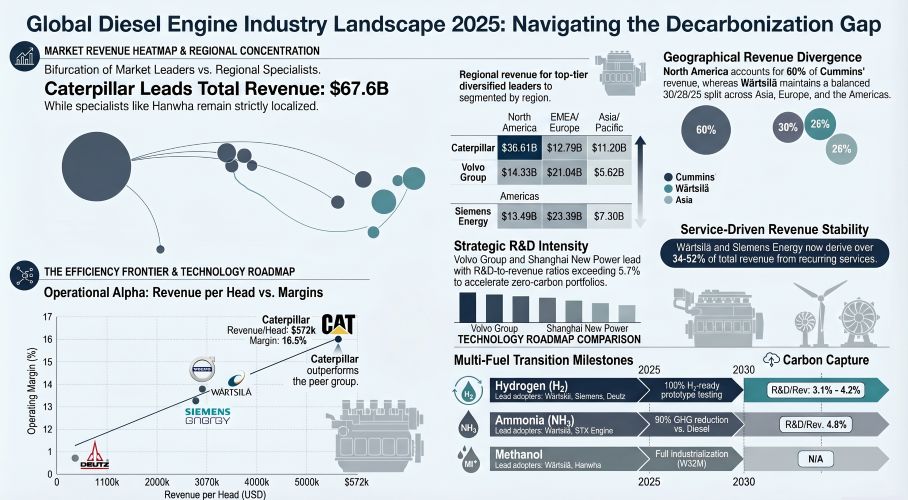

Traditional trucking and off-highway markets are experiencing a severe freight recession. Cummins Inc. (NYSE: CMI) explicitly warned of weak North American truck demand extending into 2026, while Shanghai New Power’s core market remains paralyzed by domestic overcapacity. However, the true operational moat now lies in the ability to capture the inelastic energy demand of generative AI. Caterpillar (NYSE: CAT) posted a 32% year-over-year surge in its Power Generation segment, reaching $10.27 billion, primarily driven by data center operators bypassing constrained electrical grids.

This structural shift has triggered an unprecedented wave of cash conversion. Siemens Energy (ETR: ENR) reported a massive 151% surge in pre-tax Free Cash Flow to $5.27 billion, overwhelmingly fueled by customer advance payments in its Gas Services and Grid Technologies segments. Wärtsilä (HEL: WRT1V) similarly achieved an all-time high operating cash flow of $1.81 billion. These multi-year service contracts and capacity reservations provide an insurmountable liquidity buffer against inventory de-stocking in their legacy hardware divisions.

Conversely, aggressive capitalization of unproven "green" ventures is destroying shareholder equity. The market collapse of early-stage hydrogen applications forced Cummins to record a $458 million impairment within its Accelera segment. Financial health in 2026 demands a ruthless culling of premature green tech in favor of highly accretive, fuel-flexible assets (e.g., Wärtsilä's W32M methanol engine and Siemens' H2-ready gas turbines).

Figure Global Diesel Engine Industry Landscape 2025: Navigating the Decarbonization Gap

Supply Chain Pivot: Vertical Integration and The Decoupling Premium

Supply Chain Pivot: Vertical Integration and The Decoupling Premium

Geopolitical fragmentation and trade protectionism have killed the globally optimized, just-in-time supply chain. To defend against a projected $2.6 billion tariff hit (as modeled by Caterpillar), OEMs are executing a hard pivot toward regionalized value chains and defensive vertical integration.

Volvo Group (STO: VOLV-B) currently operates with the most resilient global footprint in the cohort. Rather than reacting to retaliatory tariffs, Volvo is proactively establishing a new heavy-duty truck factory in Mexico to ring-fence its 29% North American revenue base. Meanwhile, European mid-caps are pursuing accretive acquisitions to claw back engineering value-add lost to electrification. Deutz AG (ETR: DEZ) acquired a 50% stake in HJS Emission Technology, structurally integrating exhaust aftertreatment to stabilize pricing and mitigate sub-tier supplier shocks.

A hidden margin compression threat lies deep within these reconfigured supply chains: the mandated transition to "Green Steel." Volvo’s commitment to the First Movers Coalition (integrating low-carbon steel into its FH truck frames) and Siemens Energy’s GreenerTower wind initiatives are structurally elevating the Cost of Goods Sold (COGS). To prevent these ESG mandates from destroying gross margins, companies are enforcing rigorous cost-pass-through mechanisms, utilizing index-linked supply contracts to force the end-user to absorb the premium.

HDIN Institutional Perspective: Regulatory Ceilings and The Electrification Friction

The narrative that heavy machinery is voluntarily leading the climate transition is a fundamental misreading of the balance sheet. Decarbonization is not a strategic choice; it is a rigid "Policy Ceiling" enforced by crippling financial penalties.

Cummins’ $2.0 billion EPA/CARB civil settlement and Volvo’s historic SEK 7 billion emissions component provision demonstrate that the operational risk of maintaining legacy diesel platforms has eclipsed the R&D cost of replacing them. This regulatory friction is forcing a bifurcated CapEx cycle. While Caterpillar and Siemens Energy expand their R&D testing infrastructure (such as Wärtsilä’s 35% capacity expansion at its Sustainable Technology Hub in Vaasa, Finland), they are simultaneously bleeding capital out of traditional internal combustion engine (ICE) manufacturing.

We are observing a massive divergence in asset intensity. Pure-play operators like Steyr Motors (0.93x asset intensity) face an existential threat in the 2-5 year horizon. If military and marine applications transition to zero-emission drives faster than anticipated, mid-tier manufacturers will experience a catastrophic loss of engineering value-add. The ultimate survivors of the 2026 cycle will not be those with the largest engine displacements, but those who successfully bridge the electrification gap via modular architectures, massive aftermarket service lock-ins, and an absolute dominance over localized, tariff-proof supply nodes.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier global financial intelligence and strategic advisory firm. We specialize in deep-tier fundamental analysis, unraveling complex supply chain dynamics, and identifying macroeconomic alpha for institutional investors, private equity, and corporate strategy boards across the heavy industrial, energy, and technology sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Data Center 'Alpha' and Cash Conversion

The commercial vehicle and heavy machinery industries are inherently cyclical, but the 2025 audit cycle reveals a definitive decoupling strategy: the servitization of business models and an aggressive pivot toward hyperscale data center infrastructure.

Traditional trucking and off-highway markets are experiencing a severe freight recession. Cummins Inc. (NYSE: CMI) explicitly warned of weak North American truck demand extending into 2026, while Shanghai New Power’s core market remains paralyzed by domestic overcapacity. However, the true operational moat now lies in the ability to capture the inelastic energy demand of generative AI. Caterpillar (NYSE: CAT) posted a 32% year-over-year surge in its Power Generation segment, reaching $10.27 billion, primarily driven by data center operators bypassing constrained electrical grids.

This structural shift has triggered an unprecedented wave of cash conversion. Siemens Energy (ETR: ENR) reported a massive 151% surge in pre-tax Free Cash Flow to $5.27 billion, overwhelmingly fueled by customer advance payments in its Gas Services and Grid Technologies segments. Wärtsilä (HEL: WRT1V) similarly achieved an all-time high operating cash flow of $1.81 billion. These multi-year service contracts and capacity reservations provide an insurmountable liquidity buffer against inventory de-stocking in their legacy hardware divisions.

Conversely, aggressive capitalization of unproven "green" ventures is destroying shareholder equity. The market collapse of early-stage hydrogen applications forced Cummins to record a $458 million impairment within its Accelera segment. Financial health in 2026 demands a ruthless culling of premature green tech in favor of highly accretive, fuel-flexible assets (e.g., Wärtsilä's W32M methanol engine and Siemens' H2-ready gas turbines).

Figure Global Diesel Engine Industry Landscape 2025: Navigating the Decarbonization Gap

Supply Chain Pivot: Vertical Integration and The Decoupling PremiumGeopolitical fragmentation and trade protectionism have killed the globally optimized, just-in-time supply chain. To defend against a projected $2.6 billion tariff hit (as modeled by Caterpillar), OEMs are executing a hard pivot toward regionalized value chains and defensive vertical integration.

Volvo Group (STO: VOLV-B) currently operates with the most resilient global footprint in the cohort. Rather than reacting to retaliatory tariffs, Volvo is proactively establishing a new heavy-duty truck factory in Mexico to ring-fence its 29% North American revenue base. Meanwhile, European mid-caps are pursuing accretive acquisitions to claw back engineering value-add lost to electrification. Deutz AG (ETR: DEZ) acquired a 50% stake in HJS Emission Technology, structurally integrating exhaust aftertreatment to stabilize pricing and mitigate sub-tier supplier shocks.

A hidden margin compression threat lies deep within these reconfigured supply chains: the mandated transition to "Green Steel." Volvo’s commitment to the First Movers Coalition (integrating low-carbon steel into its FH truck frames) and Siemens Energy’s GreenerTower wind initiatives are structurally elevating the Cost of Goods Sold (COGS). To prevent these ESG mandates from destroying gross margins, companies are enforcing rigorous cost-pass-through mechanisms, utilizing index-linked supply contracts to force the end-user to absorb the premium.

HDIN Institutional Perspective: Regulatory Ceilings and The Electrification Friction

The narrative that heavy machinery is voluntarily leading the climate transition is a fundamental misreading of the balance sheet. Decarbonization is not a strategic choice; it is a rigid "Policy Ceiling" enforced by crippling financial penalties.

Cummins’ $2.0 billion EPA/CARB civil settlement and Volvo’s historic SEK 7 billion emissions component provision demonstrate that the operational risk of maintaining legacy diesel platforms has eclipsed the R&D cost of replacing them. This regulatory friction is forcing a bifurcated CapEx cycle. While Caterpillar and Siemens Energy expand their R&D testing infrastructure (such as Wärtsilä’s 35% capacity expansion at its Sustainable Technology Hub in Vaasa, Finland), they are simultaneously bleeding capital out of traditional internal combustion engine (ICE) manufacturing.

We are observing a massive divergence in asset intensity. Pure-play operators like Steyr Motors (0.93x asset intensity) face an existential threat in the 2-5 year horizon. If military and marine applications transition to zero-emission drives faster than anticipated, mid-tier manufacturers will experience a catastrophic loss of engineering value-add. The ultimate survivors of the 2026 cycle will not be those with the largest engine displacements, but those who successfully bridge the electrification gap via modular architectures, massive aftermarket service lock-ins, and an absolute dominance over localized, tariff-proof supply nodes.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier global financial intelligence and strategic advisory firm. We specialize in deep-tier fundamental analysis, unraveling complex supply chain dynamics, and identifying macroeconomic alpha for institutional investors, private equity, and corporate strategy boards across the heavy industrial, energy, and technology sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*