Wetouch Technology Advances Vertical Integration with $14.4M Chengdu CAPEX as Free Cash Flow Surges 783% in FY2025 Audit

Date : 2026-04-16

Reading : 66

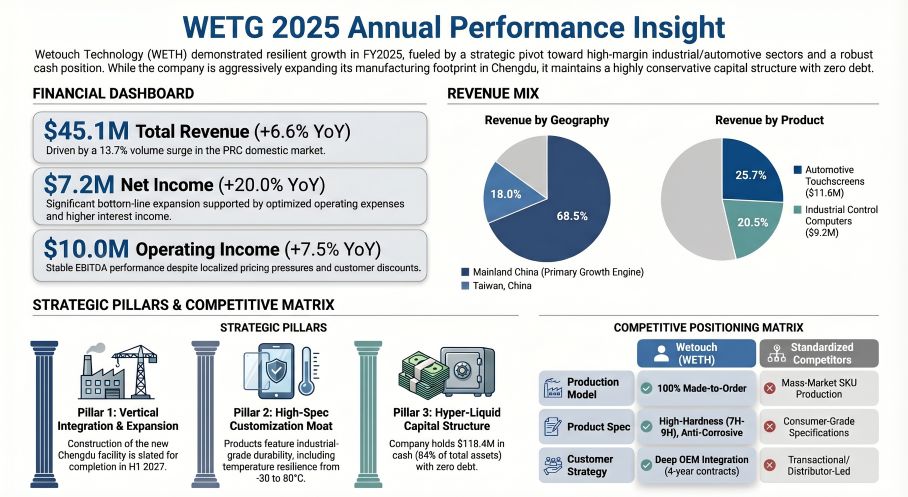

Wetouch Technology Inc. reported $45.14 million in FY2025 revenue, driven by a strategic pivot toward premium automotive and POS capacitive touchscreens across Mainland China. Executing from its Meishan City base, the zero-debt manufacturer is deploying a $14.4 million CAPEX into a new Wenjiang District, Chengdu facility to transition from component supplier to fully integrated machine assembler by H1 2027. While working capital normalization triggered a 783% surge in Free Cash Flow to $7.07 million, the company’s structural governance—characterized by an 81.7% top-five customer concentration and zero executive equity alignment—presents a highly polarized, binary risk profile for institutional allocators.

Financial Health & Operational Moats: The Liquidity and Agency Paradox

Wetouch’s FY2025 balance sheet is an anomaly in the capital-intensive hardware sector: it is hyper-liquid and fundamentally unleveraged. Cash and cash equivalents stand at an astronomical $118.36 million, representing 84.1% of total assets, supported by a 38.9x current ratio and zero interest-bearing debt following the retirement of convertible notes in FY2024.

The most material operational shift in FY2025 was the structural resolution of the prior year's working capital drag. Days Sales Outstanding (DSO) compressed from 64 to 56 days, unlocking trapped liquidity and reversing a distressed 0.18x cash conversion ratio into a highly robust 1.03x ($7.39 million OCF against $7.16 million Net Income).

The "So What": Despite this cash fortress, management exhibits a severe agency misalignment. CEO Zongyi Lian and CFO Xing Tang hold negligible-to-zero equity, and the board has explicitly ruled out dividend distributions. Rather than deploying capital toward accretive acquisitions or shareholder returns, cash is fully isolated for internal expenditures. Without stock-based incentives to drive market capitalization, the $118 million cash hoard serves purely as a defensive moat against cyclical margin compression, effectively stranding retail and institutional equity investors from the underlying cash generation.

Figure WETG 2025 Annual Performance Insight

Supply Chain Pivot: Make-to-Order Agility vs. Feedstock Exposure

Supply Chain Pivot: Make-to-Order Agility vs. Feedstock Exposure

Operating exclusively within the 7.0 to 42-inch projected capacitive touchscreen segment, Wetouch eschews standard consumer SKUs in favor of a 100% direct-to-OEM, custom-engineered framework.

This strict "made-to-order" posture structurally immunizes the firm from the severe inventory de-stocking cycles currently plaguing the broader consumer electronics and semiconductor display sectors. Procurement of critical Indium Tin Oxide (ITO) glass and panels is executed purely on a spot purchase-order basis. While this avoids long-term vendor lock-in (top four suppliers account for an evenly distributed 46.1% of volume), it leaves the company entirely exposed to upstream commodity volatility.

Because Wetouch relies on just five clients for 81.7% of its revenue, the firm possesses extremely fragile cost-pass-through mechanisms. If geopolitical frictions or supply chain bottlenecks spike ITO feedstock prices, Wetouch must absorb the hit to its 31.8% gross margin to prevent catastrophic volume defection from its highly concentrated OEM base.

To break this commoditization cycle, the firm is utilizing its liquidity for deep vertical integration. The $14.4 million CAPEX dedicated to the new Medicine City (Technology Park) facility in Wenjiang District, Chengdu, is not merely for volume expansion. The capitalized blueprints include a dedicated "touch machine construction area," signaling a strategic migration down the value chain. By moving from fabricating raw GG (Glass-Glass) and GFF (Glass-Film-Film) components to assembling fully integrated hardware units, Wetouch aims to deepen OEM switching costs and protect its blended ASPs.

HDIN Institutional Perspective: Navigating the B2B Cyclical Trough

Wetouch’s FY2025 geographic and segmental divergences provide a clear proxy for the broader industrial hardware cycle. Domestic China volume expanded by 13.7% (anchored by an $11.63M surge in automotive displays), effectively masking a 6.0% international volume contraction driven by a trough in the global gaming touchscreen vertical.

However, the institutional overhang is governed by un-remediated regulatory risks. The auditor's flag regarding Material Weaknesses in Internal Controls (specifically a lack of U.S. GAAP-competent personnel) remains a glaring liability. Furthermore, Wetouch's operational footprint requires navigating the rigid PRC Labor Contract Law, which mandates seniority-based rather than performance-based headcount reductions. In the event of a macro demand shock, this regulatory friction strips management of the agility to rapidly cut operating expenses, heightening the risk of operating leverage turning violently negative. Combined with the tightening CSRC compliance mandates for overseas-listed entities and the looming threat of HFCAA scrutiny, Wetouch’s operational execution is persistently shadowed by jurisdictional vulnerability.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, delivering rigorous, fundamentally driven analysis of corporate filings, capital expenditures, and supply chain dynamics. For more insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Liquidity and Agency Paradox

Wetouch’s FY2025 balance sheet is an anomaly in the capital-intensive hardware sector: it is hyper-liquid and fundamentally unleveraged. Cash and cash equivalents stand at an astronomical $118.36 million, representing 84.1% of total assets, supported by a 38.9x current ratio and zero interest-bearing debt following the retirement of convertible notes in FY2024.

The most material operational shift in FY2025 was the structural resolution of the prior year's working capital drag. Days Sales Outstanding (DSO) compressed from 64 to 56 days, unlocking trapped liquidity and reversing a distressed 0.18x cash conversion ratio into a highly robust 1.03x ($7.39 million OCF against $7.16 million Net Income).

The "So What": Despite this cash fortress, management exhibits a severe agency misalignment. CEO Zongyi Lian and CFO Xing Tang hold negligible-to-zero equity, and the board has explicitly ruled out dividend distributions. Rather than deploying capital toward accretive acquisitions or shareholder returns, cash is fully isolated for internal expenditures. Without stock-based incentives to drive market capitalization, the $118 million cash hoard serves purely as a defensive moat against cyclical margin compression, effectively stranding retail and institutional equity investors from the underlying cash generation.

Figure WETG 2025 Annual Performance Insight

Supply Chain Pivot: Make-to-Order Agility vs. Feedstock ExposureOperating exclusively within the 7.0 to 42-inch projected capacitive touchscreen segment, Wetouch eschews standard consumer SKUs in favor of a 100% direct-to-OEM, custom-engineered framework.

This strict "made-to-order" posture structurally immunizes the firm from the severe inventory de-stocking cycles currently plaguing the broader consumer electronics and semiconductor display sectors. Procurement of critical Indium Tin Oxide (ITO) glass and panels is executed purely on a spot purchase-order basis. While this avoids long-term vendor lock-in (top four suppliers account for an evenly distributed 46.1% of volume), it leaves the company entirely exposed to upstream commodity volatility.

Because Wetouch relies on just five clients for 81.7% of its revenue, the firm possesses extremely fragile cost-pass-through mechanisms. If geopolitical frictions or supply chain bottlenecks spike ITO feedstock prices, Wetouch must absorb the hit to its 31.8% gross margin to prevent catastrophic volume defection from its highly concentrated OEM base.

To break this commoditization cycle, the firm is utilizing its liquidity for deep vertical integration. The $14.4 million CAPEX dedicated to the new Medicine City (Technology Park) facility in Wenjiang District, Chengdu, is not merely for volume expansion. The capitalized blueprints include a dedicated "touch machine construction area," signaling a strategic migration down the value chain. By moving from fabricating raw GG (Glass-Glass) and GFF (Glass-Film-Film) components to assembling fully integrated hardware units, Wetouch aims to deepen OEM switching costs and protect its blended ASPs.

HDIN Institutional Perspective: Navigating the B2B Cyclical Trough

Wetouch’s FY2025 geographic and segmental divergences provide a clear proxy for the broader industrial hardware cycle. Domestic China volume expanded by 13.7% (anchored by an $11.63M surge in automotive displays), effectively masking a 6.0% international volume contraction driven by a trough in the global gaming touchscreen vertical.

However, the institutional overhang is governed by un-remediated regulatory risks. The auditor's flag regarding Material Weaknesses in Internal Controls (specifically a lack of U.S. GAAP-competent personnel) remains a glaring liability. Furthermore, Wetouch's operational footprint requires navigating the rigid PRC Labor Contract Law, which mandates seniority-based rather than performance-based headcount reductions. In the event of a macro demand shock, this regulatory friction strips management of the agility to rapidly cut operating expenses, heightening the risk of operating leverage turning violently negative. Combined with the tightening CSRC compliance mandates for overseas-listed entities and the looming threat of HFCAA scrutiny, Wetouch’s operational execution is persistently shadowed by jurisdictional vulnerability.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, delivering rigorous, fundamentally driven analysis of corporate filings, capital expenditures, and supply chain dynamics. For more insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.