OriginClear Attempts 'Water-as-a-Service' Pivot as FY2025 Core Equipment Revenue Surges 54.6%

Date : 2026-04-16

Reading : 68

Clearwater-based OriginClear, Inc. (OTC: OCLN) reported a 54.6% YoY revenue surge to $6.81 million in its FY2025 audit, driven entirely by its Sherman, Texas manufacturing hub. Despite top-line growth, extreme client concentration—with 62.2% of commercial billings tied to a single buyer—triggered severe gross margin compression down to 23.8%. The enterprise is currently navigating a high-risk structural pivot toward a capital-intensive "Water On Demand" (DBOO) managed services model, which generated $0 in FY2025. Compounding these operational hurdles, the firm is battling a crippling $19.04 million working capital deficit and the Q2 2026 death of foundational CEO T. Riggs Eckelberry.

Financial Health & Operational Moats: The Illusion of Top-Line Growth

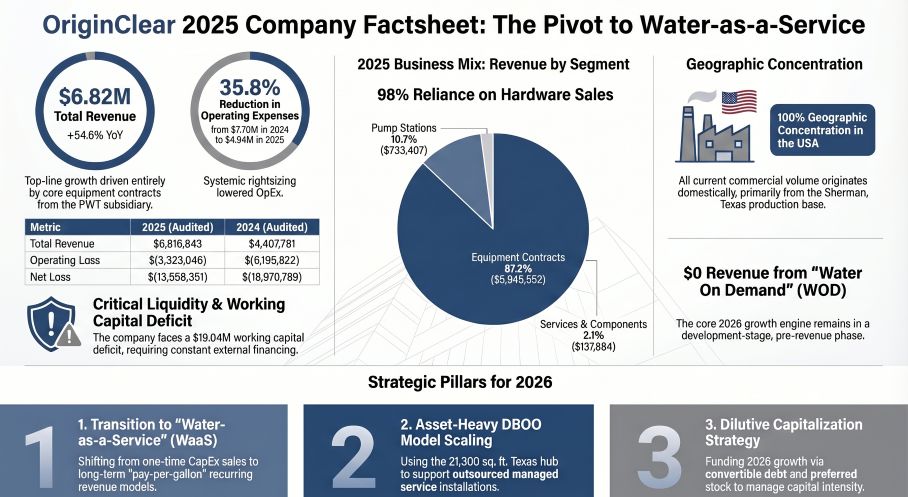

While OriginClear’s 54.6% top-line expansion appears robust on paper, a rigorous audit of the underlying revenue architecture reveals systemic vulnerabilities. Nearly 98% of the $6.81 million revenue is anchored in low-frequency, one-time CapEx equipment contracts via its Progressive Water Treatment (PWT) subsidiary.

This growth was explicitly penalized by margin compression. Gross margins contracted from 34.1% in 2024 to 23.8% in FY2025. This degradation is a direct symptom of buy-side concentration; with a single entity dictating over 62% of revenue, OriginClear lacks the pricing power necessary to execute cost-pass-through mechanisms against subcontractor and component inflation.

Below the line, the enterprise is structurally insolvent. Operating cash flow (OCF) remains persistently negative at $(3.58) million, forcing the company into a toxic capitalization loop. To maintain liquidity, OriginClear relies on heavily dilutive financing, carrying $2.61 million in convertible promissory notes and a staggering $12.13 million in volatile derivative liabilities. The resulting $(28.38) million shareholders' deficit justifies the "Going Concern" warning issued by independent auditor M&K CPAS, PLLC.

Figure OriginClear 2025 Company Factsheet: The Pivot to Water-as-a-Service

Supply Chain Pivot: Retreating to the Texas Fortress and IP Divestiture

Supply Chain Pivot: Retreating to the Texas Fortress and IP Divestiture

OriginClear’s operational footprint is now entirely consolidated within its 21,300-square-foot leased fabrication facility in Sherman, Texas. The supply chain matrix exhibits moderate concentration, with five major vendors representing 39.7% of total expenses, though management reports sufficient supplier diversification to prevent inventory de-stocking or production bottlenecks.

Strategically, FY2025 marked a period of aggressive asset rightsizing. Driven by chronic unprofitability (a dismal 3.87% gross margin), the Board executed a complete wind-down of the Modular Water Systems (MWS) division under ASC 205-20. Crucially, this exit resulted in net-negative intellectual property growth, as all core MWS patents were released back to their original inventor, Dan Early.

With $0 allocated to internal R&D in FY2025, OriginClear functions strictly as an equipment integrator rather than a proprietary technology incubator. Its remaining IP moat is heavily skewed toward branding, securing trademarks for "$H2O" and "WATER ON DEMAND" to support its pivot, alongside an unconsolidated 50/50 joint venture (Block40X) targeting Bitcoin mining in Wyoming.

HDIN Institutional Perspective: The Capital Intensity Trap of DBOO

OriginClear is attempting to execute a classic "hardware-to-services" narrative shift, transitioning from a CapEx equipment manufacturer to an outsourced "Water as a Service" (WaaS) provider through its Water On Demand (WOD) unit. Using a Design-Build-Own-Operate (DBOO) framework, the company intends to absorb the upfront capital costs of decentralized water infrastructure and charge clients a recurring, pay-per-gallon fee.

However, the unit economics of this pivot present an existential mismatch. A DBOO model requires immense, upfront balance sheet capacity. OriginClear generated $0 in WOD revenue in FY2025 and carries a $(19.04) million working capital deficit. Transforming into an infrastructure financier without organic cash generation forces the firm to fund localized CapEx through perpetual, hyper-dilutive equity and preferred stock issuances.

Furthermore, the abrupt Q2 2026 passing of CEO T. Riggs Eckelberry and the subsequent elevation of Interim CEO Cory Mertes creates a critical execution vacuum. Navigating a pivot that fundamentally alters the firm's risk profile—transferring utilization risks and third-party operational liabilities onto OCLN’s balance sheet—requires ironclad institutional confidence. Without immediate, non-toxic capital injections, the Water On Demand strategy remains a theoretical narrative rather than an accretive reality.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier independent market intelligence and institutional equity research firm, delivering unvarnished, data-driven financial analysis on micro and macro market trends. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Illusion of Top-Line Growth

While OriginClear’s 54.6% top-line expansion appears robust on paper, a rigorous audit of the underlying revenue architecture reveals systemic vulnerabilities. Nearly 98% of the $6.81 million revenue is anchored in low-frequency, one-time CapEx equipment contracts via its Progressive Water Treatment (PWT) subsidiary.

This growth was explicitly penalized by margin compression. Gross margins contracted from 34.1% in 2024 to 23.8% in FY2025. This degradation is a direct symptom of buy-side concentration; with a single entity dictating over 62% of revenue, OriginClear lacks the pricing power necessary to execute cost-pass-through mechanisms against subcontractor and component inflation.

Below the line, the enterprise is structurally insolvent. Operating cash flow (OCF) remains persistently negative at $(3.58) million, forcing the company into a toxic capitalization loop. To maintain liquidity, OriginClear relies on heavily dilutive financing, carrying $2.61 million in convertible promissory notes and a staggering $12.13 million in volatile derivative liabilities. The resulting $(28.38) million shareholders' deficit justifies the "Going Concern" warning issued by independent auditor M&K CPAS, PLLC.

Figure OriginClear 2025 Company Factsheet: The Pivot to Water-as-a-Service

Supply Chain Pivot: Retreating to the Texas Fortress and IP DivestitureOriginClear’s operational footprint is now entirely consolidated within its 21,300-square-foot leased fabrication facility in Sherman, Texas. The supply chain matrix exhibits moderate concentration, with five major vendors representing 39.7% of total expenses, though management reports sufficient supplier diversification to prevent inventory de-stocking or production bottlenecks.

Strategically, FY2025 marked a period of aggressive asset rightsizing. Driven by chronic unprofitability (a dismal 3.87% gross margin), the Board executed a complete wind-down of the Modular Water Systems (MWS) division under ASC 205-20. Crucially, this exit resulted in net-negative intellectual property growth, as all core MWS patents were released back to their original inventor, Dan Early.

With $0 allocated to internal R&D in FY2025, OriginClear functions strictly as an equipment integrator rather than a proprietary technology incubator. Its remaining IP moat is heavily skewed toward branding, securing trademarks for "$H2O" and "WATER ON DEMAND" to support its pivot, alongside an unconsolidated 50/50 joint venture (Block40X) targeting Bitcoin mining in Wyoming.

HDIN Institutional Perspective: The Capital Intensity Trap of DBOO

OriginClear is attempting to execute a classic "hardware-to-services" narrative shift, transitioning from a CapEx equipment manufacturer to an outsourced "Water as a Service" (WaaS) provider through its Water On Demand (WOD) unit. Using a Design-Build-Own-Operate (DBOO) framework, the company intends to absorb the upfront capital costs of decentralized water infrastructure and charge clients a recurring, pay-per-gallon fee.

However, the unit economics of this pivot present an existential mismatch. A DBOO model requires immense, upfront balance sheet capacity. OriginClear generated $0 in WOD revenue in FY2025 and carries a $(19.04) million working capital deficit. Transforming into an infrastructure financier without organic cash generation forces the firm to fund localized CapEx through perpetual, hyper-dilutive equity and preferred stock issuances.

Furthermore, the abrupt Q2 2026 passing of CEO T. Riggs Eckelberry and the subsequent elevation of Interim CEO Cory Mertes creates a critical execution vacuum. Navigating a pivot that fundamentally alters the firm's risk profile—transferring utilization risks and third-party operational liabilities onto OCLN’s balance sheet—requires ironclad institutional confidence. Without immediate, non-toxic capital injections, the Water On Demand strategy remains a theoretical narrative rather than an accretive reality.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier independent market intelligence and institutional equity research firm, delivering unvarnished, data-driven financial analysis on micro and macro market trends. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.