Military Microdisplay Supply Chain Shifts: Kopin Accelerates European Pivot as FY2025 Defense Revenue Contracts 29%

Date : 2026-04-16

Reading : 97

Kopin Corporation (NASDAQ: KOPN) has initiated a radical supply chain restructuring across its Westborough, Massachusetts and Dalgety Bay, Scotland facilities. As revealed in its Fiscal 2025 Annual Report, a 29% contraction in core defense revenue triggered a $15.5 million operating cash burn. To circumvent trans-Pacific geopolitical risks and satisfy strict U.S. Department of Defense mandates, Kopin is actively migrating its OLED deposition operations from mainland Chinese foundries to European partners. Bolstered by a $15.4 million Pentagon IBAS grant, Kopin is pivoting from commoditized components toward sovereign Application Specific Optical Solutions (ASOS).

Financial Health & Operational Moats: The GAAP Illusion

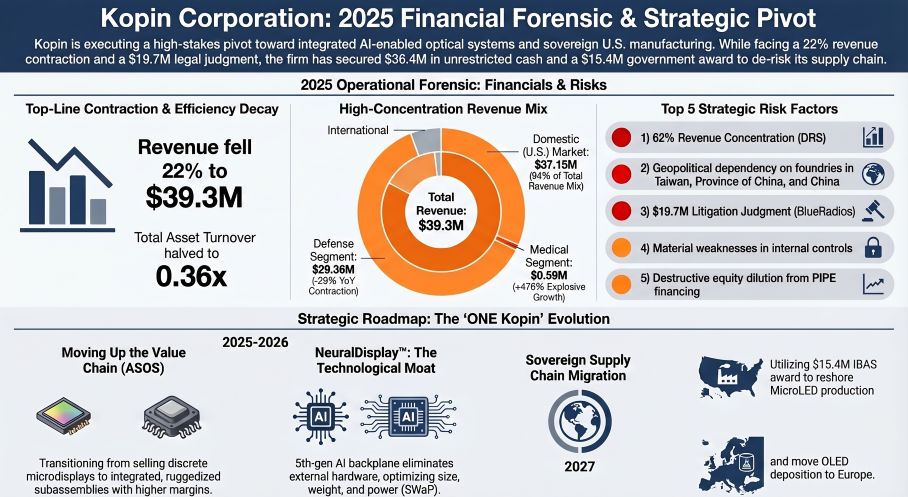

A forensic audit of Kopin’s 2025 financials reveals a highly divergent corporate profile characterized by severe top-line pressure and an optical illusion of GAAP profitability. Total revenue contracted by 21.9% to $39.32 million, largely dictated by aggressive inventory de-stocking of legacy thermal weapon sights by Kopin's primary defense prime, DRS Network & Imaging Systems (which commands a perilous 62% customer concentration).

While the income statement broadcasts a positive Net Income of $2.6 million, this is entirely an accounting artifact. The bottom line was artificially inflated by an $11.1 million non-cash gain on the deconsolidation of Kopin Europe Ltd. and a $5.1 million reversal related to the BlueRadios litigation accrual. In reality, core operations bled $15.5 million in cash. The company faced distinct margin compression, with product gross margins deteriorating from 17.0% to 15.8%. This compression was compounded by lower overhead absorption and the absence of agile cost-pass-through mechanisms in its fixed-price military contracts, culminating in a nearly $1.0 million inventory obsolescence write-down.

Despite these operational cash drains, Kopin's technological moat remains aggressively funded. Eschewing full vertical integration to maintain its "fab-lite" structure, the company directed a highly intensive 25.8% of its revenue ($10.1 million) into R&D. This capital allocation is strictly ring-fenced for proprietary IP generation, notably the 5th-generation NeuralDisplay™—a software-defined, AI-enabled backplane with bi-directional sensing that fundamentally reduces Size, Weight, and Power (SWaP) parameters for tactical AR/VR headsets. Rather than pursuing external accretive acquisitions, management has utilized heavy, albeit necessary, equity dilution (expanding shares from 156.1 million to 176.9 million via a $38.1 million PIPE) to fortify a $36.4 million unrestricted cash runway through mid-2027.

Supply Chain Pivot: Reshoring and the European Hedge

Kopin's most critical strategic maneuver in 2025 is its aggressive supply chain realignment, driven by the escalating vulnerabilities of its legacy trans-Pacific dependencies. Historically reliant on a single foundry in Taiwan (Province of China) for AMLCD circuits and mainland Chinese foundries for OLED deposition, Kopin’s exposure to geopolitical shocks and U.S. tariff regimes is severe.

To execute on the Pentagon's sovereign source-of-origin requirements, Kopin is actively transitioning its critical OLED deposition phases to European foundries. This geographic migration is not merely a risk mitigation tactic; it is structurally integrated with its market expansion. The $15.0 million strategic investment from European defense contractor Theon International Plc—which acquired a 49% stake in Kopin Europe Ltd.—serves as a direct pipeline into localized NATO defense procurements, effectively creating a dual-hemisphere defense ecosystem.

Simultaneously, domestic capital expenditures surged 76% to $1.44 million, heavily weighted toward implementing automated camera inspection systems at the Westborough hub. This automation aims to replace human defect inspection, an operational necessity to reverse current margin deterioration and prepare for higher-volume ASOS assembly.

HDIN Institutional Perspective

Kopin’s 2025 audit signals a broader cyclical trough for legacy defense optical components, exposing the violent "bullwhip effect" inherent in custom military subassembly manufacturing. Lacking the protective buffer of long-term, non-cancellable purchase orders, Kopin absorbs the full macroeconomic friction between rigid upstream Asian foundries and erratic downstream U.S. government procurement cycles.

However, Kopin’s structural value cannot be evaluated strictly through near-term EPS parameters. The enterprise functions effectively as a subsidized, domestic R&D arm for the U.S. military industrial base. The $15.4 million Industrial Base Analysis and Sustainment (IBAS) award to develop ultra-bright, full-color MicroLEDs explicitly guarantees a funded R&D pipeline aimed at full-rate sovereign production in 2026 and beyond.

Looking forward, the fundamental metric for institutional investors is not top-line quarterly beats, but the conversion rate of R&D programs into Low-Rate Initial Production (LRIP) contracts. If management can successfully commercialize the NeuralDisplay™ architecture while cleanly migrating its OLED supply chain out of China, Kopin is uniquely positioned to monopolize the premium niche of ruggedized, AI-enabled optical subassemblies.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier financial intelligence and strategic advisory firm delivering institutional-grade market analysis. We specialize in forensic corporate filing deconstruction, supply chain vulnerability assessments, and geopolitical risk modeling. Discover actionable alpha at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The GAAP Illusion

A forensic audit of Kopin’s 2025 financials reveals a highly divergent corporate profile characterized by severe top-line pressure and an optical illusion of GAAP profitability. Total revenue contracted by 21.9% to $39.32 million, largely dictated by aggressive inventory de-stocking of legacy thermal weapon sights by Kopin's primary defense prime, DRS Network & Imaging Systems (which commands a perilous 62% customer concentration).

While the income statement broadcasts a positive Net Income of $2.6 million, this is entirely an accounting artifact. The bottom line was artificially inflated by an $11.1 million non-cash gain on the deconsolidation of Kopin Europe Ltd. and a $5.1 million reversal related to the BlueRadios litigation accrual. In reality, core operations bled $15.5 million in cash. The company faced distinct margin compression, with product gross margins deteriorating from 17.0% to 15.8%. This compression was compounded by lower overhead absorption and the absence of agile cost-pass-through mechanisms in its fixed-price military contracts, culminating in a nearly $1.0 million inventory obsolescence write-down.

Despite these operational cash drains, Kopin's technological moat remains aggressively funded. Eschewing full vertical integration to maintain its "fab-lite" structure, the company directed a highly intensive 25.8% of its revenue ($10.1 million) into R&D. This capital allocation is strictly ring-fenced for proprietary IP generation, notably the 5th-generation NeuralDisplay™—a software-defined, AI-enabled backplane with bi-directional sensing that fundamentally reduces Size, Weight, and Power (SWaP) parameters for tactical AR/VR headsets. Rather than pursuing external accretive acquisitions, management has utilized heavy, albeit necessary, equity dilution (expanding shares from 156.1 million to 176.9 million via a $38.1 million PIPE) to fortify a $36.4 million unrestricted cash runway through mid-2027.

Supply Chain Pivot: Reshoring and the European Hedge

Kopin's most critical strategic maneuver in 2025 is its aggressive supply chain realignment, driven by the escalating vulnerabilities of its legacy trans-Pacific dependencies. Historically reliant on a single foundry in Taiwan (Province of China) for AMLCD circuits and mainland Chinese foundries for OLED deposition, Kopin’s exposure to geopolitical shocks and U.S. tariff regimes is severe.

To execute on the Pentagon's sovereign source-of-origin requirements, Kopin is actively transitioning its critical OLED deposition phases to European foundries. This geographic migration is not merely a risk mitigation tactic; it is structurally integrated with its market expansion. The $15.0 million strategic investment from European defense contractor Theon International Plc—which acquired a 49% stake in Kopin Europe Ltd.—serves as a direct pipeline into localized NATO defense procurements, effectively creating a dual-hemisphere defense ecosystem.

Simultaneously, domestic capital expenditures surged 76% to $1.44 million, heavily weighted toward implementing automated camera inspection systems at the Westborough hub. This automation aims to replace human defect inspection, an operational necessity to reverse current margin deterioration and prepare for higher-volume ASOS assembly.

HDIN Institutional Perspective

Kopin’s 2025 audit signals a broader cyclical trough for legacy defense optical components, exposing the violent "bullwhip effect" inherent in custom military subassembly manufacturing. Lacking the protective buffer of long-term, non-cancellable purchase orders, Kopin absorbs the full macroeconomic friction between rigid upstream Asian foundries and erratic downstream U.S. government procurement cycles.

However, Kopin’s structural value cannot be evaluated strictly through near-term EPS parameters. The enterprise functions effectively as a subsidized, domestic R&D arm for the U.S. military industrial base. The $15.4 million Industrial Base Analysis and Sustainment (IBAS) award to develop ultra-bright, full-color MicroLEDs explicitly guarantees a funded R&D pipeline aimed at full-rate sovereign production in 2026 and beyond.

Looking forward, the fundamental metric for institutional investors is not top-line quarterly beats, but the conversion rate of R&D programs into Low-Rate Initial Production (LRIP) contracts. If management can successfully commercialize the NeuralDisplay™ architecture while cleanly migrating its OLED supply chain out of China, Kopin is uniquely positioned to monopolize the premium niche of ruggedized, AI-enabled optical subassemblies.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier financial intelligence and strategic advisory firm delivering institutional-grade market analysis. We specialize in forensic corporate filing deconstruction, supply chain vulnerability assessments, and geopolitical risk modeling. Discover actionable alpha at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*