Heavy Building Materials Leaders Pivot to High-Margin Aggregates and CCUS as Concrete Capacity Utilization Plunges to 20%

Date : 2026-04-16

Reading : 196

Global heavy building materials leaders—including CRH (NYSE: CRH), Holcim (SWX: HOLN), and Tianshan Materials (SZSE: 000877)—are executing aggressive asset rationalizations in FY2025. Facing an irreversible real estate demand contraction that dragged ready-mix concrete capacity utilization down to 20%, operators are deliberately divesting downstream assets. Capital allocation is structurally shifting toward high-margin aggregates, AI-driven logistics, and Carbon Capture, Utilization, and Storage (CCUS) compliance. This operational divergence strictly separates Western entities capturing legislative green premiums from APAC operators currently enduring severe margin compression and inventory de-stocking.

Financial Health & Operational Moats: The Aggregates Monopoly

Beneath the headline revenue figures of the 2025 audit cycle lies a ruthless polarization of earnings quality. Western operators have successfully shielded their balance sheets through aggressive vertical integration and strategic geographic monopolies, while emerging market incumbents face a severe liquidity squeeze.

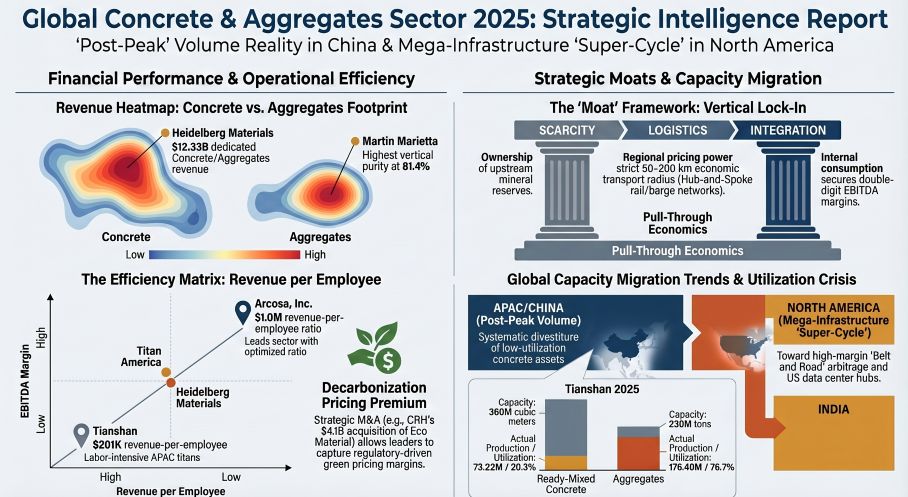

CRH plc and Heidelberg Materials (ETR: HEI) dictate global scale, generating $37.45 billion and $24.26 billion in total revenues, respectively. However, Martin Marietta (NYSE: MLM) offers the definitive benchmark for margin defense. By functioning as a near pure-play aggregates oligopolist—deriving over 81% of its $6.15 billion revenue from upstream stone extraction—the company achieved an exceptional 34% gross margin in its aggregates segment. MLM effectively leverages geological scarcity and permitting barriers (e.g., US EPA PSD regulations) to enact unilateral cost-pass-through mechanisms, easily outpacing underlying macroeconomic inflation.

Conversely, Chinese operators are navigating acute cash flow distress. Tianshan Materials reported a massive $1.01 billion (CNY 7.29 billion) net loss, recognizing $891 million in asset impairments and bad debt provisions. This collapse in earning quality is a direct result of toxic downstream exposure. The localized ready-mix concrete market suffers from extreme fragmentation, a lack of product differentiation, and highly stressed accounts receivable cycles tied to a paralyzed residential property sector.

The "So What" for Auditors and Investors: The ~20% concrete utilization rate is an undeniable distress signal. Arcosa (NYSE: ACA) generates an estimated $1.00 million per employee, optimizing human capital via high-margin infrastructure components, whereas volume-heavy APAC operators (averaging >$200,000 per employee) carry bloated, labor-intensive cost structures. Auditors must meticulously scrutinize delayed asset impairments on stranded heavy machinery and aggressive off-balance-sheet factoring (e.g., Special Purpose Entities used to artificially suppress Days Sales Outstanding).

Figure Global Concrete & Aggregates Sector 2025: Strategic Intelligence Report

Supply Chain Pivot: Logistics Arbitrage & AI-Driven Dispatch

Supply Chain Pivot: Logistics Arbitrage & AI-Driven Dispatch

Because heavy building materials possess an exceptionally low value-to-weight ratio, margin preservation explicitly depends on breaking the 200-kilometer terrestrial transport limit. Incumbents are abandoning localized truck-haul dependencies to construct intermodal "hub-and-spoke" hegemonies.

Titan America and Martin Marietta are successfully executing a waterborne arbitrage strategy. By utilizing multi-product marine import terminals—such as Titan’s Port Tampa Bay Terminal (handling 75,000-ton vessels)—these firms bypass localized geological constraints. MLM moves materials via oceangoing ships from mega-quarries in The Bahamas directly to the high-demand U.S. East Coast, converting a previously localized commodity into a fungible international asset.

Simultaneously, the supply chain is undergoing a brutal technological upgrade. Holcim’s global deployment of its AI-powered Transport Analytics Center (TAC) and OptiCEM formulation algorithm successfully removed 150,000 days of traditional laboratory testing time and eliminated empty-load truck journeys. Conch Cement (HKG: 0914) pioneered the industry's first manufacturing AI large model at its Congyang facility to maintain an elite $23.15/ton production cost. In 2026, the competitive moat is no longer just holding the physical quarry; it is possessing the edge-cloud AI necessary to orchestrate autonomous haul trucks and dynamic dispatching.

CapEx Realignment & The Green Premium

Capital expenditure has permanently rotated away from raw capacity expansion toward decarbonization and high-value accretive acquisitions. European operators, operating under the looming threat of the Carbon Border Adjustment Mechanism (CBAM) and strict ETS quotas, are wielding environmental compliance as a distinct economic weapon.

Heidelberg Materials secured global pricing power by launching the industry’s first industrial-scale Carbon Capture and Storage (CCS) plant in Brevik, Norway, enabling the commercialization of its carbon-captured net-zero cement, *evoZero*. Holcim committed a staggering $2.4 billion to CCUS projects by 2030, while utilizing green cash flow to execute 14 bolt-on acquisitions in Europe.

In North America, CRH completed an aggressive $4.1 billion M&A spree, anchored by the acquisition of Eco Material Technologies, North America's leading supplier of supplementary cementitious materials (SCM). These are not ESG optics; they are calculated maneuvers to capture a monopoly on the "Green Premium." In highly regulated markets, low-carbon concrete dictates premium pricing. In markets lacking regulatory carbon ceilings, high-cost green products face immediate rejection by cost-sensitive buyers, triggering market share erosion.

HDIN Institutional Perspective: A Permanent Structural Divergence

The era of synchronized global volume growth, historically underwritten by Chinese urbanization and zero-interest-rate real estate booms, is dead. HDIN Research concludes that the building materials sector has bifurcated into two mutually exclusive realities.

In the U.S., a politically insulated infrastructure super-cycle is underway. Supported by the Infrastructure Investment and Jobs Act (IIJA) and the AI-driven data center build-out, operators like CRH and Arcosa are entirely insulated from residential housing dips.

In APAC, the sector is experiencing a Japan-style structural plateau. Domestic operations are trapped in a vicious cycle of inventory de-stocking and price wars. To survive, Chinese state-backed titans are forced to export their industrial overcapacity through aggressive cross-border M&A. Tianshan’s 2025 acquisitions of Société Les Ciments de Jbel Oust in Tunisia and Qaz Cement Industries in Kazakhstan represent geographic arbitrage—fleeing domestic deflation to establish pricing power in the MENA and Central Asian corridors. Moving into 2026, terminal profitability will belong exclusively to those who control upstream aggregates, possess deep-water logistics, and govern the proprietary AI models driving alternative fuel combustion.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm specializing in global industrial supply chains, financial benchmarking, and macroeconomic policy analysis. For deeper institutional insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Aggregates Monopoly

Beneath the headline revenue figures of the 2025 audit cycle lies a ruthless polarization of earnings quality. Western operators have successfully shielded their balance sheets through aggressive vertical integration and strategic geographic monopolies, while emerging market incumbents face a severe liquidity squeeze.

CRH plc and Heidelberg Materials (ETR: HEI) dictate global scale, generating $37.45 billion and $24.26 billion in total revenues, respectively. However, Martin Marietta (NYSE: MLM) offers the definitive benchmark for margin defense. By functioning as a near pure-play aggregates oligopolist—deriving over 81% of its $6.15 billion revenue from upstream stone extraction—the company achieved an exceptional 34% gross margin in its aggregates segment. MLM effectively leverages geological scarcity and permitting barriers (e.g., US EPA PSD regulations) to enact unilateral cost-pass-through mechanisms, easily outpacing underlying macroeconomic inflation.

Conversely, Chinese operators are navigating acute cash flow distress. Tianshan Materials reported a massive $1.01 billion (CNY 7.29 billion) net loss, recognizing $891 million in asset impairments and bad debt provisions. This collapse in earning quality is a direct result of toxic downstream exposure. The localized ready-mix concrete market suffers from extreme fragmentation, a lack of product differentiation, and highly stressed accounts receivable cycles tied to a paralyzed residential property sector.

The "So What" for Auditors and Investors: The ~20% concrete utilization rate is an undeniable distress signal. Arcosa (NYSE: ACA) generates an estimated $1.00 million per employee, optimizing human capital via high-margin infrastructure components, whereas volume-heavy APAC operators (averaging >$200,000 per employee) carry bloated, labor-intensive cost structures. Auditors must meticulously scrutinize delayed asset impairments on stranded heavy machinery and aggressive off-balance-sheet factoring (e.g., Special Purpose Entities used to artificially suppress Days Sales Outstanding).

Figure Global Concrete & Aggregates Sector 2025: Strategic Intelligence Report

Supply Chain Pivot: Logistics Arbitrage & AI-Driven DispatchBecause heavy building materials possess an exceptionally low value-to-weight ratio, margin preservation explicitly depends on breaking the 200-kilometer terrestrial transport limit. Incumbents are abandoning localized truck-haul dependencies to construct intermodal "hub-and-spoke" hegemonies.

Titan America and Martin Marietta are successfully executing a waterborne arbitrage strategy. By utilizing multi-product marine import terminals—such as Titan’s Port Tampa Bay Terminal (handling 75,000-ton vessels)—these firms bypass localized geological constraints. MLM moves materials via oceangoing ships from mega-quarries in The Bahamas directly to the high-demand U.S. East Coast, converting a previously localized commodity into a fungible international asset.

Simultaneously, the supply chain is undergoing a brutal technological upgrade. Holcim’s global deployment of its AI-powered Transport Analytics Center (TAC) and OptiCEM formulation algorithm successfully removed 150,000 days of traditional laboratory testing time and eliminated empty-load truck journeys. Conch Cement (HKG: 0914) pioneered the industry's first manufacturing AI large model at its Congyang facility to maintain an elite $23.15/ton production cost. In 2026, the competitive moat is no longer just holding the physical quarry; it is possessing the edge-cloud AI necessary to orchestrate autonomous haul trucks and dynamic dispatching.

CapEx Realignment & The Green Premium

Capital expenditure has permanently rotated away from raw capacity expansion toward decarbonization and high-value accretive acquisitions. European operators, operating under the looming threat of the Carbon Border Adjustment Mechanism (CBAM) and strict ETS quotas, are wielding environmental compliance as a distinct economic weapon.

Heidelberg Materials secured global pricing power by launching the industry’s first industrial-scale Carbon Capture and Storage (CCS) plant in Brevik, Norway, enabling the commercialization of its carbon-captured net-zero cement, *evoZero*. Holcim committed a staggering $2.4 billion to CCUS projects by 2030, while utilizing green cash flow to execute 14 bolt-on acquisitions in Europe.

In North America, CRH completed an aggressive $4.1 billion M&A spree, anchored by the acquisition of Eco Material Technologies, North America's leading supplier of supplementary cementitious materials (SCM). These are not ESG optics; they are calculated maneuvers to capture a monopoly on the "Green Premium." In highly regulated markets, low-carbon concrete dictates premium pricing. In markets lacking regulatory carbon ceilings, high-cost green products face immediate rejection by cost-sensitive buyers, triggering market share erosion.

HDIN Institutional Perspective: A Permanent Structural Divergence

The era of synchronized global volume growth, historically underwritten by Chinese urbanization and zero-interest-rate real estate booms, is dead. HDIN Research concludes that the building materials sector has bifurcated into two mutually exclusive realities.

In the U.S., a politically insulated infrastructure super-cycle is underway. Supported by the Infrastructure Investment and Jobs Act (IIJA) and the AI-driven data center build-out, operators like CRH and Arcosa are entirely insulated from residential housing dips.

In APAC, the sector is experiencing a Japan-style structural plateau. Domestic operations are trapped in a vicious cycle of inventory de-stocking and price wars. To survive, Chinese state-backed titans are forced to export their industrial overcapacity through aggressive cross-border M&A. Tianshan’s 2025 acquisitions of Société Les Ciments de Jbel Oust in Tunisia and Qaz Cement Industries in Kazakhstan represent geographic arbitrage—fleeing domestic deflation to establish pricing power in the MENA and Central Asian corridors. Moving into 2026, terminal profitability will belong exclusively to those who control upstream aggregates, possess deep-water logistics, and govern the proprietary AI models driving alternative fuel combustion.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm specializing in global industrial supply chains, financial benchmarking, and macroeconomic policy analysis. For deeper institutional insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.