AI Infrastructure Leaders Post Diverging ROIC: Dell Hits 22.9% as Supermicro Faces Working Capital Trap and Governance Red Flags

Date : 2026-04-17

Reading : 575

The global IT infrastructure sector has reached a structural crossroads in 2026, transitioning from traditional hardware assembly to advanced systems engineering driven by explosive Artificial Intelligence (AI) demand. While top-line growth remains robust, a deep-dive analysis into the FY2025/2026 disclosures of market leaders—including Dell Technologies, HPE, Cisco, and Super Micro Computer (SMCI)—reveals a widening chasm in capital efficiency and earnings quality. As thermal and power limitations become the new industry bottleneck, the strategic focus has shifted from mere silicon procurement to liquid cooling mastery and "Sovereign AI" infrastructure.

Financial Health: The ROIC Divergence & The "Working Capital Trap"

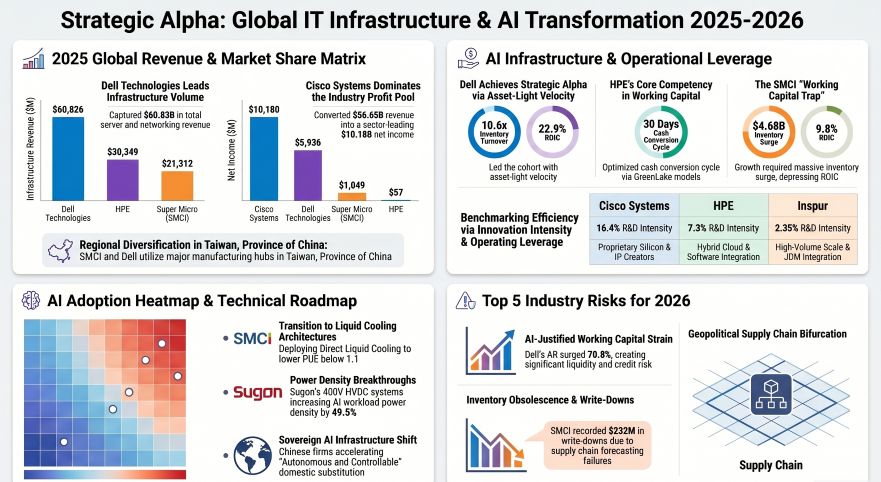

A critical examination of Return on Invested Capital (ROIC) highlights the operational victors in the AI arms race. Dell Technologies (NYSE: DELL) has emerged as the capital efficiency leader with a projected 22.9% ROIC, weaponizing its supply chain mastery and "As-a-Service" model to operate on a lean, even negative, equity base. Conversely, Super Micro Computer (NASDAQ: SMCI) finds itself in a "working capital trap," with an ROIC of just 9.8%. Despite staggering 46.6% revenue growth, SMCI has been forced to balloon its inventory to $4.68 billion to secure GPU allocations, severely diluting its strategic alpha.

Cisco Systems (NASDAQ: CSCO) continues to prioritize high-margin "sticky" revenue, maintaining a 16.4% R&D intensity focused on proprietary silicon (Silicon One) and cybersecurity, insulating itself from low-margin server volume wars.

Figure Global IT infrastructure & Al Transformation 2025-2026

The New Bottleneck: Thermal Management & Power Density

The New Bottleneck: Thermal Management & Power Density

Physical constraints—specifically power and thermal limits—now dictate Capital Expenditure (CapEx) trends. Traditional air cooling has hit its limit as single-chip heat dissipation for next-gen GPUs exceeds 3000W.

Liquid Cooling Standards: Inspur has deployed megawatt-level two-phase liquid-cooled racks, while SMCI claims its "DLC-2" solution reduces data center electricity costs by 40%.

Power Distribution: Sugon is addressing AI power density by developing 400V High Voltage Direct Current (HVDC) systems, increasing density by nearly 50% to support massive AI workloads.

As-a-Service Pivot: HPE and Dell are aggressively funding "assets in customer contracts" (e.g., HPE GreenLake), diverting billions in CapEx to support flexible consumption models that lower the initial barrier for AI adoption.

Supply Chain Resilience: Diversification vs. Localization

Geopolitical tensions have fractured the global hardware stack, forcing a bifurcated supply chain strategy.

Hewlett Packard Enterprise (NYSE: HPE) currently possesses the most geopolitically resilient network, distributing final assembly across 15 distinct global hubs, including the U.S., Mexico, Malaysia, and the Czech Republic. In contrast, SMCI faces acute concentration risk, with 64.4% of its total purchases sourced from a single supplier (Supplier A), leaving it vulnerable to pricing and availability shocks.

In the East, Unisplendour and Sugon are executing "Autonomous and Controllable" mandates. Unisplendour has successfully commercialized 800G switches utilizing domestic "National Chips" , while Sugon has deployed a 30,000-card domestic AI computing pool to insulate its ecosystem from U.S. export controls.

HDIN Institutional Perspective: Audit Red Flags in a High-Growth Cycle

While AI demand provides a convenient narrative for massive inventory builds, HDIN Research warns analysts to look past the "AI-Justified" working capital expansions.

Super Micro Computer presents a severe governance red flag following the resignation of its independent auditor, Ernst & Young (EY), over transparency concerns and material weaknesses in internal controls. Furthermore, SMCI's $232 million inventory write-down in 2025—a 180% year-over-year spike—suggests significant supply chain forecasting failures in an allegedly "supply-constrained" market.

Investors should also monitor Dell’s 70.8% surge in Accounts Receivable, which poses liquidity risks if the ROI on end-customer AI infrastructure fails to materialize.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a leading global provider of strategic market intelligence and equity analysis, delivering unvarnished insights into the world's most complex industrial and technology sectors.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health: The ROIC Divergence & The "Working Capital Trap"

A critical examination of Return on Invested Capital (ROIC) highlights the operational victors in the AI arms race. Dell Technologies (NYSE: DELL) has emerged as the capital efficiency leader with a projected 22.9% ROIC, weaponizing its supply chain mastery and "As-a-Service" model to operate on a lean, even negative, equity base. Conversely, Super Micro Computer (NASDAQ: SMCI) finds itself in a "working capital trap," with an ROIC of just 9.8%. Despite staggering 46.6% revenue growth, SMCI has been forced to balloon its inventory to $4.68 billion to secure GPU allocations, severely diluting its strategic alpha.

Cisco Systems (NASDAQ: CSCO) continues to prioritize high-margin "sticky" revenue, maintaining a 16.4% R&D intensity focused on proprietary silicon (Silicon One) and cybersecurity, insulating itself from low-margin server volume wars.

Figure Global IT infrastructure & Al Transformation 2025-2026

The New Bottleneck: Thermal Management & Power DensityPhysical constraints—specifically power and thermal limits—now dictate Capital Expenditure (CapEx) trends. Traditional air cooling has hit its limit as single-chip heat dissipation for next-gen GPUs exceeds 3000W.

Liquid Cooling Standards: Inspur has deployed megawatt-level two-phase liquid-cooled racks, while SMCI claims its "DLC-2" solution reduces data center electricity costs by 40%.

Power Distribution: Sugon is addressing AI power density by developing 400V High Voltage Direct Current (HVDC) systems, increasing density by nearly 50% to support massive AI workloads.

As-a-Service Pivot: HPE and Dell are aggressively funding "assets in customer contracts" (e.g., HPE GreenLake), diverting billions in CapEx to support flexible consumption models that lower the initial barrier for AI adoption.

Supply Chain Resilience: Diversification vs. Localization

Geopolitical tensions have fractured the global hardware stack, forcing a bifurcated supply chain strategy.

Hewlett Packard Enterprise (NYSE: HPE) currently possesses the most geopolitically resilient network, distributing final assembly across 15 distinct global hubs, including the U.S., Mexico, Malaysia, and the Czech Republic. In contrast, SMCI faces acute concentration risk, with 64.4% of its total purchases sourced from a single supplier (Supplier A), leaving it vulnerable to pricing and availability shocks.

In the East, Unisplendour and Sugon are executing "Autonomous and Controllable" mandates. Unisplendour has successfully commercialized 800G switches utilizing domestic "National Chips" , while Sugon has deployed a 30,000-card domestic AI computing pool to insulate its ecosystem from U.S. export controls.

HDIN Institutional Perspective: Audit Red Flags in a High-Growth Cycle

While AI demand provides a convenient narrative for massive inventory builds, HDIN Research warns analysts to look past the "AI-Justified" working capital expansions.

Super Micro Computer presents a severe governance red flag following the resignation of its independent auditor, Ernst & Young (EY), over transparency concerns and material weaknesses in internal controls. Furthermore, SMCI's $232 million inventory write-down in 2025—a 180% year-over-year spike—suggests significant supply chain forecasting failures in an allegedly "supply-constrained" market.

Investors should also monitor Dell’s 70.8% surge in Accounts Receivable, which poses liquidity risks if the ROI on end-customer AI infrastructure fails to materialize.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a leading global provider of strategic market intelligence and equity analysis, delivering unvarnished insights into the world's most complex industrial and technology sectors.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.