Global EV Manufacturers Face Strategic Bifurcation: Tesla and BYD Consolidate Market Power as Sub-Scale Players Signal Distressed Liquidity in 2025 Audit

Date : 2026-04-17

Reading : 266

Following the comprehensive audit of 2025 fiscal year filings, the global New Energy Vehicle (NEV) sector has transitioned into a ruthless "elimination round". While Tesla (NASDAQ: TSLA) and BYD (HKG: 1211) leveraged massive cash reserves and vertical integration to maintain dominance, emerging players like Lucid (NASDAQ: LCID) and NIO (NYSE: NIO) faced distressed leverage profiles and critical cash burn. This divergence is fueled by a pivot toward AI-driven intelligence, localized manufacturing to bypass 100% US tariffs, and a shift from hardware margins to recurring software revenue.

Financial Health & Operational Moats: The "Solvency Gap"

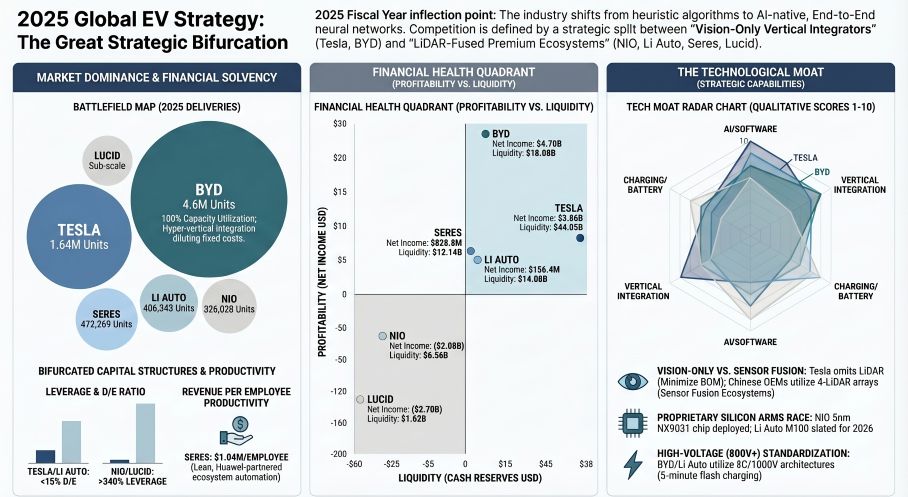

The 2025 balance sheets reveal a stark bifurcation in capital structure between industry leaders and those reliant on alternative financing.

Tier 1: Self-Sustaining Moats: Tesla maintains exceptional solvency with a Debt-to-Equity (D/E) ratio of ~10.2% and a $44.05 billion liquidity buffer. Similarly, Seres achieved a definitive financial moat in 2025, generating $3.4 billion in Free Cash Flow (FCF) and operating with a highly efficient, negative Cash Conversion Cycle (CCC).

Tier 2: Growth-Dependent Moats: BYD reported excellent operational cash generation of $8.2 billion but remains FCF negative due to an aggressive $21.8 billion CapEx expansion aimed at global capacity. Li Auto holds a formidable $14.5 billion cash reserve but saw its operating cash flow turn negative in 2025 primarily due to a $1.86 billion pay-down of supplier obligations.

Tier 3: External Capital Reliance: NIO and Lucid exhibit distressed leverage, with D/E ratios of ~349% and ~381%, respectively. NIO’s current liabilities ($11.23 billion) now exceed its current assets ($10.95 billion), triggering "Going Concern" warnings from auditors.

Figure 2025 Global EV Strategy

Supply Chain Pivot: Localized Manufacturing & Tariff Defense

Supply Chain Pivot: Localized Manufacturing & Tariff Defense

In response to intensifying geopolitical trade barriers—including 100% tariffs in the U.S. and up to 45.3% duties in the EU—OEMs have shifted to an "In-Market, For-Market" manufacturing paradigm.

Global Footprint Expansion: BYD achieved its first vehicle roll-off in Brazil in July 2025 and is advancing production in Thailand and Hungary to bypass import restrictions. Tesla continues to secure its North American footprint through Tesla Manufacturing Mexico and internal battery cell production in Texas.

Capacity Polarization: Seres demonstrated high manufacturing efficiency, with its core "Smart Factory" operating at 144.11% utilization. In contrast, Lucid's AMP-1 facility in Arizona remains structurally underutilized despite Phase 2 expansion to 90,000 units.

Vertical Integration as a Moat: BYD maintains absolute control over its supply chain via its "Blade Battery" and in-house semiconductor R&D. Tesla’s Texas lithium refinery, operational as of January 2026, further insulates the company from raw material price volatility.

The AI Frontier: Software-Defined Vehicles (SDVs)

Hardware has become a commoditized conduit for high-margin software ecosystems, with AI and Autonomous Driving (AD) serving as the primary moats in 2025.

Table 2025 Strategic Capability Matrix

Recurring Revenue Streams: Tesla and NIO are successfully extracting SaaS-like margins from services. Tesla's "Services and Other" revenue reached $12.53 billion, while NIO’s Battery-as-a-Service (BaaS) model and technical licensing to brands like McLaren have turned its "Other Sales" margin from -8.6% to +6.6%.

HDIN Institutional Perspective: The "Red Flag" Framework

Professional analysts must scrutinize the following 2025 anomalies:

Li Auto’s Earnings Quality: The extreme divergence between positive Net Income ($162.9M) and negative Operating Cash Flow (-$1.23B) suggests aggressive working capital management or a buildup of potentially obsolete inventory.

Lucid’s Inventory Mismatch: Lucid recorded $815.7 million in inventory write-downs—roughly 60% of its total annual revenue—indicating a catastrophic failure in demand forecasting.

Supplier Leverage Traps: Seres and BYD carry massive payables ($11.08B and $25.98B respectively). While this provides "interest-free" leverage, any slowdown in sales velocity could trigger a sudden liquidity crunch as supplier obligations come due.

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides data-driven, MECE-aligned intelligence on the global technology and automotive sectors.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The "Solvency Gap"

The 2025 balance sheets reveal a stark bifurcation in capital structure between industry leaders and those reliant on alternative financing.

Tier 1: Self-Sustaining Moats: Tesla maintains exceptional solvency with a Debt-to-Equity (D/E) ratio of ~10.2% and a $44.05 billion liquidity buffer. Similarly, Seres achieved a definitive financial moat in 2025, generating $3.4 billion in Free Cash Flow (FCF) and operating with a highly efficient, negative Cash Conversion Cycle (CCC).

Tier 2: Growth-Dependent Moats: BYD reported excellent operational cash generation of $8.2 billion but remains FCF negative due to an aggressive $21.8 billion CapEx expansion aimed at global capacity. Li Auto holds a formidable $14.5 billion cash reserve but saw its operating cash flow turn negative in 2025 primarily due to a $1.86 billion pay-down of supplier obligations.

Tier 3: External Capital Reliance: NIO and Lucid exhibit distressed leverage, with D/E ratios of ~349% and ~381%, respectively. NIO’s current liabilities ($11.23 billion) now exceed its current assets ($10.95 billion), triggering "Going Concern" warnings from auditors.

Figure 2025 Global EV Strategy

Supply Chain Pivot: Localized Manufacturing & Tariff DefenseIn response to intensifying geopolitical trade barriers—including 100% tariffs in the U.S. and up to 45.3% duties in the EU—OEMs have shifted to an "In-Market, For-Market" manufacturing paradigm.

Global Footprint Expansion: BYD achieved its first vehicle roll-off in Brazil in July 2025 and is advancing production in Thailand and Hungary to bypass import restrictions. Tesla continues to secure its North American footprint through Tesla Manufacturing Mexico and internal battery cell production in Texas.

Capacity Polarization: Seres demonstrated high manufacturing efficiency, with its core "Smart Factory" operating at 144.11% utilization. In contrast, Lucid's AMP-1 facility in Arizona remains structurally underutilized despite Phase 2 expansion to 90,000 units.

Vertical Integration as a Moat: BYD maintains absolute control over its supply chain via its "Blade Battery" and in-house semiconductor R&D. Tesla’s Texas lithium refinery, operational as of January 2026, further insulates the company from raw material price volatility.

The AI Frontier: Software-Defined Vehicles (SDVs)

Hardware has become a commoditized conduit for high-margin software ecosystems, with AI and Autonomous Driving (AD) serving as the primary moats in 2025.

Table 2025 Strategic Capability Matrix

| Company | Sensor Paradigm | Silicon Strategy | Key Software Milestone |

| Tesla |

Vision-Only |

In-house Inference Chips |

Robotaxi Launch (June 2025) |

| BYD |

Sensor Fusion |

Central Compute Platform |

Xuanji Intelligent Architecture |

| NIO |

LiDAR-Heavy |

5nm NX9031 (In-house) |

NIO WorldModel (NWM) |

| Li Auto |

LiDAR-Heavy |

M100 (In-house, 2026) |

VLA Driver AI Model |

Recurring Revenue Streams: Tesla and NIO are successfully extracting SaaS-like margins from services. Tesla's "Services and Other" revenue reached $12.53 billion, while NIO’s Battery-as-a-Service (BaaS) model and technical licensing to brands like McLaren have turned its "Other Sales" margin from -8.6% to +6.6%.

HDIN Institutional Perspective: The "Red Flag" Framework

Professional analysts must scrutinize the following 2025 anomalies:

Li Auto’s Earnings Quality: The extreme divergence between positive Net Income ($162.9M) and negative Operating Cash Flow (-$1.23B) suggests aggressive working capital management or a buildup of potentially obsolete inventory.

Lucid’s Inventory Mismatch: Lucid recorded $815.7 million in inventory write-downs—roughly 60% of its total annual revenue—indicating a catastrophic failure in demand forecasting.

Supplier Leverage Traps: Seres and BYD carry massive payables ($11.08B and $25.98B respectively). While this provides "interest-free" leverage, any slowdown in sales velocity could trigger a sudden liquidity crunch as supplier obligations come due.

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research provides data-driven, MECE-aligned intelligence on the global technology and automotive sectors.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.