Tonies SE Consolidates Global Audio Leadership as North America Revenue Surges 31.1% in FY2025 Audit

Date : 2026-04-17

Reading : 62

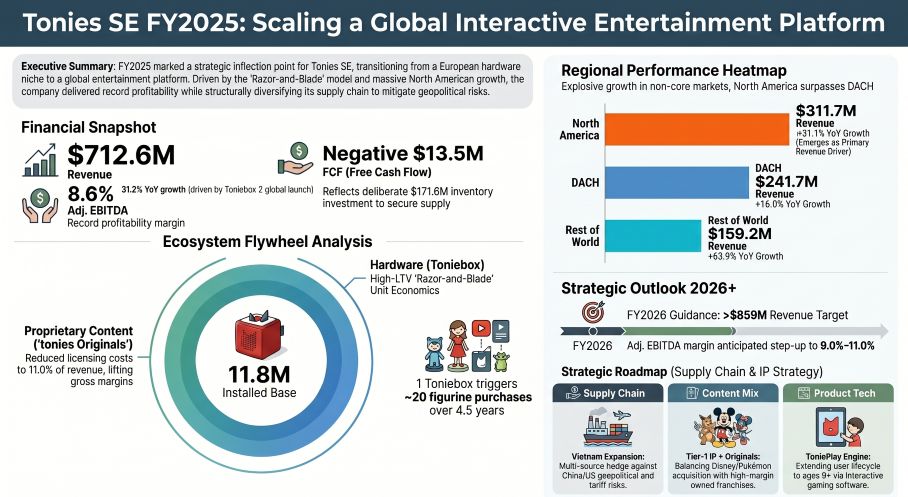

Tonies SE (FRA: TNIE) achieved a strategic inflection point in FY2025, reporting a 31.2% YoY revenue surge to $712.62 million. Driven by the global launch of Toniebox 2 and aggressive North American expansion, the region officially surpassed the DACH market as the group’s largest revenue contributor. Management leveraged a high-margin "Razor-and-Blade" model and expanded Adjusted EBITDA margins to 8.6%, while proactively de-risking the supply chain through a 70% inventory build-up and production shifts to Vietnam to hedge against geopolitical volatility.

Financial Health & Operational Moats: The Razor-and-Blade Inflection

Tonies SE has successfully transitioned from a category creator to a scaling global platform, characterized by robust unit economics and operational leverage.

Revenue Dynamics: Total revenue reached $712.62 million (EUR 630.3 million). The ecosystem’s "blades"—Tonie figurines—generated $505.60 million (+37.4% YoY), significantly outperforming the "razor" hardware sales of $182.25 million.

Margin Expansion: Gross margin expanded to 62.8%. This was fueled by the "tonies Originals" strategy, which reduced licensing costs to 11.0% of revenue. The Contribution Margin improved to 37.0%.

Geographic Pivot: North America now accounts for 43.7% of total revenue ($311.7 million), fueled by over 7,300 points of sale including Walmart and Target.

Profitability Guidance: Management issued 2026 revenue guidance exceeding $859.3 million, with Adjusted EBITDA margins projected to climb to 9.0%–11.0%.

Figure Tonies SE FY2025 Scaling a Global Interactive Entertainment Platform

Supply Chain Pivot: Strategic Stockpiling and De-risking China

Supply Chain Pivot: Strategic Stockpiling and De-risking China

In response to US-China geopolitical tensions and tariff uncertainties, Tonies executed a massive strategic shift in its Net Working Capital (NWC).

Inventory Strategy: Inventory grew 70.3% YoY to $171.63 million. This "strategic build-up" was designed to secure product availability for the Toniebox 2 launch and insulate the company from potential US protective tariffs.

Multi-Sourcing Execution: To reduce dependency on Chinese manufacturing, the company successfully onboarded an additional hardware manufacturer in Vietnam.

Near-shoring & Friend-shoring: Production of figurines in Bosnia and Tunisia places manufacturing closer to core European markets, while Vietnam serves as a "friend-shoring" hedge for the North American supply chain.

Logistics Optimization: The establishment of local warehousing hubs is intended to reduce freight costs and minimize transit times.

Platform Evolution: Expanding the Demographic Moat

The launch of Toniebox 2 marks a shift from a simple audio player to an interactive entertainment platform.

Age Expansion: The target demographic has been widened from 3–7 years to 1–9+ years through products like "My First Tonies" for infants and "Pocket Tonies" for older children.

ToniePlay Engine: The new hardware integrates a proprietary gaming engine, introducing audio-first interactive games (e.g., Monopoly with Hasbro) to retain older users.

IP Fortress: The company maintains a dual-track IP strategy, using "Blockbuster" licenses (e.g., Disney, Pokémon, Paw Patrol) for acquisition while driving margins through proprietary content like Sleepy Friends.

HDIN Institutional Perspective: Balancing Growth with Liquidity Risks

While Tonies SE's 2025 performance signals a "scale-up" success, the transition is not without friction. The Free Cash Flow (FCF) turned negative (-$13.45 million) in 2025, a direct consequence of the $64.56 million cash outflow into Net Working Capital.

The doubling of obsolescence expenses to $11.04 million indicates that the aggressive inventory build-up carries inherent overstocking risks. Furthermore, the company faces significant supplier concentration risk and a high reliance on the US consumer, leaving it vulnerable to macroeconomic cooling. However, the successful syndicated loan facility increase to $113 million provides the liquidity cushion necessary to navigate these seasonal and geopolitical headwinds.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a leading provider of independent equity research and strategic market intelligence, focusing on global technology and consumer ecosystems.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Razor-and-Blade Inflection

Tonies SE has successfully transitioned from a category creator to a scaling global platform, characterized by robust unit economics and operational leverage.

Revenue Dynamics: Total revenue reached $712.62 million (EUR 630.3 million). The ecosystem’s "blades"—Tonie figurines—generated $505.60 million (+37.4% YoY), significantly outperforming the "razor" hardware sales of $182.25 million.

Margin Expansion: Gross margin expanded to 62.8%. This was fueled by the "tonies Originals" strategy, which reduced licensing costs to 11.0% of revenue. The Contribution Margin improved to 37.0%.

Geographic Pivot: North America now accounts for 43.7% of total revenue ($311.7 million), fueled by over 7,300 points of sale including Walmart and Target.

Profitability Guidance: Management issued 2026 revenue guidance exceeding $859.3 million, with Adjusted EBITDA margins projected to climb to 9.0%–11.0%.

Figure Tonies SE FY2025 Scaling a Global Interactive Entertainment Platform

Supply Chain Pivot: Strategic Stockpiling and De-risking ChinaIn response to US-China geopolitical tensions and tariff uncertainties, Tonies executed a massive strategic shift in its Net Working Capital (NWC).

Inventory Strategy: Inventory grew 70.3% YoY to $171.63 million. This "strategic build-up" was designed to secure product availability for the Toniebox 2 launch and insulate the company from potential US protective tariffs.

Multi-Sourcing Execution: To reduce dependency on Chinese manufacturing, the company successfully onboarded an additional hardware manufacturer in Vietnam.

Near-shoring & Friend-shoring: Production of figurines in Bosnia and Tunisia places manufacturing closer to core European markets, while Vietnam serves as a "friend-shoring" hedge for the North American supply chain.

Logistics Optimization: The establishment of local warehousing hubs is intended to reduce freight costs and minimize transit times.

Platform Evolution: Expanding the Demographic Moat

The launch of Toniebox 2 marks a shift from a simple audio player to an interactive entertainment platform.

Age Expansion: The target demographic has been widened from 3–7 years to 1–9+ years through products like "My First Tonies" for infants and "Pocket Tonies" for older children.

ToniePlay Engine: The new hardware integrates a proprietary gaming engine, introducing audio-first interactive games (e.g., Monopoly with Hasbro) to retain older users.

IP Fortress: The company maintains a dual-track IP strategy, using "Blockbuster" licenses (e.g., Disney, Pokémon, Paw Patrol) for acquisition while driving margins through proprietary content like Sleepy Friends.

HDIN Institutional Perspective: Balancing Growth with Liquidity Risks

While Tonies SE's 2025 performance signals a "scale-up" success, the transition is not without friction. The Free Cash Flow (FCF) turned negative (-$13.45 million) in 2025, a direct consequence of the $64.56 million cash outflow into Net Working Capital.

The doubling of obsolescence expenses to $11.04 million indicates that the aggressive inventory build-up carries inherent overstocking risks. Furthermore, the company faces significant supplier concentration risk and a high reliance on the US consumer, leaving it vulnerable to macroeconomic cooling. However, the successful syndicated loan facility increase to $113 million provides the liquidity cushion necessary to navigate these seasonal and geopolitical headwinds.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a leading provider of independent equity research and strategic market intelligence, focusing on global technology and consumer ecosystems.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.