Autonomous Last Mile Infrastructure Enters Liquidity Node: Arrive AI Signals Going Concern Risk Amid $12.8M Cash Bleed and Nasdaq Delisting Threat

Date : 2026-04-21

Reading : 59

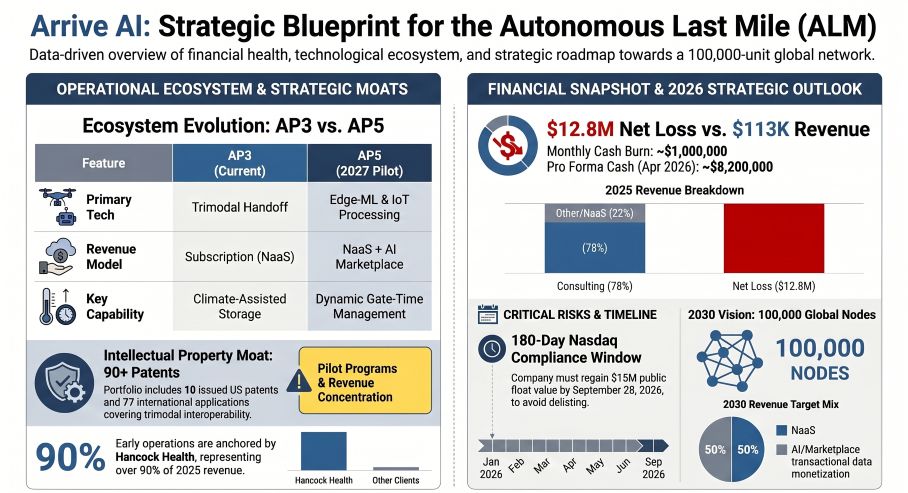

Fishers, Indiana-based Arrive AI is navigating an acute liquidity crisis following its FY2026 audit disclosures. The Autonomous Last Mile (ALM) infrastructure developer received formal Nasdaq delisting notices on March 31, 2026, after its Market Value of Publicly Held Shares (MVPHS) collapsed below the $15 million regulatory threshold. Burning approximately $1 million in cash monthly against a meager $113,250 in 2025 commercial revenue—90% of which is concentrated with a single pilot partner, Hancock Health—the company is structurally reliant on highly dilutive convertible debt from Streeterville Capital. Failure to regain listing compliance by September 28, 2026, risks triggering a fatal downward equity spiral.

Financial Health & Operational Moats: The NaaS Pivot Meets Toxic Capital

Arrive AI is attempting an aggressive transition from a pre-revenue R&D outfit into a Network-as-a-Service (NaaS) platform operator. The strategic roadmap involves moving away from basic automated handoffs (AP3 units) toward edge-computing ALM infrastructure (AP5 units) capable of dynamic pricing and artificial intelligence-driven data monetization. However, the fundamental execution of this Mailbox-as-a-Service (MaaS) model is severely bottlenecked by a toxic capital structure.

A forensic analysis of the 2025 balance sheet reveals exceptionally low earnings quality, distorted by ASC 815 derivative accounting complexities. Operating expenses surged 128% year-over-year to $10.46 million, driving a net loss of $12.83 million and negative operating cash flows of $8.25 million.

To avert immediate insolvency, Arrive AI secured $9.6 million in net proceeds via a January 26, 2026, convertible note (Pre-Paid Purchase No. 4) from Streeterville Capital, extending its cash runway through late Q4 2026. This $40 million debt facility acts as a double-edged sword. It features a punitive "Lookback Formula" with a $0.25 per share floor. If the volume-weighted average price (VWAP) breaches this floor, it activates a trigger mandating cash repayments of $2,887,500 per month—effectively a death knell for a company with $8.2 million in short-term liquidity. This creates a perpetual overhang, suppressing the stock price and triggering continuous share dilution.

Figure Arrive Al Strategic Blueprint for the Autonomous Last Mile (ALM)

Supply Chain Pivot & Governance Disconnect

Supply Chain Pivot & Governance Disconnect

Operationally, Arrive AI has executed a strategic internalization of its engineering capabilities, scaling its full-time headcount from 8 to 41 employees. This vertical integration successfully drove down third-party R&D vendor costs from $760,036 in 2024 to $600,510 in 2025. Yet, critical supply chain vulnerabilities remain, notably a reliance on non-cancelable purchase commitments for regulated refrigerant substances required for cold-chain storage, and a heavy IT dependency on Microsoft Azure infrastructure managed by Synoptek, LLC.

More alarming is the structural decoupling between insider incentives and public shareholder value. While public equity faces relentless dilution, management aggressively extracted capital during the DPO process, including $1.86 million in one-time public-listing "success bonuses" for executives.

Furthermore, the company lacks direct ownership of its core foundational patents. The intellectual property is exclusively licensed from CEO Daniel O'Toole in a perpetual agreement that guarantees him a $25-per-unit royalty once monthly revenues scale. If the company defaults on this related-party agreement, the license reverts to non-exclusive status, stripping Arrive AI of its primary competitive moat and exposing the enterprise to catastrophic operational failure.

HDIN Institutional Perspective: A "Highest Common Denominator" CapEx Trap?

From an institutional standpoint, Arrive AI’s strategy to position itself as the "Highest Common Denominator"—a hardware-agnostic platform capable of servicing drones, autonomous mobile robots (AMRs), and human couriers—is theoretically sound. It counter-positions against the fragmented, closed-loop proprietary networks currently deployed by FedEx or Walmart.

However, macroeconomic and regulatory realities cap the near-term Total Addressable Market. Broad ALM adoption remains throttled by the Federal Aviation Administration’s (FAA) Beyond Visual Line of Sight (BVLOS) restrictions. The assumption that Arrive AI can scale to 100,000 active nodes by 2030 to achieve a 50/50 revenue split between hardware subscriptions and its "AdSense-like" ALM Marketplace ignores the systemic friction in municipal zoning and airspace regulation.

Until the regulatory environment matures to support dense, autonomous drone routing, Arrive AI is trapped in an asset-heavy CapEx cycle. It must fund the upfront manufacturing and deployment of AP4 and AP5 units while extracting nominal subscription fees from early-adopter healthcare pilots. Unless the company secures non-toxic, long-term institutional equity to bridge the gap between pilot scale and network density, the operation remains fundamentally distressed.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and corporate strategy firm providing institutional-grade financial analysis. For more actionable market intelligence, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The NaaS Pivot Meets Toxic Capital

Arrive AI is attempting an aggressive transition from a pre-revenue R&D outfit into a Network-as-a-Service (NaaS) platform operator. The strategic roadmap involves moving away from basic automated handoffs (AP3 units) toward edge-computing ALM infrastructure (AP5 units) capable of dynamic pricing and artificial intelligence-driven data monetization. However, the fundamental execution of this Mailbox-as-a-Service (MaaS) model is severely bottlenecked by a toxic capital structure.

A forensic analysis of the 2025 balance sheet reveals exceptionally low earnings quality, distorted by ASC 815 derivative accounting complexities. Operating expenses surged 128% year-over-year to $10.46 million, driving a net loss of $12.83 million and negative operating cash flows of $8.25 million.

To avert immediate insolvency, Arrive AI secured $9.6 million in net proceeds via a January 26, 2026, convertible note (Pre-Paid Purchase No. 4) from Streeterville Capital, extending its cash runway through late Q4 2026. This $40 million debt facility acts as a double-edged sword. It features a punitive "Lookback Formula" with a $0.25 per share floor. If the volume-weighted average price (VWAP) breaches this floor, it activates a trigger mandating cash repayments of $2,887,500 per month—effectively a death knell for a company with $8.2 million in short-term liquidity. This creates a perpetual overhang, suppressing the stock price and triggering continuous share dilution.

Figure Arrive Al Strategic Blueprint for the Autonomous Last Mile (ALM)

Supply Chain Pivot & Governance DisconnectOperationally, Arrive AI has executed a strategic internalization of its engineering capabilities, scaling its full-time headcount from 8 to 41 employees. This vertical integration successfully drove down third-party R&D vendor costs from $760,036 in 2024 to $600,510 in 2025. Yet, critical supply chain vulnerabilities remain, notably a reliance on non-cancelable purchase commitments for regulated refrigerant substances required for cold-chain storage, and a heavy IT dependency on Microsoft Azure infrastructure managed by Synoptek, LLC.

More alarming is the structural decoupling between insider incentives and public shareholder value. While public equity faces relentless dilution, management aggressively extracted capital during the DPO process, including $1.86 million in one-time public-listing "success bonuses" for executives.

Furthermore, the company lacks direct ownership of its core foundational patents. The intellectual property is exclusively licensed from CEO Daniel O'Toole in a perpetual agreement that guarantees him a $25-per-unit royalty once monthly revenues scale. If the company defaults on this related-party agreement, the license reverts to non-exclusive status, stripping Arrive AI of its primary competitive moat and exposing the enterprise to catastrophic operational failure.

HDIN Institutional Perspective: A "Highest Common Denominator" CapEx Trap?

From an institutional standpoint, Arrive AI’s strategy to position itself as the "Highest Common Denominator"—a hardware-agnostic platform capable of servicing drones, autonomous mobile robots (AMRs), and human couriers—is theoretically sound. It counter-positions against the fragmented, closed-loop proprietary networks currently deployed by FedEx or Walmart.

However, macroeconomic and regulatory realities cap the near-term Total Addressable Market. Broad ALM adoption remains throttled by the Federal Aviation Administration’s (FAA) Beyond Visual Line of Sight (BVLOS) restrictions. The assumption that Arrive AI can scale to 100,000 active nodes by 2030 to achieve a 50/50 revenue split between hardware subscriptions and its "AdSense-like" ALM Marketplace ignores the systemic friction in municipal zoning and airspace regulation.

Until the regulatory environment matures to support dense, autonomous drone routing, Arrive AI is trapped in an asset-heavy CapEx cycle. It must fund the upfront manufacturing and deployment of AP4 and AP5 units while extracting nominal subscription fees from early-adopter healthcare pilots. Unless the company secures non-toxic, long-term institutional equity to bridge the gap between pilot scale and network density, the operation remains fundamentally distressed.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier global market intelligence and corporate strategy firm providing institutional-grade financial analysis. For more actionable market intelligence, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*