TSMC Consolidates AI Dominance as HPC Revenue Surges 48% Amid $56B Global CAPEX Realignment for FY2026

Date : 2026-04-20

Reading : 1655

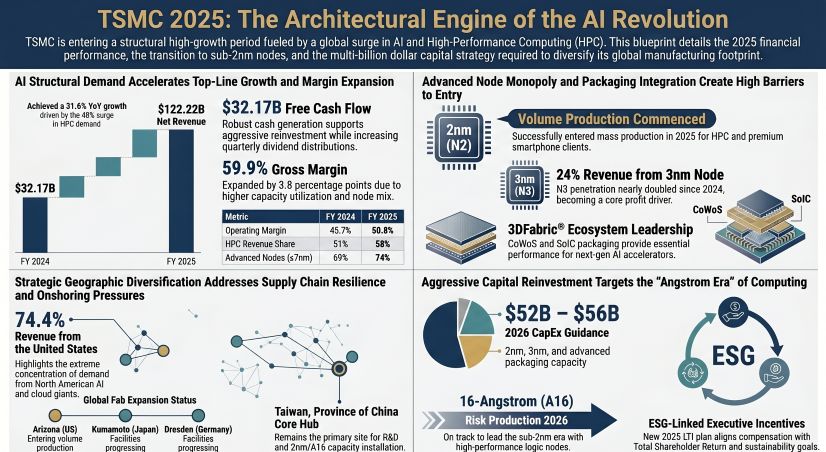

Taiwan Semiconductor Manufacturing Co. (NYSE: TSM) recorded a 31.6% revenue surge to $122.22 billion in FY2025, driven by a 48% spike in High-Performance Computing (HPC) demand across global AI infrastructures. To secure its silicon monopoly heading into FY2026, TSMC is aggressively executing a $52–$56 billion CapEx mandate to scale 2-nanometer and 16-angstrom nodes across localized fabs in Arizona, Kumamoto, and Dresden. However, this geographic decentralization exposes the foundry to severe cross-cultural labor frictions, U.S. export controls, and structural resource constraints tied to localized feedstock sourcing and impending environmental compliance.

Financial Health & Operational Moats: The 3DFabric Lock-In

TSMC’s FY2025 audit reveals an entity that has decoupled from traditional semiconductor cyclicality, morphing into the definitive toll bridge for global AI commercialization. Gross margins expanded to 59.9% (up from 56.1%), translating to an operating margin of 50.8%. This profitability surge is not merely a function of volume; it represents ruthless pricing power in advanced logic. Advanced nodes (7nm and below) now constitute 74% of total wafer revenue, with the 3nm family alone capturing 24%.

The underlying moat, however, extends beyond raw node progression. While legacy automotive and smartphone platforms navigated prolonged inventory de-stocking, TSMC’s HPC segment generated $70.36 billion. The foundry is effectively executing a form of vertical integration through its 3DFabric® advanced packaging suite (CoWoS and TSMC-SoIC). By interlocking silicon fabrication with proprietary high-density packaging, TSMC binds hyperscaler architectures to its ecosystem, creating an insurmountable switching cost for fabless designers.

Financially, this operational leverage generated $72.99 billion in Operating Cash Flow (OCF), leaving an estimated $32.17 billion in Free Cash Flow. Crucially, this self-funding matrix allows TSMC to digest an unprecedented $40.83 billion FY2025 CapEx without external debt reliance, eschewing traditional accretive acquisitions in favor of organic joint-venture scaling (e.g., JASM in Japan, ESMC in Germany).

Figure TSMC 2025 The Architectural Engine of the Al Revolution

Supply Chain Pivot: Decentralization and Tariff Geopolitics

Supply Chain Pivot: Decentralization and Tariff Geopolitics

The transition from a highly concentrated hub in Taiwan, Province of China, to a decentralized global footprint is injecting severe friction into TSMC's historically pristine operational model. U.S. and European subsidies ($6.6 billion under the U.S. CHIPS Act and €5 billion via the European Chips Act) offset immediate facility CapEx at Fab 21 (Arizona) and Fab 24 (Dresden), but they do not solve the structural margin compression inherent in fragmented supply chains.

The FY2025 disclosures expose a hyper-vulnerability to geopolitical trade barriers. With the U.S. imposing a 10% baseline tariff and a 25% ad valorem tariff on advanced computing imports, TSMC is forced to execute rigorous cost-pass-through mechanisms to shield its bottom line from localized raw material inflation and escalated equipment costs. Furthermore, TSMC is actively dismantling its sole-sourced dependency on silicon wafers and specialty gases through mandatory "dual-plant qualifications." The company's specialized cross-functional task force now dictates that primary suppliers must physically divide their production across at least two distinct geographic facilities to meet strict new Business Continuity Plan (BCP) thresholds.

HDIN Institutional Perspective: The "Invisible" Constraints of 2026

Our institutional analysis indicates that TSMC’s expansion ceiling is no longer dictated by capital or technological capability, but by ecological and human capital deficits.

First, the transition to the 16-angstrom era faces rigid environmental boundaries. TSMC has secured 7.3 GW in renewable Power Purchase Agreements (PPAs), an aggressive maneuver to pre-empt the direct financial liabilities of the 2026 carbon fee implementation in Taiwan, Province of China. Power reliability and water scarcity have officially escalated from ESG talking points to hard caps on fab utilization rates.

Second, the demographic reality of managing 90,557 employees across fragmented borders is straining TSMC’s traditional agility. The inability to rapidly reassign engineers across overseas sites due to immigration controls has forced a total overhaul of corporate compensation. The 2025 rollout of a trust-funded Long-Term Incentive (LTI) plan—tied to ESG metrics and relative S&P 500 IT Index TSR—signals a structural pivot from short-term cash profit-sharing to equity-driven retention. TSMC is no longer just battling Intel or Samsung for node supremacy; it is fighting a localized, trench-warfare battle against global talent poaching to staff its $56 billion future.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic intelligence and equity research firm dedicated to decoding complex corporate filings and macroeconomic shifts. We deliver institutional-grade market intelligence to empower precise, data-driven investment strategies. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The 3DFabric Lock-In

TSMC’s FY2025 audit reveals an entity that has decoupled from traditional semiconductor cyclicality, morphing into the definitive toll bridge for global AI commercialization. Gross margins expanded to 59.9% (up from 56.1%), translating to an operating margin of 50.8%. This profitability surge is not merely a function of volume; it represents ruthless pricing power in advanced logic. Advanced nodes (7nm and below) now constitute 74% of total wafer revenue, with the 3nm family alone capturing 24%.

The underlying moat, however, extends beyond raw node progression. While legacy automotive and smartphone platforms navigated prolonged inventory de-stocking, TSMC’s HPC segment generated $70.36 billion. The foundry is effectively executing a form of vertical integration through its 3DFabric® advanced packaging suite (CoWoS and TSMC-SoIC). By interlocking silicon fabrication with proprietary high-density packaging, TSMC binds hyperscaler architectures to its ecosystem, creating an insurmountable switching cost for fabless designers.

Financially, this operational leverage generated $72.99 billion in Operating Cash Flow (OCF), leaving an estimated $32.17 billion in Free Cash Flow. Crucially, this self-funding matrix allows TSMC to digest an unprecedented $40.83 billion FY2025 CapEx without external debt reliance, eschewing traditional accretive acquisitions in favor of organic joint-venture scaling (e.g., JASM in Japan, ESMC in Germany).

Figure TSMC 2025 The Architectural Engine of the Al Revolution

Supply Chain Pivot: Decentralization and Tariff GeopoliticsThe transition from a highly concentrated hub in Taiwan, Province of China, to a decentralized global footprint is injecting severe friction into TSMC's historically pristine operational model. U.S. and European subsidies ($6.6 billion under the U.S. CHIPS Act and €5 billion via the European Chips Act) offset immediate facility CapEx at Fab 21 (Arizona) and Fab 24 (Dresden), but they do not solve the structural margin compression inherent in fragmented supply chains.

The FY2025 disclosures expose a hyper-vulnerability to geopolitical trade barriers. With the U.S. imposing a 10% baseline tariff and a 25% ad valorem tariff on advanced computing imports, TSMC is forced to execute rigorous cost-pass-through mechanisms to shield its bottom line from localized raw material inflation and escalated equipment costs. Furthermore, TSMC is actively dismantling its sole-sourced dependency on silicon wafers and specialty gases through mandatory "dual-plant qualifications." The company's specialized cross-functional task force now dictates that primary suppliers must physically divide their production across at least two distinct geographic facilities to meet strict new Business Continuity Plan (BCP) thresholds.

HDIN Institutional Perspective: The "Invisible" Constraints of 2026

Our institutional analysis indicates that TSMC’s expansion ceiling is no longer dictated by capital or technological capability, but by ecological and human capital deficits.

First, the transition to the 16-angstrom era faces rigid environmental boundaries. TSMC has secured 7.3 GW in renewable Power Purchase Agreements (PPAs), an aggressive maneuver to pre-empt the direct financial liabilities of the 2026 carbon fee implementation in Taiwan, Province of China. Power reliability and water scarcity have officially escalated from ESG talking points to hard caps on fab utilization rates.

Second, the demographic reality of managing 90,557 employees across fragmented borders is straining TSMC’s traditional agility. The inability to rapidly reassign engineers across overseas sites due to immigration controls has forced a total overhaul of corporate compensation. The 2025 rollout of a trust-funded Long-Term Incentive (LTI) plan—tied to ESG metrics and relative S&P 500 IT Index TSR—signals a structural pivot from short-term cash profit-sharing to equity-driven retention. TSMC is no longer just battling Intel or Samsung for node supremacy; it is fighting a localized, trench-warfare battle against global talent poaching to staff its $56 billion future.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic intelligence and equity research firm dedicated to decoding complex corporate filings and macroeconomic shifts. We deliver institutional-grade market intelligence to empower precise, data-driven investment strategies. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*