Besterra Consolidates Decarbonized Demolition Market as Asset-Light Engineering Pivot Doubles FY2026 Operating Profit

Date : 2026-04-21

Reading : 74

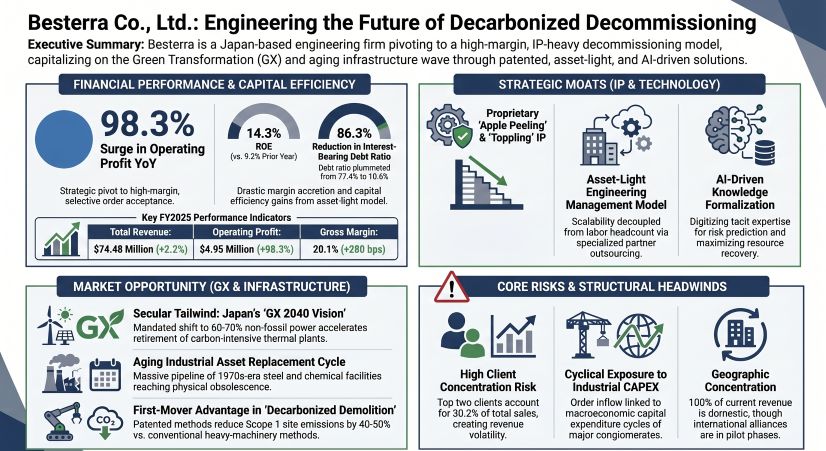

In the FY2026 audit, Tokyo-based Besterra Co., Ltd. (TYO: 1433) aggressively executed a structural profitability pivot within Japan's complex industrial dismantling sector. By weaponizing an IP-driven, asset-light engineering model against chronic domestic labor shortages, the firm successfully doubled its operating profit to $4.95 million. Catalyzed by Japan’s national GX 2040 decarbonization mandate, Besterra’s strict selective order strategy and severe balance sheet deleveraging insulate the firm from heavy construction volatility, positioning it to capture the multi-decade pipeline of legacy thermal and nuclear power plant retirements.

Financial Health & Operational Moats: Engineering an IP-Leveraged Margin Expansion

Besterra’s FY2026 financial architecture demonstrates a deliberate rejection of low-quality volume in favor of rigorous margin expansion. While top-line consolidated revenue saw a disciplined 2.2% YoY growth to $74.48 million (11.14 billion JPY), operating profit surged 98.3% to $4.95 million, driving operating margins from 3.4% to 6.7%.

This is not a byproduct of cyclical luck; it is a structural moat. Traditional demolition contractors suffer from acute margin compression due to volatile heavy machinery depreciation and blue-collar wage inflation. Besterra bypasses these headwinds through an elite engineering management model. By strictly deploying proprietary patents—most notably the gravity-driven "Apple Peeling Method" for spherical tanks and the "Wind Turbine Toppling Method"—the company slashes project construction time by up to 65%.

The "So What" for institutional investors is the balance sheet transformation. Driven by robust operating cash flow ($10.99 million) and strict adherence to Corporate Governance Code mandates, Besterra liquidated $9.45 million in strategic cross-shareholdings. Management weaponized this liquidity to entirely eliminate $20.06 million in short-term debt, driving the equity ratio to an impenetrable 64.8%. This deleveraging, paired with accretive share cancellations (1.44 million treasury shares) and progressive dividend hikes (targeting >3.5% DOE), catapulted ROE to 14.3%. With an asset turnover ratio of 1.34x, Besterra behaves less like a heavy industrial contractor and more like a high-tier specialty engineering consultancy.

Figure Besterra Engineering the Future of Decarbonized Decommissioning

Supply Chain Pivot: Coopetition and Circular Economy Integration

Supply Chain Pivot: Coopetition and Circular Economy Integration

Besterra has structurally engineered its supply chain to sidestep the systemic demographic decay crippling Japan's construction sector. Generating approximately $402,600 in sales per employee, the company outsources physical labor and heavy machinery operations to a highly vetted network of specialized partner firms. This limits fixed-cost exposure and negates the need for the complex cost-pass-through mechanisms that drag down traditional general contractors during inflationary periods.

Furthermore, Besterra has seamlessly integrated vertical integration tactics into the downstream circular economy. Industrial dismantling inherently yields massive volumes of high-value scrap (iron, copper, stainless steel). Rather than treating this as waste, Besterra evaluates real-time market prices during the bidding phase and factors scrap monetization directly into contract negotiations. In tandem with their J&T Environment alliance, these scrap sales are aggressively captured as completed construction revenue, effectively subsidizing the primary project costs and artificially suppressing top-line volatility.

HDIN Institutional Perspective: Riding the GX 2040 CAPEX Cycle

From an institutional standpoint, Besterra’s near-term underperformance against its previous top-line targets is largely irrelevant. Management’s recalibrated "Leading the Future 2030" plan—targeting over $200.58 million (30 billion JPY) in revenue with an ROE exceeding 20%—is highly credible when mapped against macroeconomic catalysts.

Besterra's order book is hyper-sensitive to the CAPEX cycles of Japanese heavy industry, with clients like Nippon Steel (Nittetsu Texeng) and JFE Plant Engineering constituting the core of their $56.91 million project backlog. The macro trigger here is the Japanese government’s "GX 2040 Vision," which mandates a 60-70% non-fossil power grid. This policy guarantees a multi-decade CAPEX super-cycle focused on retiring carbon-intensive thermal assets.

Besterra is fundamentally decoupling its revenue growth from human headcount. By utilizing the remote-controlled "Ringo☆Star" gas-cutting robot and commercializing BIM-compatible 3D-CAD measurements, the firm translates tacit demolition knowledge into scalable AI models. Crucially, its strategic alliance with Hitachi Plant Construction signals a quiet but highly lucrative entry into the nuclear decommissioning space. As Japan accelerates its energy transition, Besterra’s ability to offer "Decarbonized Decommissioning" (cutting CO2 emissions at the work site by up to 50%) transitions the firm from a simple subcontractor into a critical ESG-compliance partner for Japan's industrial titans.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in dissecting complex corporate filings to deliver predictive strategic analysis. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Engineering an IP-Leveraged Margin Expansion

Besterra’s FY2026 financial architecture demonstrates a deliberate rejection of low-quality volume in favor of rigorous margin expansion. While top-line consolidated revenue saw a disciplined 2.2% YoY growth to $74.48 million (11.14 billion JPY), operating profit surged 98.3% to $4.95 million, driving operating margins from 3.4% to 6.7%.

This is not a byproduct of cyclical luck; it is a structural moat. Traditional demolition contractors suffer from acute margin compression due to volatile heavy machinery depreciation and blue-collar wage inflation. Besterra bypasses these headwinds through an elite engineering management model. By strictly deploying proprietary patents—most notably the gravity-driven "Apple Peeling Method" for spherical tanks and the "Wind Turbine Toppling Method"—the company slashes project construction time by up to 65%.

The "So What" for institutional investors is the balance sheet transformation. Driven by robust operating cash flow ($10.99 million) and strict adherence to Corporate Governance Code mandates, Besterra liquidated $9.45 million in strategic cross-shareholdings. Management weaponized this liquidity to entirely eliminate $20.06 million in short-term debt, driving the equity ratio to an impenetrable 64.8%. This deleveraging, paired with accretive share cancellations (1.44 million treasury shares) and progressive dividend hikes (targeting >3.5% DOE), catapulted ROE to 14.3%. With an asset turnover ratio of 1.34x, Besterra behaves less like a heavy industrial contractor and more like a high-tier specialty engineering consultancy.

Figure Besterra Engineering the Future of Decarbonized Decommissioning

Supply Chain Pivot: Coopetition and Circular Economy IntegrationBesterra has structurally engineered its supply chain to sidestep the systemic demographic decay crippling Japan's construction sector. Generating approximately $402,600 in sales per employee, the company outsources physical labor and heavy machinery operations to a highly vetted network of specialized partner firms. This limits fixed-cost exposure and negates the need for the complex cost-pass-through mechanisms that drag down traditional general contractors during inflationary periods.

Furthermore, Besterra has seamlessly integrated vertical integration tactics into the downstream circular economy. Industrial dismantling inherently yields massive volumes of high-value scrap (iron, copper, stainless steel). Rather than treating this as waste, Besterra evaluates real-time market prices during the bidding phase and factors scrap monetization directly into contract negotiations. In tandem with their J&T Environment alliance, these scrap sales are aggressively captured as completed construction revenue, effectively subsidizing the primary project costs and artificially suppressing top-line volatility.

HDIN Institutional Perspective: Riding the GX 2040 CAPEX Cycle

From an institutional standpoint, Besterra’s near-term underperformance against its previous top-line targets is largely irrelevant. Management’s recalibrated "Leading the Future 2030" plan—targeting over $200.58 million (30 billion JPY) in revenue with an ROE exceeding 20%—is highly credible when mapped against macroeconomic catalysts.

Besterra's order book is hyper-sensitive to the CAPEX cycles of Japanese heavy industry, with clients like Nippon Steel (Nittetsu Texeng) and JFE Plant Engineering constituting the core of their $56.91 million project backlog. The macro trigger here is the Japanese government’s "GX 2040 Vision," which mandates a 60-70% non-fossil power grid. This policy guarantees a multi-decade CAPEX super-cycle focused on retiring carbon-intensive thermal assets.

Besterra is fundamentally decoupling its revenue growth from human headcount. By utilizing the remote-controlled "Ringo☆Star" gas-cutting robot and commercializing BIM-compatible 3D-CAD measurements, the firm translates tacit demolition knowledge into scalable AI models. Crucially, its strategic alliance with Hitachi Plant Construction signals a quiet but highly lucrative entry into the nuclear decommissioning space. As Japan accelerates its energy transition, Besterra’s ability to offer "Decarbonized Decommissioning" (cutting CO2 emissions at the work site by up to 50%) transitions the firm from a simple subcontractor into a critical ESG-compliance partner for Japan's industrial titans.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in dissecting complex corporate filings to deliver predictive strategic analysis. (www.hdinresearch.com)

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*