CIQTEK Challenges Bruker and Thermo Fisher Dominance: Quantum Pioneer Targets 2026 Profitability on 46.98% Gross Margin Expansion

Date : 2026-04-22

Reading : 272

Hefei-based CIQTEK is aggressively dismantling the high-end scientific instrument monopolies historically controlled by Western and Japanese conglomerates. Driven by a 29.11% three-year revenue CAGR to $92.69 million in FY2025, the University of Science and Technology of China (USTC) spin-off is leveraging severe geopolitical export controls to capture domestic market share. With operating cash flow inflecting to a positive $16.46 million, CIQTEK is deploying a planned $208.56 million IPO to fund global application centers, weaponizing localized vertical integration to challenge incumbents like Thermo Fisher and Bruker on a structural profitability target of 2026.

Financial Health & Operational Moats: The Cash Flow Inflection

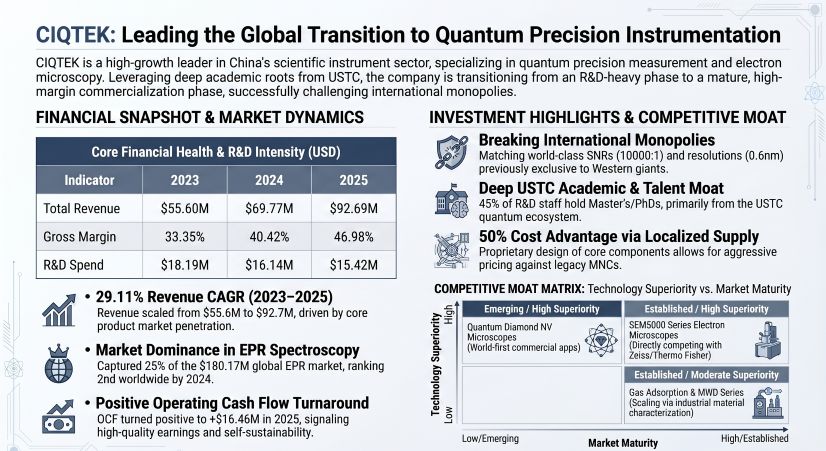

CIQTEK’s FY2025 audit reveals a classic transition from an intensive R&D burn phase to scalable commercialization. While the headline accounting figure shows a net loss of -$0.81 million, this metric obscures a highly robust underlying earnings quality. Operating Cash Flow (OCF) surged to +$16.46 million, driven by the absorption of heavy non-cash expenses, including $3.45 million in share-based compensation required to retain top-tier quantum physicists.

The company's gross margin expansion—from 33.35% in 2023 to 46.98% in FY2025—signals a material shift in product mix and pricing power. The Electron Microscope (EM) segment has officially overtaken the foundational Quantum & Spin Resonance division as the primary revenue engine, generating $51.90 million (56.29% of total revenue). By offering instruments with technical parity to international rivals—such as Field Emission SEMs achieving 0.6nm@15kV resolution—at roughly a 50% price discount, CIQTEK is driving economies of scale that dilute fixed costs.

Furthermore, the company’s bottom line is structurally supported by high-visibility government subsidies. Totalling $6.38 million in 2025, these cash inflows are not one-off windfalls but sustainable, operationally linked software VAT refunds and national R&D grants that effectively underwrite the company's aggressive market-capture pricing strategy.

Figure ClOTEK Leading the Global Transition to Quantum Precision Instrumentation

Supply Chain Pivot: Geopolitics as a Structural Catalyst

Supply Chain Pivot: Geopolitics as a Structural Catalyst

Global technology export controls have inadvertently engineered a massive domestic substitution moat for CIQTEK. The US Entity List and Japan’s April 2024 export restrictions on scanning electron microscopes for semiconductor applications have forced Chinese research institutions and industrial enterprises into a rapid procurement pivot.

To mitigate upstream macro risks, CIQTEK has achieved high self-sufficiency in critical engine nodes, vertically integrating the production of Electron Paramagnetic Resonance (EPR) probes, precise electron/ion guns, and low-ripple high-voltage power supplies. However, residual supply chain vulnerabilities remain. The company still relies on international channels for highly specialized sub-components, evidenced by its procurement of vacuum pumps from Edwards Trading (Shanghai) and specific detectors from Anhui Xin'an. Moving forward, maintaining bargaining power against these fragmented tier-2 suppliers while aggressively scaling its "build-to-order" production model will be critical for working capital management.

The Global Push: Breaching the "Import Worship" Barrier

Despite domestic dominance—capturing roughly 25% of the global EPR sales scale and ranking first among domestic SEM brands—CIQTEK’s overseas revenue penetration sits at just 12.95%. Institutional and academic clients exhibit notoriously high switching costs and entrenched brand loyalty to legacy incumbents like JEOL and Zeiss.

To break this bottleneck, CIQTEK is allocating $36.85 million of its IPO proceeds directly into an Application Center Network Construction Project. By deploying decentralized testing laboratories and showrooms across North America, Europe, and Southeast Asia, the company aims to eliminate cross-border service delays and directly challenge the post-sales technical support moats of multinational conglomerates in their home territories.

HDIN Institutional Perspective: The Governance and Scale Test

From an institutional vantage point, CIQTEK's trajectory signals a broader cyclical peak in the domestic substitution narrative and the beginning of a genuine global competitive phase for Chinese scientific instruments. However, the operational pivot from an academic lab to a decentralized manufacturing powerhouse introduces acute corporate governance risks.

The company’s equity structure is heavily dispersed. Actual controllers He Yu and Rong Xing rely entirely on a Concert Party Agreement governing just 34.87% of pre-IPO voting rights (projected to dilute to 31.38% post-IPO). Should friction arise between the core USTC academic founders and institutional investors (such as Hillhouse) regarding the pace of global capital expenditure versus near-term margin compression, control stability could be threatened.

Ultimately, CIQTEK’s 2026 profitability target is highly credible, provided it can manage its extended Accounts Receivable collection cycle (3.28 turnover ratio in FY2025) typical of state-owned downstream clients, and successfully convert its $109.19 million Industrialization Project into standardized manufacturing output without inflating inventory obsolescence.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

Visit www.hdinresearch.com for more institutional market intelligence.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cash Flow Inflection

CIQTEK’s FY2025 audit reveals a classic transition from an intensive R&D burn phase to scalable commercialization. While the headline accounting figure shows a net loss of -$0.81 million, this metric obscures a highly robust underlying earnings quality. Operating Cash Flow (OCF) surged to +$16.46 million, driven by the absorption of heavy non-cash expenses, including $3.45 million in share-based compensation required to retain top-tier quantum physicists.

The company's gross margin expansion—from 33.35% in 2023 to 46.98% in FY2025—signals a material shift in product mix and pricing power. The Electron Microscope (EM) segment has officially overtaken the foundational Quantum & Spin Resonance division as the primary revenue engine, generating $51.90 million (56.29% of total revenue). By offering instruments with technical parity to international rivals—such as Field Emission SEMs achieving 0.6nm@15kV resolution—at roughly a 50% price discount, CIQTEK is driving economies of scale that dilute fixed costs.

Furthermore, the company’s bottom line is structurally supported by high-visibility government subsidies. Totalling $6.38 million in 2025, these cash inflows are not one-off windfalls but sustainable, operationally linked software VAT refunds and national R&D grants that effectively underwrite the company's aggressive market-capture pricing strategy.

Figure ClOTEK Leading the Global Transition to Quantum Precision Instrumentation

Supply Chain Pivot: Geopolitics as a Structural CatalystGlobal technology export controls have inadvertently engineered a massive domestic substitution moat for CIQTEK. The US Entity List and Japan’s April 2024 export restrictions on scanning electron microscopes for semiconductor applications have forced Chinese research institutions and industrial enterprises into a rapid procurement pivot.

To mitigate upstream macro risks, CIQTEK has achieved high self-sufficiency in critical engine nodes, vertically integrating the production of Electron Paramagnetic Resonance (EPR) probes, precise electron/ion guns, and low-ripple high-voltage power supplies. However, residual supply chain vulnerabilities remain. The company still relies on international channels for highly specialized sub-components, evidenced by its procurement of vacuum pumps from Edwards Trading (Shanghai) and specific detectors from Anhui Xin'an. Moving forward, maintaining bargaining power against these fragmented tier-2 suppliers while aggressively scaling its "build-to-order" production model will be critical for working capital management.

The Global Push: Breaching the "Import Worship" Barrier

Despite domestic dominance—capturing roughly 25% of the global EPR sales scale and ranking first among domestic SEM brands—CIQTEK’s overseas revenue penetration sits at just 12.95%. Institutional and academic clients exhibit notoriously high switching costs and entrenched brand loyalty to legacy incumbents like JEOL and Zeiss.

To break this bottleneck, CIQTEK is allocating $36.85 million of its IPO proceeds directly into an Application Center Network Construction Project. By deploying decentralized testing laboratories and showrooms across North America, Europe, and Southeast Asia, the company aims to eliminate cross-border service delays and directly challenge the post-sales technical support moats of multinational conglomerates in their home territories.

HDIN Institutional Perspective: The Governance and Scale Test

From an institutional vantage point, CIQTEK's trajectory signals a broader cyclical peak in the domestic substitution narrative and the beginning of a genuine global competitive phase for Chinese scientific instruments. However, the operational pivot from an academic lab to a decentralized manufacturing powerhouse introduces acute corporate governance risks.

The company’s equity structure is heavily dispersed. Actual controllers He Yu and Rong Xing rely entirely on a Concert Party Agreement governing just 34.87% of pre-IPO voting rights (projected to dilute to 31.38% post-IPO). Should friction arise between the core USTC academic founders and institutional investors (such as Hillhouse) regarding the pace of global capital expenditure versus near-term margin compression, control stability could be threatened.

Ultimately, CIQTEK’s 2026 profitability target is highly credible, provided it can manage its extended Accounts Receivable collection cycle (3.28 turnover ratio in FY2025) typical of state-owned downstream clients, and successfully convert its $109.19 million Industrialization Project into standardized manufacturing output without inflating inventory obsolescence.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

Visit www.hdinresearch.com for more institutional market intelligence.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*