LSE: Ceres Power Shifts from NRE to Commercial Royalties as Asian Licensees Deploy $224M CAPEX to Target AI Data Center Energy Deficits

Date : 2026-04-20

Reading : 849

Following its FY2025 audit, Ceres Power (LSE: CWR) has officially transitioned from an R&D-heavy licensing model to a recurring royalty generator. Headquartered in the UK, the company leverages Tier-1 manufacturing partners across Asia (Doosan, Delta Electronics, Weichai) to commercialize its solid oxide fuel cell (SOFC) and electrolysis (SOEC) technology. By sidelining heavy CAPEX requirements and targeting 800V DC power architectures directly aligned with AI data center requirements, Ceres is exploiting severe grid bottlenecks to secure a high-margin foothold in the global clean power and green hydrogen markets.

Financial Health & Operational Moats: The End of the NRE Trough

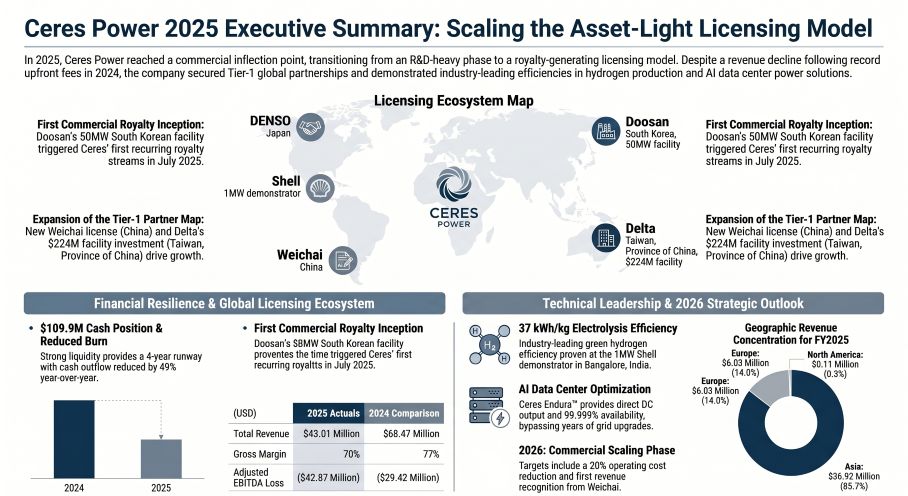

Ceres’ FY2025 financial disclosures reveal a classic inflection point for an asset-light intellectual property (IP) licensor. The company reported a 37% top-line revenue contraction to $43.01 million (£32.6 million). Institutional observers should not misread this as market share erosion; rather, it reflects the structural lumpiness of upfront Non-Recurring Engineering (NRE) fees and technology transfer revenues recognized during the 2024 onboarding of Delta and DENSO.

In July 2025, Doosan commenced mass market production at its first-of-a-kind 50MW facility in Jeollabuk-do, South Korea, triggering Ceres’ first-ever commercial royalty streams ($145,112). While currently a fractional revenue contributor, this proves the viability of Ceres' endpoint monetization strategy.

Ceres maintained a robust 70% gross margin—a direct reflection of its IP-centric moat. Backed by $109.89 million (£83.3 million) in cash reserves and a freshly implemented corporate restructuring aimed at a 20% operating expense reduction for 2026, the company holds roughly 4.3 years of operational runway. However, analysts must track the surge in deferred income (contract liabilities), which swelled to $30.71 million. While this provides a short-term working capital buffer, it cements significant future performance obligations that will test the company's newly streamlined cross-functional operations.

Figure Ceres Power 2025 Executive Summary: Scaling the Asset-Light Licensing Model

Supply Chain Pivot: Insulating Margins from Rare-Earth Volatility

Supply Chain Pivot: Insulating Margins from Rare-Earth Volatility

As global supply chains face systemic inflationary pressure and geopolitical fragmentation, Ceres leverages its proprietary "Ceres Endura™" architecture to engineer out supply chain risk. Competing Proton Exchange Membrane (PEM) electrolyzers are heavily reliant on highly expensive, rare-earth metal catalysts. Ceres deliberately utilizes a metal-supported ceramic cell structure, utilizing base materials that bypass rare-earth feedstock bottlenecks and shield manufacturing partners from sudden cost-pass-through mechanisms.

Simultaneously, Ceres is forcing bill of materials (BOM) localization by shifting capital expenditure burdens to its global licensees. Delta Electronics has committed $224.26 million (NT$6.95 billion) to acquire land and facilities in Taiwan, targeting pilot production by late 2026. Concurrently, the newly signed November 2025 manufacturing license with Weichai will establish a localized footprint in Shandong, China. This multi-sourcing strategy absorbed the shock of Bosch’s strategic divestment of its 17.4% equity stake earlier in the year, proving the resilience of an aggressively decentralized, midstream manufacturing network.

HDIN Institutional Perspective: The AI Data Center Catalyst

Ceres is perfectly positioned at the intersection of a severe macro trend: the structural energy deficit driven by artificial intelligence. Traditional grid upgrades required for gigawatt-scale data centers face permitting purgatories of up to 15 years in the EU and North America.

Ceres’ SOFCs bypass these grid constraints entirely, delivering microgrid power in a matter of months with 99.999% availability. Crucially, the Ceres Endura™ platform natively outputs stable Direct Current (DC) power. This aligns seamlessly with the 800V DC architectures required by next-generation AI GPUs, completely eliminating the energy loss typically associated with AC/DC inverter conversions.

From an institutional standpoint, the FY2025 data signals that Ceres has survived the "valley of death" inherent to hardware R&D. The successful demonstration of 37 kWh/kg SOEC efficiency at Shell’s 1MW Bangalore demonstrator proves the technical floor, but the immediate alpha lies in the stationary power market. As Weichai and Delta bring multi-gigawatt targeted capacities online, Ceres is primed for significant operating leverage, converting today's deferred engineering contracts into tomorrow's accretive, high-margin royalties.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic advisory and market intelligence firm delivering institutional-grade financial analysis. We specialize in decoding complex corporate filings to provide actionable, macroeconomic insights for global equity markets and institutional investors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The End of the NRE Trough

Ceres’ FY2025 financial disclosures reveal a classic inflection point for an asset-light intellectual property (IP) licensor. The company reported a 37% top-line revenue contraction to $43.01 million (£32.6 million). Institutional observers should not misread this as market share erosion; rather, it reflects the structural lumpiness of upfront Non-Recurring Engineering (NRE) fees and technology transfer revenues recognized during the 2024 onboarding of Delta and DENSO.

In July 2025, Doosan commenced mass market production at its first-of-a-kind 50MW facility in Jeollabuk-do, South Korea, triggering Ceres’ first-ever commercial royalty streams ($145,112). While currently a fractional revenue contributor, this proves the viability of Ceres' endpoint monetization strategy.

Ceres maintained a robust 70% gross margin—a direct reflection of its IP-centric moat. Backed by $109.89 million (£83.3 million) in cash reserves and a freshly implemented corporate restructuring aimed at a 20% operating expense reduction for 2026, the company holds roughly 4.3 years of operational runway. However, analysts must track the surge in deferred income (contract liabilities), which swelled to $30.71 million. While this provides a short-term working capital buffer, it cements significant future performance obligations that will test the company's newly streamlined cross-functional operations.

Figure Ceres Power 2025 Executive Summary: Scaling the Asset-Light Licensing Model

Supply Chain Pivot: Insulating Margins from Rare-Earth VolatilityAs global supply chains face systemic inflationary pressure and geopolitical fragmentation, Ceres leverages its proprietary "Ceres Endura™" architecture to engineer out supply chain risk. Competing Proton Exchange Membrane (PEM) electrolyzers are heavily reliant on highly expensive, rare-earth metal catalysts. Ceres deliberately utilizes a metal-supported ceramic cell structure, utilizing base materials that bypass rare-earth feedstock bottlenecks and shield manufacturing partners from sudden cost-pass-through mechanisms.

Simultaneously, Ceres is forcing bill of materials (BOM) localization by shifting capital expenditure burdens to its global licensees. Delta Electronics has committed $224.26 million (NT$6.95 billion) to acquire land and facilities in Taiwan, targeting pilot production by late 2026. Concurrently, the newly signed November 2025 manufacturing license with Weichai will establish a localized footprint in Shandong, China. This multi-sourcing strategy absorbed the shock of Bosch’s strategic divestment of its 17.4% equity stake earlier in the year, proving the resilience of an aggressively decentralized, midstream manufacturing network.

HDIN Institutional Perspective: The AI Data Center Catalyst

Ceres is perfectly positioned at the intersection of a severe macro trend: the structural energy deficit driven by artificial intelligence. Traditional grid upgrades required for gigawatt-scale data centers face permitting purgatories of up to 15 years in the EU and North America.

Ceres’ SOFCs bypass these grid constraints entirely, delivering microgrid power in a matter of months with 99.999% availability. Crucially, the Ceres Endura™ platform natively outputs stable Direct Current (DC) power. This aligns seamlessly with the 800V DC architectures required by next-generation AI GPUs, completely eliminating the energy loss typically associated with AC/DC inverter conversions.

From an institutional standpoint, the FY2025 data signals that Ceres has survived the "valley of death" inherent to hardware R&D. The successful demonstration of 37 kWh/kg SOEC efficiency at Shell’s 1MW Bangalore demonstrator proves the technical floor, but the immediate alpha lies in the stationary power market. As Weichai and Delta bring multi-gigawatt targeted capacities online, Ceres is primed for significant operating leverage, converting today's deferred engineering contracts into tomorrow's accretive, high-margin royalties.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic advisory and market intelligence firm delivering institutional-grade financial analysis. We specialize in decoding complex corporate filings to provide actionable, macroeconomic insights for global equity markets and institutional investors. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*