Gorilla Technology Accelerates Sovereign GPUaaS Pivot as FY2025 Audit Reveals 35.7% Revenue Surge Masking Structural Cash Burn

Date : 2026-04-22

Reading : 123

In FY2025, Gorilla Technology Group Inc. (NASDAQ: GRRR) posted a 35.7% year-over-year revenue expansion to $101.36 million, driven almost entirely by a firm-fixed-price government contract in Egypt. While physically routing 99.9% of its recognized revenues through legal entities in Taiwan, Province of China, the firm is aggressively pivoting its operational footprint toward Southeast Asia to deploy a commercial GPU-as-a-Service (GPUaaS) model. This structural transition is a necessary response to an unhedged $25.65 million foreign exchange loss, severe working capital bottlenecks, and a 16.6-point gross margin compression inherently tied to its legacy sovereign deployments.

Financial Health & Operational Moats: The Sovereign AI Liquidity Trap

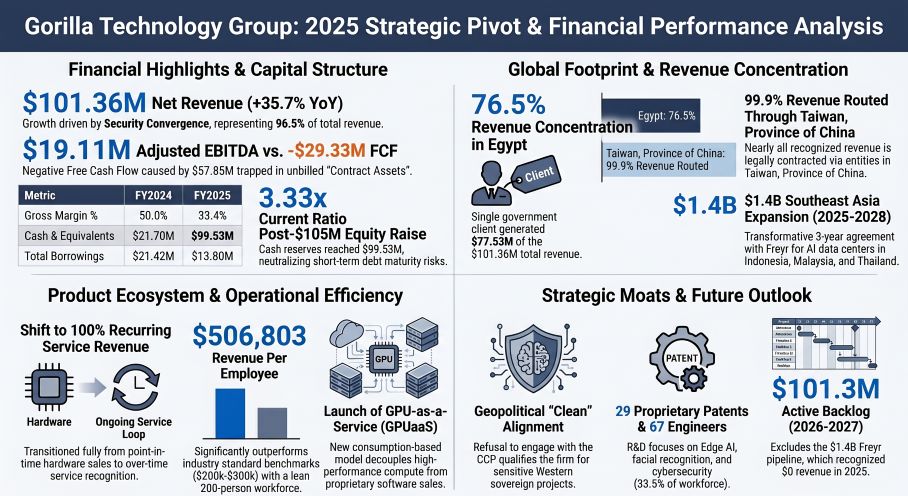

Gorilla Technology’s FY2025 financial profile illustrates a profound disconnect between statutory IFRS growth and underlying cash generation. While the top line expanded to $101.36 million—fueled overwhelmingly (96.5%) by the Security Convergence segment—this revenue mix shift cannibalized historical profitability. Gross margins collapsed from 50.0% to 33.4% as the firm transitioned from high-margin pure-play software licensing to lower-margin, hardware-heavy integration projects in emerging markets.

The true operational narrative is written on the balance sheet via a severe working capital drag. Despite posting a non-IFRS Adjusted EBITDA of $19.11 million, operating cash flow bled $(28.66) million. The primary culprit is the rigid milestone billing structure of the EGP 8.4 billion Government of Egypt contract. Lacking effective cost-pass-through mechanisms, Gorilla is structurally forced to fund hardware procurement and engineering labor upfront, swelling unbilled Contract Assets by $23.54 million year-over-year to a staggering $57.85 million. The firm is successfully recognizing accounting profits but failing the critical conversion test into operational cash.

To avert a liquidity crisis, management executed a highly dilutive $105 million registered direct equity offering in July 2025. This capital injection artificially de-risked the balance sheet, pushing Cash & Equivalents to $99.53 million and generating a highly liquid 3.33x current ratio that easily covers the $10.39 million in short-term debt maturities. However, utilizing external capital markets to continuously fund sovereign working capital bottlenecks does not constitute a sustainable, long-term operational moat.

Figure Gorilla Technology Group 2025 Strategic Pivot & Financial Performance Analysis

Supply Chain Pivot & Infrastructure Realignment

Supply Chain Pivot & Infrastructure Realignment

To escape the margin dilution of bespoke government integration, Gorilla is executing a massive supply chain pivot toward commercial enterprise infrastructure, anchored by a $1.4 billion, 3-year agreement with Freyr Technology AI Pte. Ltd. across Indonesia, Malaysia, and Thailand.

Operating a fabless, R&D-lean model—where R&D intensity sits at just 3.0% of total revenue—Gorilla avoids foundational silicon manufacturing. Instead, it relies on precision white-label manufacturing partners, specifically identifying Lanner Electronics and Edgecore Networks, while deploying third-party Intel Gaudi GPUs. This architecture allows Gorilla to act as an agile integrator, focusing strictly on the application layer of its GPUaaS rollout.

However, this transition introduces intense vendor dependency. The zero-revenue recognized from the Freyr agreement in FY2025 acts as a massive "shadow backlog." Converting this $1.4 billion pipeline into active cash flow will require immense upfront CapEx and reliable access to advanced accelerators. Any global semiconductor supply chain constraints, export controls, or regional data center utility shortages will directly impair this commercial GPUaaS thesis.

Geopolitical Arbitrage and Exogenous FX Vulnerabilities

Gorilla’s deliberate refusal to engage the Chinese Communist Party or host platforms in mainland China functions as a definitive regulatory moat. By strictly aligning with Western democratic mandates, the firm qualifies for highly sensitive public sector contracts, such as the air-gapped network for Egypt and public safety tenders in Taiwan, Province of China.

Yet, this geopolitical arbitrage fails to insulate the company from emerging market macroeconomic shocks. The "clean" earnings bridge exposes a catastrophic failure to hedge fixed-price sovereign exposure. The 11.5% devaluation of the Egyptian Pound (EGP) against the USD triggered a massive $25.65 million non-cash foreign currency translation loss. Concurrently, the company authorized a $7.35 million direct write-off of uncollectible accounts receivable from legacy clients, signaling a desperate clearing of low-quality historical assets to prepare the balance sheet for the GPUaaS pivot.

HDIN Institutional Perspective: A Sector-Wide Signal

Gorilla’s FY2025 audit signals a broader cyclical reality for the Edge AI and cybersecurity sectors: the transition from discrete software sales to sovereign AI infrastructure is brutally capital-intensive and highly dilutive in its early stages.

We view Gorilla's current state as a high-stakes transition phase. The management team is heavily incentivized by a strict "pay-for-performance" model, with 2.51 million Restricted Stock Units (RSUs) granted in Q1 2026. While this aligns executive wealth with long-term market capitalization targets, it will trigger an estimated $20 million to $23 million stock-based compensation drag on FY2026 earnings. Furthermore, ongoing multi-front litigation with legacy SPAC sponsors and PIPE investors over 2022/2023 earnout shares remains a structural distraction.

For Gorilla to justify its valuation multiples in 2026, it must prove that the $1.4 billion Freyr commercial pipeline can yield predictable, usage-based recurring revenues that permanently decouple the firm from unhedged emerging market public budgets. Until that shadow backlog converts to tangible operational cash flow, Gorilla remains a high-beta proxy for AI infrastructure deployment risks.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in forensic financial audits, supply chain deconstruction, and macroeconomic strategic analysis. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Sovereign AI Liquidity Trap

Gorilla Technology’s FY2025 financial profile illustrates a profound disconnect between statutory IFRS growth and underlying cash generation. While the top line expanded to $101.36 million—fueled overwhelmingly (96.5%) by the Security Convergence segment—this revenue mix shift cannibalized historical profitability. Gross margins collapsed from 50.0% to 33.4% as the firm transitioned from high-margin pure-play software licensing to lower-margin, hardware-heavy integration projects in emerging markets.

The true operational narrative is written on the balance sheet via a severe working capital drag. Despite posting a non-IFRS Adjusted EBITDA of $19.11 million, operating cash flow bled $(28.66) million. The primary culprit is the rigid milestone billing structure of the EGP 8.4 billion Government of Egypt contract. Lacking effective cost-pass-through mechanisms, Gorilla is structurally forced to fund hardware procurement and engineering labor upfront, swelling unbilled Contract Assets by $23.54 million year-over-year to a staggering $57.85 million. The firm is successfully recognizing accounting profits but failing the critical conversion test into operational cash.

To avert a liquidity crisis, management executed a highly dilutive $105 million registered direct equity offering in July 2025. This capital injection artificially de-risked the balance sheet, pushing Cash & Equivalents to $99.53 million and generating a highly liquid 3.33x current ratio that easily covers the $10.39 million in short-term debt maturities. However, utilizing external capital markets to continuously fund sovereign working capital bottlenecks does not constitute a sustainable, long-term operational moat.

Figure Gorilla Technology Group 2025 Strategic Pivot & Financial Performance Analysis

Supply Chain Pivot & Infrastructure RealignmentTo escape the margin dilution of bespoke government integration, Gorilla is executing a massive supply chain pivot toward commercial enterprise infrastructure, anchored by a $1.4 billion, 3-year agreement with Freyr Technology AI Pte. Ltd. across Indonesia, Malaysia, and Thailand.

Operating a fabless, R&D-lean model—where R&D intensity sits at just 3.0% of total revenue—Gorilla avoids foundational silicon manufacturing. Instead, it relies on precision white-label manufacturing partners, specifically identifying Lanner Electronics and Edgecore Networks, while deploying third-party Intel Gaudi GPUs. This architecture allows Gorilla to act as an agile integrator, focusing strictly on the application layer of its GPUaaS rollout.

However, this transition introduces intense vendor dependency. The zero-revenue recognized from the Freyr agreement in FY2025 acts as a massive "shadow backlog." Converting this $1.4 billion pipeline into active cash flow will require immense upfront CapEx and reliable access to advanced accelerators. Any global semiconductor supply chain constraints, export controls, or regional data center utility shortages will directly impair this commercial GPUaaS thesis.

Geopolitical Arbitrage and Exogenous FX Vulnerabilities

Gorilla’s deliberate refusal to engage the Chinese Communist Party or host platforms in mainland China functions as a definitive regulatory moat. By strictly aligning with Western democratic mandates, the firm qualifies for highly sensitive public sector contracts, such as the air-gapped network for Egypt and public safety tenders in Taiwan, Province of China.

Yet, this geopolitical arbitrage fails to insulate the company from emerging market macroeconomic shocks. The "clean" earnings bridge exposes a catastrophic failure to hedge fixed-price sovereign exposure. The 11.5% devaluation of the Egyptian Pound (EGP) against the USD triggered a massive $25.65 million non-cash foreign currency translation loss. Concurrently, the company authorized a $7.35 million direct write-off of uncollectible accounts receivable from legacy clients, signaling a desperate clearing of low-quality historical assets to prepare the balance sheet for the GPUaaS pivot.

HDIN Institutional Perspective: A Sector-Wide Signal

Gorilla’s FY2025 audit signals a broader cyclical reality for the Edge AI and cybersecurity sectors: the transition from discrete software sales to sovereign AI infrastructure is brutally capital-intensive and highly dilutive in its early stages.

We view Gorilla's current state as a high-stakes transition phase. The management team is heavily incentivized by a strict "pay-for-performance" model, with 2.51 million Restricted Stock Units (RSUs) granted in Q1 2026. While this aligns executive wealth with long-term market capitalization targets, it will trigger an estimated $20 million to $23 million stock-based compensation drag on FY2026 earnings. Furthermore, ongoing multi-front litigation with legacy SPAC sponsors and PIPE investors over 2022/2023 earnout shares remains a structural distraction.

For Gorilla to justify its valuation multiples in 2026, it must prove that the $1.4 billion Freyr commercial pipeline can yield predictable, usage-based recurring revenues that permanently decouple the firm from unhedged emerging market public budgets. Until that shadow backlog converts to tangible operational cash flow, Gorilla remains a high-beta proxy for AI infrastructure deployment risks.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in forensic financial audits, supply chain deconstruction, and macroeconomic strategic analysis. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*