Next-Generation Tobacco Incumbents Defend Market Share: CQENS Technologies Executes $1.83M Italian CAPEX Pivot Amid Pre-Commercial Cash Burn

Date : 2026-04-22

Reading : 84

CQENS Technologies Inc., a pre-revenue developer targeting the $1.1 trillion global inhalation market, is aggressively attempting to commercialize its 112-patent Heat-not-Burn (HnB) portfolio ahead of a delayed 2027 U.S. product launch. Squeezed by a severe "going concern" qualification in its FY2025 audit, the company is bypassing traditional vertical integration by outsourcing hardware to Shenzhen, China, and high-speed consumable manufacturing to Montrade S.p.A. in Bologna, Italy. Facing an FDA PMTA regulatory bottleneck and zero market share, CQENS’s survival now hinges entirely on sustained equity dilution to battle deeply entrenched monopolies like Philip Morris International (PMI) and British American Tobacco (BAT).

Financial Health & The Intellectual Property Moat

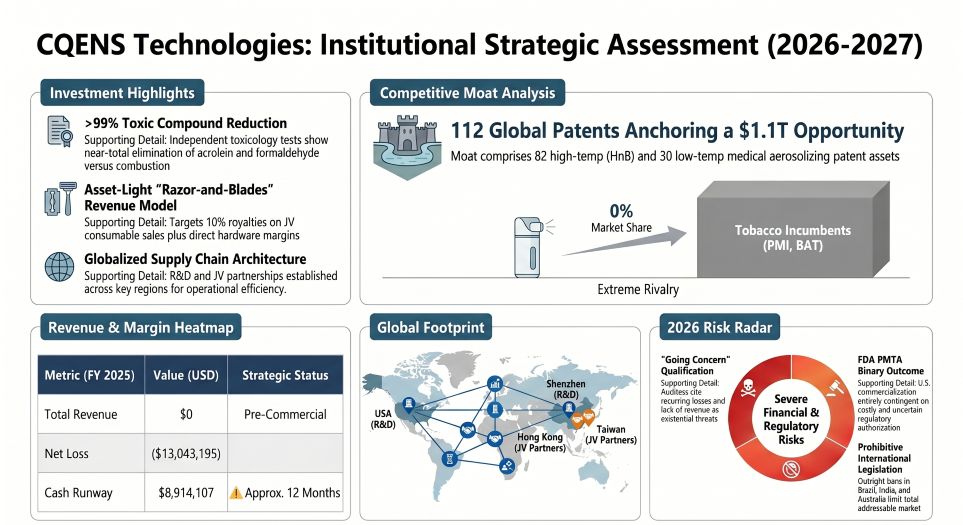

CQENS currently exhibits the forensic financial profile of a highly speculative, cash-starved R&D entity where traditional valuation metrics are mathematically unviable. With FY2025 operating expenses surging 21.8% to $13.31 million and free cash flow plummeting to a negative $6.61 million, the enterprise is surviving via structural equity dilution.

CQENS is masking its operational cash hemorrhage by utilizing its own capitalization table as currency. An aggressive $8.84 million in non-cash charges—predominantly stock options and common stock issued for services—accounted for over 66% of the company's FY2025 operating expenses. While this temporarily preserves the $8.91 million cash balance generated from recent equity raises, it fundamentally degrades the quality of shares held by minority investors.

However, the company’s isolated competitive moat—its intellectual property—continues to harden. A 30.8% year-over-year increase in R&D spending to $1.96 million directly funds the engineering architecture backing 82 high-temperature HnB and 30 low-temperature aerosolizing patents. Independent toxicology protocols showing a >99% harm reduction compared to combustible benchmarks confirm technical viability. Yet, without robust cost-pass-through mechanisms or any active revenue streams, this IP portfolio remains a theoretical asset trapped behind an insurmountable FDA Pre-market Tobacco Authorization (PMTA) wall.

Figure CQENS Technologies Institutional Strategic Assessment (2026-2027)

Supply Chain Pivot: Hyper-Fragmented Dis-Integration

Supply Chain Pivot: Hyper-Fragmented Dis-Integration

While incumbent conglomerates execute accretive acquisitions to consolidate manufacturing, CQENS is pursuing severe supply chain fragmentation to avoid the capital expenditure required for complete vertical integration.

The company is redirecting its limited capital toward strategic offshore nodes. A critical $1.83 million in FY2025 CAPEX was heavily allocated to "Construction in Progress," specifically funding bespoke, high-speed automated consumable machinery engineered by Montrade S.p.A. in Italy. Simultaneously, CQENS expanded its technical human capital by opening an R&D facility in Shenzhen, China (anchored by a fixed 34,373 RMB monthly lease), and consolidating its device component sourcing through CQENS Electronics (Hong Kong) Limited—a 50% joint venture with Asahi Corporation.

This asset-light architecture is designed to yield high-margin royalties (10% top-line from its unfinalized U.S. Firebird Manufacturing JV) post-2027. However, the geographic dispersion exposes CQENS to critical third-party execution bottlenecks. Unlike PMI or BAT, which can internalize supply shocks and absorb cyclical inventory de-stocking, any failure by Montrade to deliver regulatory-grade automation, or by Firebird to meet FDA Good Manufacturing Practice (GMP) standards, will instantly derail CQENS’s commercial timeline.

HDIN Institutional Perspective: The High Cost of Regulatory Monopolies

The corporate trajectory of CQENS acts as a proxy for the structural barriers deliberately engineered into the modern tobacco and nicotine-alternative sectors. The extreme costs associated with the FDA’s PMTA process function as an invisible economic moat protecting legacy incumbents. Philip Morris and British American Tobacco possess the massive operational cash flows required to weaponize compliance, sustaining multi-year regulatory reviews and engaging in aggressive patent litigation that effectively starves undercapitalized challengers.

Furthermore, internal governance structures at CQENS amplify institutional risk. The complete absence of independent directors, the lack of an audit committee, and openly acknowledged "material weaknesses" in financial reporting controls render the stock un-investable for ESG-mandated funds or institutional capital. The lack of standard corporate oversight combined with heavy reliance on related-party transactions (such as zero-interest loans from Xten Capital Group and consulting payouts to Plexus International, both controlled by CQENS executives) suggests that the company operates more as an insider-driven IP incubator than a transparent public entity. Until CQENS secures its PMTA clearance and translates its Shenzhen-engineered prototypes into commercial realities, the firm remains a binary wager on regulatory outcomes rather than a stable hardware manufacturer.

Presentation Download & Video Access

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence firm specializing in forensic financial deconstruction, supply chain pivot tracking, and macroeconomic cycle analysis. For more institutional-grade insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & The Intellectual Property Moat

CQENS currently exhibits the forensic financial profile of a highly speculative, cash-starved R&D entity where traditional valuation metrics are mathematically unviable. With FY2025 operating expenses surging 21.8% to $13.31 million and free cash flow plummeting to a negative $6.61 million, the enterprise is surviving via structural equity dilution.

CQENS is masking its operational cash hemorrhage by utilizing its own capitalization table as currency. An aggressive $8.84 million in non-cash charges—predominantly stock options and common stock issued for services—accounted for over 66% of the company's FY2025 operating expenses. While this temporarily preserves the $8.91 million cash balance generated from recent equity raises, it fundamentally degrades the quality of shares held by minority investors.

However, the company’s isolated competitive moat—its intellectual property—continues to harden. A 30.8% year-over-year increase in R&D spending to $1.96 million directly funds the engineering architecture backing 82 high-temperature HnB and 30 low-temperature aerosolizing patents. Independent toxicology protocols showing a >99% harm reduction compared to combustible benchmarks confirm technical viability. Yet, without robust cost-pass-through mechanisms or any active revenue streams, this IP portfolio remains a theoretical asset trapped behind an insurmountable FDA Pre-market Tobacco Authorization (PMTA) wall.

Figure CQENS Technologies Institutional Strategic Assessment (2026-2027)

Supply Chain Pivot: Hyper-Fragmented Dis-IntegrationWhile incumbent conglomerates execute accretive acquisitions to consolidate manufacturing, CQENS is pursuing severe supply chain fragmentation to avoid the capital expenditure required for complete vertical integration.

The company is redirecting its limited capital toward strategic offshore nodes. A critical $1.83 million in FY2025 CAPEX was heavily allocated to "Construction in Progress," specifically funding bespoke, high-speed automated consumable machinery engineered by Montrade S.p.A. in Italy. Simultaneously, CQENS expanded its technical human capital by opening an R&D facility in Shenzhen, China (anchored by a fixed 34,373 RMB monthly lease), and consolidating its device component sourcing through CQENS Electronics (Hong Kong) Limited—a 50% joint venture with Asahi Corporation.

This asset-light architecture is designed to yield high-margin royalties (10% top-line from its unfinalized U.S. Firebird Manufacturing JV) post-2027. However, the geographic dispersion exposes CQENS to critical third-party execution bottlenecks. Unlike PMI or BAT, which can internalize supply shocks and absorb cyclical inventory de-stocking, any failure by Montrade to deliver regulatory-grade automation, or by Firebird to meet FDA Good Manufacturing Practice (GMP) standards, will instantly derail CQENS’s commercial timeline.

HDIN Institutional Perspective: The High Cost of Regulatory Monopolies

The corporate trajectory of CQENS acts as a proxy for the structural barriers deliberately engineered into the modern tobacco and nicotine-alternative sectors. The extreme costs associated with the FDA’s PMTA process function as an invisible economic moat protecting legacy incumbents. Philip Morris and British American Tobacco possess the massive operational cash flows required to weaponize compliance, sustaining multi-year regulatory reviews and engaging in aggressive patent litigation that effectively starves undercapitalized challengers.

Furthermore, internal governance structures at CQENS amplify institutional risk. The complete absence of independent directors, the lack of an audit committee, and openly acknowledged "material weaknesses" in financial reporting controls render the stock un-investable for ESG-mandated funds or institutional capital. The lack of standard corporate oversight combined with heavy reliance on related-party transactions (such as zero-interest loans from Xten Capital Group and consulting payouts to Plexus International, both controlled by CQENS executives) suggests that the company operates more as an insider-driven IP incubator than a transparent public entity. Until CQENS secures its PMTA clearance and translates its Shenzhen-engineered prototypes into commercial realities, the firm remains a binary wager on regulatory outcomes rather than a stable hardware manufacturer.

Presentation Download & Video Access

* Click the PDF download link under 'Related Topics' to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier strategic market intelligence firm specializing in forensic financial deconstruction, supply chain pivot tracking, and macroeconomic cycle analysis. For more institutional-grade insights, visit www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.