Rain Enhancement Technologies (Nasdaq: RET) Pivots to 'Water-as-a-Service' as Pre-Revenue Burn Drives $13.0M Working Capital Deficit in FY2025 Audit

Date : 2026-04-23

Reading : 76

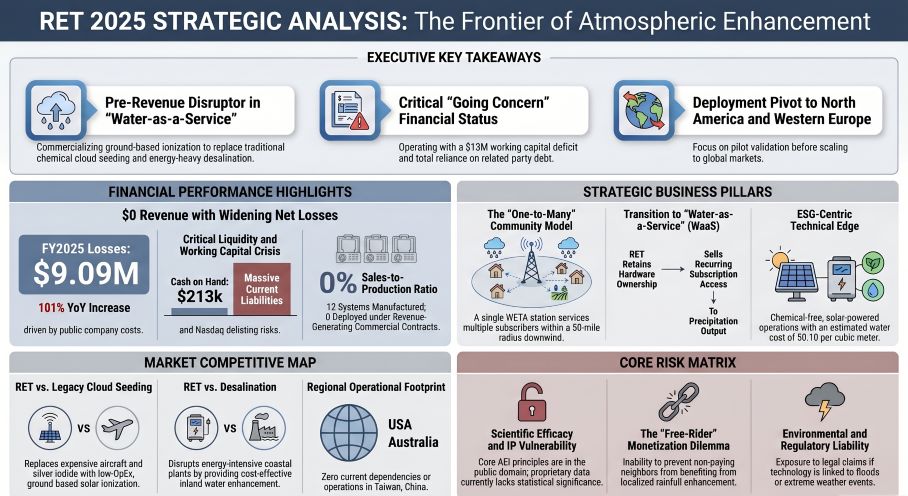

In March 2026, Rain Enhancement Technologies (Nasdaq: RET) filed its FY2025 Annual Report from its Naples, Florida headquarters, revealing $0 in revenue against a widening $9.09 million net loss. Driven by a complete absence of commercial execution, the climate hardware developer is attempting a critical pivot to a 'Water-as-a-Service' model. However, with a $13.0 million working capital deficit and total reliance on high-interest, related-party debt to fund atmospheric pilot deployments in Utah and Australia, RET faces an immediate liquidity crisis that threatens its going-concern status heading into 2027.

Financial Health & Operational Moats: The Capital Structure Chokehold

A fundamental teardown of RET’s FY2025 balance sheet reveals a highly distressed enterprise surviving almost entirely on external related-party life support. While the company deployed $987,805 in capital expenditures to expand its Weather Enhancement Technology Array (WETA) fleet to 12 total units, actual operational cash flow health is critically weak. RET ended the fiscal year with a mere $213,688 in cash, offset by current liabilities of $13.29 million.

Despite operating at a 0% sales-to-production ratio and generating zero commercial contracts, General and Administrative (G&A) expenses spiked to $7.65 million. Astoundingly, absolute Research & Development (R&D) spend was a negligible $62,011. This capital misallocation is exacerbated by an exceptionally cash-heavy executive compensation structure, including a $1.0 million annual cash bonus paid to CEO Randy Seidl in early 2026 and a guaranteed $5.82 million retention bonus trigger.

Furthermore, RET’s capital structure is functionally locked by a floating-rate $10.0 million line of credit from RHY Management, an entity affiliated with Chairman Harry You. A newly instituted board mandate requires that up to 30% of the net proceeds from any future public equity capital raise be explicitly diverted to repay this related-party debt. For prospective investors, this covenant guarantees immediate capital structure dilution and signals that new equity will be systematically siphoned to de-risk insider loans rather than fund proprietary meteorological engineering.

Figure RET 2025 STRATEGIC ANALYSIS The Frontier of Atmospheric Enhancement

Supply Chain Pivot: Australian Sourcing and Inventory Accumulation

Supply Chain Pivot: Australian Sourcing and Inventory Accumulation

RET's physical footprint indicates a heavy reliance on a fragmented, international supply base. Lacking vertical integration, the company is acutely exposed to global commodity volatility, specifically cyclical international pricing for fiberglass and steel inputs. During 2025, RET utilized third-party contract manufacturers in Australia to construct 10 new WETA systems, which were subsequently shipped to the United States.

Rather than adopting a lean manufacturing posture, RET is engaged in aggressive inventory buffering—a sharp divergence from the broader industrial inventory de-stocking trend. Seven completed WETA units currently sit idle in a 4,050-square-foot leased warehouse in Brighton, Colorado, pending future, unconfirmed deployments. Unable to establish immediate cost-pass-through mechanisms due to its pre-commercial status and unproven "One-to-Many" subscription model, RET absorbs all raw material and freight inflation directly. If the company fails to successfully execute its near-shoring initiatives, it risks severe margin compression long before it achieves its targeted $0.10 per cubic meter water-generation cost.

HDIN Institutional Perspective: The "Free-Rider" Dilemma and Technological Obsolescence

RET’s fundamental scientific premise—Atmospheric Enhancement by Ionization (AEI)—presents a highly disruptive ESG narrative. Utilizing ground-based, 3600W off-grid solar arrays that consume just 600 kWh annually, the WETA system theoretically bypasses the downstream environmental contamination risks and extreme aviation logistics of legacy chemical cloud seeding (e.g., silver iodide dispersal).

However, from an institutional perspective, the company’s technological moat is practically non-existent. The core scientific principles of AEI have resided in the public domain since the 1950s. RET's IP portfolio relies primarily on heavily restricted licenses rather than newly minted, proprietary utility patents. Crucially, the company admits it has zero deployed Artificial Intelligence capabilities. Without the immediate pursuit of accretive acquisitions to secure proprietary machine-learning algorithms and predictive radar synchronization, RET’s hardware is highly vulnerable to being leapfrogged by better-capitalized incumbents integrating AI into traditional weather modification networks.

Even if the current non-revenue pilot hubs—specifically the snowpack enhancement trial in the La Sal Range of Grand County, Utah, and the fog mitigation pilot in Australia—yield statistically significant data, RET's "Water-as-a-Service" model faces an unresolved localized monetization paradox. Because the WETA ionization plume covers a 50-mile downwind radius, neighboring agricultural operators and municipalities can capture the precipitation benefits without subscribing. Unless RET can mandate regional legislative compliance or secure massive top-down state contracts, this inherent "free-rider" problem will act as a permanent governor on top-line revenue growth.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is an elite financial intelligence and strategic advisory firm specializing in deep-dive corporate audits, supply chain deconstruction, and macroeconomic risk assessment. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Capital Structure Chokehold

A fundamental teardown of RET’s FY2025 balance sheet reveals a highly distressed enterprise surviving almost entirely on external related-party life support. While the company deployed $987,805 in capital expenditures to expand its Weather Enhancement Technology Array (WETA) fleet to 12 total units, actual operational cash flow health is critically weak. RET ended the fiscal year with a mere $213,688 in cash, offset by current liabilities of $13.29 million.

Despite operating at a 0% sales-to-production ratio and generating zero commercial contracts, General and Administrative (G&A) expenses spiked to $7.65 million. Astoundingly, absolute Research & Development (R&D) spend was a negligible $62,011. This capital misallocation is exacerbated by an exceptionally cash-heavy executive compensation structure, including a $1.0 million annual cash bonus paid to CEO Randy Seidl in early 2026 and a guaranteed $5.82 million retention bonus trigger.

Furthermore, RET’s capital structure is functionally locked by a floating-rate $10.0 million line of credit from RHY Management, an entity affiliated with Chairman Harry You. A newly instituted board mandate requires that up to 30% of the net proceeds from any future public equity capital raise be explicitly diverted to repay this related-party debt. For prospective investors, this covenant guarantees immediate capital structure dilution and signals that new equity will be systematically siphoned to de-risk insider loans rather than fund proprietary meteorological engineering.

Figure RET 2025 STRATEGIC ANALYSIS The Frontier of Atmospheric Enhancement

Supply Chain Pivot: Australian Sourcing and Inventory AccumulationRET's physical footprint indicates a heavy reliance on a fragmented, international supply base. Lacking vertical integration, the company is acutely exposed to global commodity volatility, specifically cyclical international pricing for fiberglass and steel inputs. During 2025, RET utilized third-party contract manufacturers in Australia to construct 10 new WETA systems, which were subsequently shipped to the United States.

Rather than adopting a lean manufacturing posture, RET is engaged in aggressive inventory buffering—a sharp divergence from the broader industrial inventory de-stocking trend. Seven completed WETA units currently sit idle in a 4,050-square-foot leased warehouse in Brighton, Colorado, pending future, unconfirmed deployments. Unable to establish immediate cost-pass-through mechanisms due to its pre-commercial status and unproven "One-to-Many" subscription model, RET absorbs all raw material and freight inflation directly. If the company fails to successfully execute its near-shoring initiatives, it risks severe margin compression long before it achieves its targeted $0.10 per cubic meter water-generation cost.

HDIN Institutional Perspective: The "Free-Rider" Dilemma and Technological Obsolescence

RET’s fundamental scientific premise—Atmospheric Enhancement by Ionization (AEI)—presents a highly disruptive ESG narrative. Utilizing ground-based, 3600W off-grid solar arrays that consume just 600 kWh annually, the WETA system theoretically bypasses the downstream environmental contamination risks and extreme aviation logistics of legacy chemical cloud seeding (e.g., silver iodide dispersal).

However, from an institutional perspective, the company’s technological moat is practically non-existent. The core scientific principles of AEI have resided in the public domain since the 1950s. RET's IP portfolio relies primarily on heavily restricted licenses rather than newly minted, proprietary utility patents. Crucially, the company admits it has zero deployed Artificial Intelligence capabilities. Without the immediate pursuit of accretive acquisitions to secure proprietary machine-learning algorithms and predictive radar synchronization, RET’s hardware is highly vulnerable to being leapfrogged by better-capitalized incumbents integrating AI into traditional weather modification networks.

Even if the current non-revenue pilot hubs—specifically the snowpack enhancement trial in the La Sal Range of Grand County, Utah, and the fog mitigation pilot in Australia—yield statistically significant data, RET's "Water-as-a-Service" model faces an unresolved localized monetization paradox. Because the WETA ionization plume covers a 50-mile downwind radius, neighboring agricultural operators and municipalities can capture the precipitation benefits without subscribing. Unless RET can mandate regional legislative compliance or secure massive top-down state contracts, this inherent "free-rider" problem will act as a permanent governor on top-line revenue growth.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is an elite financial intelligence and strategic advisory firm specializing in deep-dive corporate audits, supply chain deconstruction, and macroeconomic risk assessment. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.