AI-Biotech Platform XtalPi (HKEX: 2228) Disrupts Legacy CRO Economics with Autonomous R&D as FY2025 Revenue Surges 201.2%

Date : 2026-04-21

Reading : 86

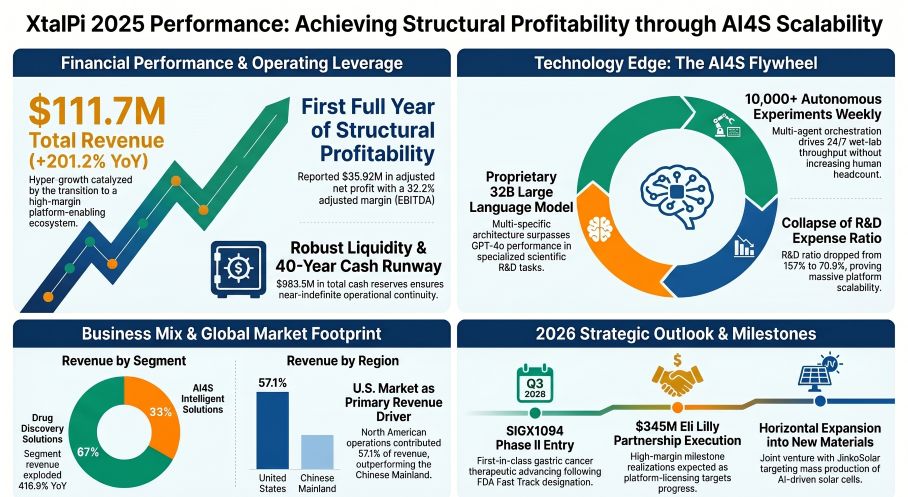

In its FY2025 audit, Shenzhen-based AI-biopharma platform XtalPi (HKEX: 2228) posted its first full-year adjusted net profit of $35.92 million, driven by a 201.2% top-line surge to $111.67 million. Capitalizing on a strategic pivot from manual project services to a highly automated "platform licensing" model, the company generated 57.1% of its revenue from the United States. By replacing traditional bench chemists with a proprietary 32B Large Language Model and robotic wet-lab infrastructure, XtalPi effectively decouples drug discovery throughput from human labor constraints, establishing a new commercial paradigm for high-margin, scalable R&D.

Financial Health & Operational Moats: The Death of Linear Scaling

XtalPi’s 2025 financial disclosures reveal a structural dismantling of the legacy Contract Research Organization (CRO) economic model. While traditional service providers rely on headcount expansion to drive revenue, XtalPi utilized a remarkably light capital expenditure (CapEx) of just $10.35 million to support a $74.60 million absolute increase in top-line revenue. This ultra-high asset turnover is the direct result of its "AI + Robotics + Multi-Agent" flywheel, which autonomously executes over 10,000 compound synthesis experiments weekly.

Because total revenue outpaced fulfillment costs, gross margins expanded dramatically to 69.7% (up from 46.3% in 2024). More critically, while absolute R&D spend increased to $79.19 million, R&D as a percentage of revenue collapsed from 157.0% to 70.9%. The company has engineered a closed-loop system where its domain-specific 32B LLM directs robotic arrays, minimizing reagent waste and effectively neutralizing the manual variance that plagues traditional labs. This leverage catalyzed their $345 million multi-target licensing agreement with Eli Lilly, transitioning XtalPi’s revenue from discrete consulting fees to robust, milestone-driven cost-pass-through mechanisms that shield the balance sheet from inflationary pressures.

Figure XtalPi 2025 Performance Achieving Structural Profitability through Al4S Scalability

Supply Chain Pivot: Transatlantic Arbitrage and Wet-Lab Decentralization

Supply Chain Pivot: Transatlantic Arbitrage and Wet-Lab Decentralization

An analysis of XtalPi’s geographical billing exposes a deliberate regional realignment. Despite operating highly cost-efficient wet labs (exceeding 10,000 square meters) in Shenzhen, Shanghai, and Beijing—where it utilizes a 15% High and New Technology Enterprise (HNTE) tax rate—57.1% ($63.76 million) of its 2025 revenue was extracted from the US market.

To insulate its intellectual property and establish proximity to key Western biopharma clients, XtalPi is executing a strict vertical integration of its international supply chain. The Boston operational base serves as the primary anchor for North American client acquisition, navigating higher state and federal tax burdens to secure premium contracts. Concurrently, the company established a European automated R&D hub via the $34.78 million buyout of UK-based LCC Technologies. This move stands as a textbook example of accretive acquisitions, directly embedding LCC’s automated chiral chemistry capabilities into XtalPi’s broader AI4S (AI for Science) ecosystem without requiring years of foundational organic development.

HDIN Institutional Perspective: A Trough for CDMOs, A Premium for AI4S

The broader life sciences manufacturing sector is currently navigating a cyclical trough. Legacy CROs and CDMOs are grappling with severe margin compression and prolonged inventory de-stocking driven by post-pandemic capacity gluts and a tightening biotech funding environment. XtalPi’s FY2025 turnaround signals a profound market bifurcation: capital is fleeing labor-heavy bench operations and rotating aggressively toward deterministic, high-throughput automated platforms.

XtalPi’s aggressive accumulation of $7.60 million in forward-looking contract liabilities (a 223% YoY jump) indicates that global giants like BASF, Roche, and JW Pharmaceutical are willing to pay significant upfront premiums for AI-generated pipeline certainty. Furthermore, armed with $983.46 million in cash reserves and a subsequent $367.64 million convertible bond issuance in early 2026, XtalPi possesses an near-indefinite runway. We view this liquidity not just as a defensive buffer, but as an offensive war chest to scale its technology into non-biological adjacencies—most notably evidenced by its joint venture with JinkoSolar to automate perovskite tandem solar cell mass production by 2028. XtalPi is no longer merely a biotech service provider; it is mutating into the foundational operating system for global material and life sciences.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence and strategic corporate analysis, serving global asset managers and executive boards. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Death of Linear Scaling

XtalPi’s 2025 financial disclosures reveal a structural dismantling of the legacy Contract Research Organization (CRO) economic model. While traditional service providers rely on headcount expansion to drive revenue, XtalPi utilized a remarkably light capital expenditure (CapEx) of just $10.35 million to support a $74.60 million absolute increase in top-line revenue. This ultra-high asset turnover is the direct result of its "AI + Robotics + Multi-Agent" flywheel, which autonomously executes over 10,000 compound synthesis experiments weekly.

Because total revenue outpaced fulfillment costs, gross margins expanded dramatically to 69.7% (up from 46.3% in 2024). More critically, while absolute R&D spend increased to $79.19 million, R&D as a percentage of revenue collapsed from 157.0% to 70.9%. The company has engineered a closed-loop system where its domain-specific 32B LLM directs robotic arrays, minimizing reagent waste and effectively neutralizing the manual variance that plagues traditional labs. This leverage catalyzed their $345 million multi-target licensing agreement with Eli Lilly, transitioning XtalPi’s revenue from discrete consulting fees to robust, milestone-driven cost-pass-through mechanisms that shield the balance sheet from inflationary pressures.

Figure XtalPi 2025 Performance Achieving Structural Profitability through Al4S Scalability

Supply Chain Pivot: Transatlantic Arbitrage and Wet-Lab Decentralization An analysis of XtalPi’s geographical billing exposes a deliberate regional realignment. Despite operating highly cost-efficient wet labs (exceeding 10,000 square meters) in Shenzhen, Shanghai, and Beijing—where it utilizes a 15% High and New Technology Enterprise (HNTE) tax rate—57.1% ($63.76 million) of its 2025 revenue was extracted from the US market.

To insulate its intellectual property and establish proximity to key Western biopharma clients, XtalPi is executing a strict vertical integration of its international supply chain. The Boston operational base serves as the primary anchor for North American client acquisition, navigating higher state and federal tax burdens to secure premium contracts. Concurrently, the company established a European automated R&D hub via the $34.78 million buyout of UK-based LCC Technologies. This move stands as a textbook example of accretive acquisitions, directly embedding LCC’s automated chiral chemistry capabilities into XtalPi’s broader AI4S (AI for Science) ecosystem without requiring years of foundational organic development.

HDIN Institutional Perspective: A Trough for CDMOs, A Premium for AI4S

The broader life sciences manufacturing sector is currently navigating a cyclical trough. Legacy CROs and CDMOs are grappling with severe margin compression and prolonged inventory de-stocking driven by post-pandemic capacity gluts and a tightening biotech funding environment. XtalPi’s FY2025 turnaround signals a profound market bifurcation: capital is fleeing labor-heavy bench operations and rotating aggressively toward deterministic, high-throughput automated platforms.

XtalPi’s aggressive accumulation of $7.60 million in forward-looking contract liabilities (a 223% YoY jump) indicates that global giants like BASF, Roche, and JW Pharmaceutical are willing to pay significant upfront premiums for AI-generated pipeline certainty. Furthermore, armed with $983.46 million in cash reserves and a subsequent $367.64 million convertible bond issuance in early 2026, XtalPi possesses an near-indefinite runway. We view this liquidity not just as a defensive buffer, but as an offensive war chest to scale its technology into non-biological adjacencies—most notably evidenced by its joint venture with JinkoSolar to automate perovskite tandem solar cell mass production by 2028. XtalPi is no longer merely a biotech service provider; it is mutating into the foundational operating system for global material and life sciences.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence and strategic corporate analysis, serving global asset managers and executive boards. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.