Zhipu AI Consolidates Autonomous Agent Dominance as Cloud Revenue Surges 292.6% in FY2025 Audit

Date : 2026-04-21

Reading : 121

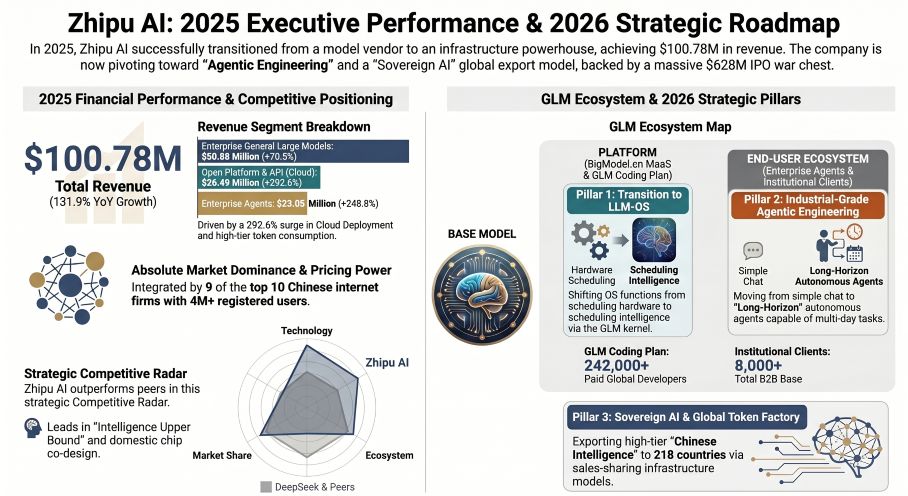

Following its January 2026 Hong Kong IPO, Beijing-based Zhipu AI reported a 131.9% top-line explosion to $100.78 million in its FY2025 audit. Driven by intense enterprise adoption of its GLM-5 architecture for complex "Agentic Engineering," the company successfully monetized its transition from a raw model vendor to a Large Language Model Operating System (LLM-OS). To circumvent systemic geopolitical semiconductor bottlenecks, management executed a radical 83.8% CapEx reduction, pivoting toward an OpEx computing procurement model while aggressively deploying domestic hardware-software co-design to sustain its global rollout across 218 regional markets.

Financial Health & Operational Moats: The Margin Compression Paradox

Zhipu AI’s FY2025 P&L reflects the classic structural deficit of a frontier AI infrastructure player aggressively seizing market share. While total revenue scaled exponentially to $100.78 million, corporate gross margins compressed from 56.3% to 41.0%. This margin compression is not indicative of deteriorating pricing power—rather, it is a deliberate absorption of heavy delivery resource costs required for high-touch, localized enterprise deployments ($74.29 million revenue contribution).

The underlying metric of operational strength lies in the company's absolute pricing power. Zhipu implemented severe cost-pass-through mechanisms, hiking API call pricing by 83% and removing enterprise discounts on its GLM Coding Plan (which holds 242,000 paid developers), triggering a "volume and price both rising" trajectory. This inelastic demand underscores a deep ecosystem moat. Concurrently, economies of scale in the Open Platform segment pushed cloud deployment gross margins from 3.3% to 18.9%. Furthermore, R&D intensity dropped from 702.7% to a more sustainable 439.1% ($442.50 million), signaling that top-line commercialization is finally beginning to outpace algorithmic burn rates.

Figure Zhipu Al 2025 Executive Performance & 2026 Strategic Roadmap

Supply Chain Pivot: CapEx Realignment and Domestic "Co-Design"

Supply Chain Pivot: CapEx Realignment and Domestic "Co-Design"

Faced with a domestic "compute panic" and restricted global supply chains for high-end GPUs, Zhipu AI orchestrated a profound capital strategy pivot. Capital Expenditures (CapEx) plummeted by 83.8%, dropping from $64.32 million to merely $10.39 million. Instead of absorbing depreciation via hardware capitalization, the firm shifted entirely to an OpEx model, procuring elastic computing services from third-party clusters.

To hedge against external silicon dependency, Zhipu accelerated deep kernel-level integration with domestic Chinese chips. By engineering proprietary fusion technologies—specifically the "Lightning Indexer" and "FlashComm" protocols—the company achieved zero-day adaptation. Combined with the algorithmic pruning of the Slime framework, Muon Split optimization, and MLA-256 improvements, Zhipu effectively reduced its KVCache footprint and halved deployment costs. This hardware-software co-design transforms a supply chain vulnerability into a sovereign infrastructure advantage, forming the backbone of its "Token Going Global" export strategy.

HDIN Institutional Perspective: The "Neutrality Premium" and LLM-OS Cycle

From an institutional standpoint, Zhipu AI's FY2025 disclosures dismantle the prevalent bear thesis that domestic AI foundation models are merely captive R&D subsidiaries for tech giants. Despite having Meituan and Ant Group on its capitalization table, Zhipu's Related Party Transactions (RPTs) reveal extreme operational independence. Direct RPT revenue accounted for only ~4.5% ($4.58 million) of total sales, and related-party computing procurement was a negligible $1.05 million. Zhipu is not subject to vendor lock-in with Alibaba Cloud or Tencent Cloud. This strict neutrality warrants a significant market valuation premium, allowing Zhipu to position itself as the foundational, agnostic LLM-OS layer for Fortune 500 enterprises and government entities requiring absolute data sovereignty.

Looking forward, the successful $628.05 million capital injection from its January 2026 Hong Kong public offering structurally derisks the balance sheet. With an estimated liquidity buffer of $942 million and an operating cash burn stabilizing near $312.5 million annually, Zhipu AI possesses a definitive ~3.0-year runway. This capital moat allows the firm to weather the current semiconductor capacity constraints and cement its status as an indispensable autonomous agent utility before the next cyclical trough in legacy software procurement.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm delivering institutional-grade analysis on frontier technologies, capital markets, and geopolitical supply chain shifts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Margin Compression Paradox

Zhipu AI’s FY2025 P&L reflects the classic structural deficit of a frontier AI infrastructure player aggressively seizing market share. While total revenue scaled exponentially to $100.78 million, corporate gross margins compressed from 56.3% to 41.0%. This margin compression is not indicative of deteriorating pricing power—rather, it is a deliberate absorption of heavy delivery resource costs required for high-touch, localized enterprise deployments ($74.29 million revenue contribution).

The underlying metric of operational strength lies in the company's absolute pricing power. Zhipu implemented severe cost-pass-through mechanisms, hiking API call pricing by 83% and removing enterprise discounts on its GLM Coding Plan (which holds 242,000 paid developers), triggering a "volume and price both rising" trajectory. This inelastic demand underscores a deep ecosystem moat. Concurrently, economies of scale in the Open Platform segment pushed cloud deployment gross margins from 3.3% to 18.9%. Furthermore, R&D intensity dropped from 702.7% to a more sustainable 439.1% ($442.50 million), signaling that top-line commercialization is finally beginning to outpace algorithmic burn rates.

Figure Zhipu Al 2025 Executive Performance & 2026 Strategic Roadmap

Supply Chain Pivot: CapEx Realignment and Domestic "Co-Design"Faced with a domestic "compute panic" and restricted global supply chains for high-end GPUs, Zhipu AI orchestrated a profound capital strategy pivot. Capital Expenditures (CapEx) plummeted by 83.8%, dropping from $64.32 million to merely $10.39 million. Instead of absorbing depreciation via hardware capitalization, the firm shifted entirely to an OpEx model, procuring elastic computing services from third-party clusters.

To hedge against external silicon dependency, Zhipu accelerated deep kernel-level integration with domestic Chinese chips. By engineering proprietary fusion technologies—specifically the "Lightning Indexer" and "FlashComm" protocols—the company achieved zero-day adaptation. Combined with the algorithmic pruning of the Slime framework, Muon Split optimization, and MLA-256 improvements, Zhipu effectively reduced its KVCache footprint and halved deployment costs. This hardware-software co-design transforms a supply chain vulnerability into a sovereign infrastructure advantage, forming the backbone of its "Token Going Global" export strategy.

HDIN Institutional Perspective: The "Neutrality Premium" and LLM-OS Cycle

From an institutional standpoint, Zhipu AI's FY2025 disclosures dismantle the prevalent bear thesis that domestic AI foundation models are merely captive R&D subsidiaries for tech giants. Despite having Meituan and Ant Group on its capitalization table, Zhipu's Related Party Transactions (RPTs) reveal extreme operational independence. Direct RPT revenue accounted for only ~4.5% ($4.58 million) of total sales, and related-party computing procurement was a negligible $1.05 million. Zhipu is not subject to vendor lock-in with Alibaba Cloud or Tencent Cloud. This strict neutrality warrants a significant market valuation premium, allowing Zhipu to position itself as the foundational, agnostic LLM-OS layer for Fortune 500 enterprises and government entities requiring absolute data sovereignty.

Looking forward, the successful $628.05 million capital injection from its January 2026 Hong Kong public offering structurally derisks the balance sheet. With an estimated liquidity buffer of $942 million and an operating cash burn stabilizing near $312.5 million annually, Zhipu AI possesses a definitive ~3.0-year runway. This capital moat allows the firm to weather the current semiconductor capacity constraints and cement its status as an indispensable autonomous agent utility before the next cyclical trough in legacy software procurement.

Presentation Download & Video Access

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier market intelligence and strategic advisory firm delivering institutional-grade analysis on frontier technologies, capital markets, and geopolitical supply chain shifts. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.