Cloud AI Infrastructure Enters Domestic Substitution Cycle: Enflame Technology Targets $834M IPO CAPEX to Bypass CUDA Monopoly Amid Tightening Supply Chains

Date : 2026-04-21

Reading : 445

Enflame Technology is seeking an $834.78 million initial public offering on the domestic exchange in early 2026 to aggressively scale its AI inference clusters and counter geopolitical semiconductor constraints. For the fiscal year 2025, the Shanghai-based Fabless designer leveraged a deep strategic alliance with Tencent to post $137.76 million in revenue. However, beneath the 81.3% three-year compound growth rate lies a highly concentrated operating model. Enflame is now executing a massive supply chain pivot, utilizing localized advanced packaging and its proprietary TopsRider software stack to capture China’s exploding data center demand.

Financial Health & Operational Moats: The Cost of Ecosystem Lock-In

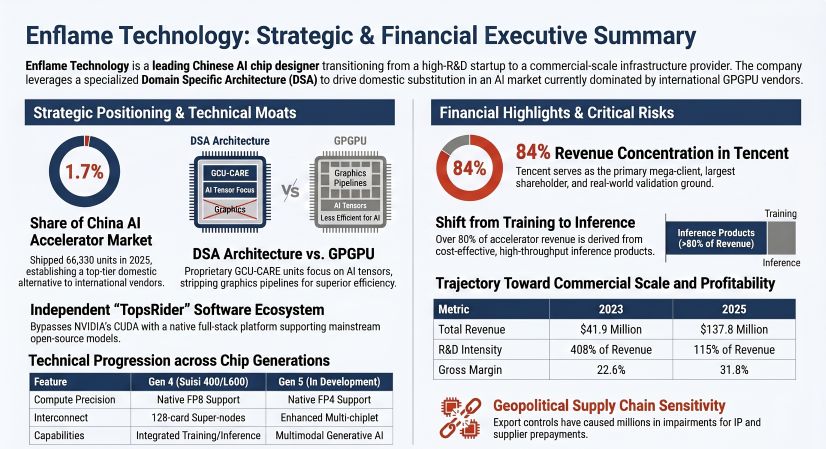

Enflame’s transition from a capital-intensive R&D outfit to a commercial-scale AI infrastructure provider is yielding structurally improving unit economics, though severe underlying working capital risks remain. Gross margins expanded to 31.78% in 2025, driven by the rollout of the 3rd-generation and 4th-generation (Suisi 400) AI accelerators. By utilizing a Domain Specific Architecture (DSA) rather than a generalized GPGPU model, Enflame strips out redundant graphics rendering pipelines, delivering superior performance-per-watt for dedicated tensor calculations.

However, this growth is accompanied by targeted margin compression engineered by its largest backer. Tencent Tech (Shenzhen) accounted for an overwhelming 74.90% of Enflame's direct accelerator sales ($106.87 million) in 2025. This mega-client concentration stripped Enflame of absolute pricing power, forcing a 6.5% contraction in the Average Selling Price (ASP) of its primary AI modules to $1,836.26 due to volume discounts. Unlike peers who might utilize accretive acquisitions to diversify revenue, Enflame's reliance on Tencent’s captive ecosystem operates as both its ultimate commercialization engine and its primary structural vulnerability.

More concerning for institutional investors is the drastic deterioration in Accounts Receivable (AR) quality. While aggregate inventory turnover slowed to 0.66 as the company aggressively hoarded $149.46 million in wafers to prevent inventory de-stocking shocks, the AR aging structure collapsed. In 2025, 80.28% of Enflame's total AR balance shifted into the 1-to-2-year aging bucket, driving bad debt provisions up to 24.76%. This signals that while revenue for "Intelligent Computing Clusters" (like the $20.19 million booked from Chengdu Gaoxin Electronics) is recognized aggressively upon project acceptance, actual cash collection from regional operators is heavily delayed. With an annual operating cash burn of roughly $134 million, the proposed IPO is not merely a growth vehicle—it is a strict liquidity prerequisite.

Figure Enflame Technology Strategic & Financial Executive Summary

Supply Chain Pivot: Engineering "First-Time Right" Localization

Supply Chain Pivot: Engineering "First-Time Right" Localization

Operating under a purely Fabless model, Enflame is acutely exposed to the geopolitical realities of the global semiconductor trade. The 2025 prospectus quantifies this vulnerability: the company was forced to book millions in impairment losses on intellectual property (IP) and supplier prepayments directly due to international trade frictions severing access to specific EDA tools and fabrication nodes.

To establish supply chain resilience, Enflame is abandoning legacy international dependencies in favor of aggressive vertical integration within the domestic ecosystem. The company's 4th-generation L600 training-inference integrated module operating at a 700W TDP, now utilizes fully domestic advanced packaging (Chiplet) solutions.

Furthermore, the planned $834.78 million IPO CAPEX allocation is highly targeted. It directs $209.18 million toward a 5th-generation chip (focusing on native FP4 precision) and $459.13 million toward building 10,000-card (Scale-out) training and inference clusters. Rather than building physical foundries, this capital will act as massive prepayments to secure heavily constrained domestic wafer and High Bandwidth Memory (HBM) capacities. By bypassing Nvidia's NVLink in favor of its proprietary GCU-LARE interconnect and RoCE network protocols (powering its ESL32/64 super-nodes), Enflame is insulating its hardware architecture from future export controls.

HDIN Institutional Perspective: The Asymmetric AIGC Strategy

From a macroeconomic standpoint, Enflame is not attempting to build a 1:1 clone of Nvidia's H100 to compete in generalized LLM training. Instead, HDIN Research views Enflame’s product roadmap as an asymmetric strategy designed to capture the impending inflection point where AI inference demand overtakes training.

By engineering the Suisi 400 and L600 to natively support FP8 mixed-precision computing, Enflame captures the most lucrative segment of edge and cloud inference deployment. Crucially, the company bypassed the trap of building a CUDA-compatible translation layer. By forcing adherence to its proprietary TopsRider full-stack platform—optimized specifically for open-source models like DeepSeek and Qwen—Enflame is constructing a high-switching-cost moat.

Yet, Enflame's path to its projected 2026 profitability relies heavily on state-sponsored macroeconomic tailwinds. The company currently benefits from a 15% preferential tax rate, massive R&D super-deductions, and direct government subsidies. If domestic policymakers tighten these fiscal incentives, Enflame currently lacks the cost-pass-through mechanisms required to force price increases onto mega-clients like Tencent. Ultimately, Enflame's transition from a 1.7% market share challenger to a sovereign AI infrastructure leader hinges on whether its localized supply chain can achieve advanced node parity before its institutional liquidity runway evaporates.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, specializing in deep-dive fundamental analysis of global semiconductor supply chains, geopolitical macroeconomic policy, and advanced computing infrastructure.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of Ecosystem Lock-In

Enflame’s transition from a capital-intensive R&D outfit to a commercial-scale AI infrastructure provider is yielding structurally improving unit economics, though severe underlying working capital risks remain. Gross margins expanded to 31.78% in 2025, driven by the rollout of the 3rd-generation and 4th-generation (Suisi 400) AI accelerators. By utilizing a Domain Specific Architecture (DSA) rather than a generalized GPGPU model, Enflame strips out redundant graphics rendering pipelines, delivering superior performance-per-watt for dedicated tensor calculations.

However, this growth is accompanied by targeted margin compression engineered by its largest backer. Tencent Tech (Shenzhen) accounted for an overwhelming 74.90% of Enflame's direct accelerator sales ($106.87 million) in 2025. This mega-client concentration stripped Enflame of absolute pricing power, forcing a 6.5% contraction in the Average Selling Price (ASP) of its primary AI modules to $1,836.26 due to volume discounts. Unlike peers who might utilize accretive acquisitions to diversify revenue, Enflame's reliance on Tencent’s captive ecosystem operates as both its ultimate commercialization engine and its primary structural vulnerability.

More concerning for institutional investors is the drastic deterioration in Accounts Receivable (AR) quality. While aggregate inventory turnover slowed to 0.66 as the company aggressively hoarded $149.46 million in wafers to prevent inventory de-stocking shocks, the AR aging structure collapsed. In 2025, 80.28% of Enflame's total AR balance shifted into the 1-to-2-year aging bucket, driving bad debt provisions up to 24.76%. This signals that while revenue for "Intelligent Computing Clusters" (like the $20.19 million booked from Chengdu Gaoxin Electronics) is recognized aggressively upon project acceptance, actual cash collection from regional operators is heavily delayed. With an annual operating cash burn of roughly $134 million, the proposed IPO is not merely a growth vehicle—it is a strict liquidity prerequisite.

Figure Enflame Technology Strategic & Financial Executive Summary

Supply Chain Pivot: Engineering "First-Time Right" LocalizationOperating under a purely Fabless model, Enflame is acutely exposed to the geopolitical realities of the global semiconductor trade. The 2025 prospectus quantifies this vulnerability: the company was forced to book millions in impairment losses on intellectual property (IP) and supplier prepayments directly due to international trade frictions severing access to specific EDA tools and fabrication nodes.

To establish supply chain resilience, Enflame is abandoning legacy international dependencies in favor of aggressive vertical integration within the domestic ecosystem. The company's 4th-generation L600 training-inference integrated module operating at a 700W TDP, now utilizes fully domestic advanced packaging (Chiplet) solutions.

Furthermore, the planned $834.78 million IPO CAPEX allocation is highly targeted. It directs $209.18 million toward a 5th-generation chip (focusing on native FP4 precision) and $459.13 million toward building 10,000-card (Scale-out) training and inference clusters. Rather than building physical foundries, this capital will act as massive prepayments to secure heavily constrained domestic wafer and High Bandwidth Memory (HBM) capacities. By bypassing Nvidia's NVLink in favor of its proprietary GCU-LARE interconnect and RoCE network protocols (powering its ESL32/64 super-nodes), Enflame is insulating its hardware architecture from future export controls.

HDIN Institutional Perspective: The Asymmetric AIGC Strategy

From a macroeconomic standpoint, Enflame is not attempting to build a 1:1 clone of Nvidia's H100 to compete in generalized LLM training. Instead, HDIN Research views Enflame’s product roadmap as an asymmetric strategy designed to capture the impending inflection point where AI inference demand overtakes training.

By engineering the Suisi 400 and L600 to natively support FP8 mixed-precision computing, Enflame captures the most lucrative segment of edge and cloud inference deployment. Crucially, the company bypassed the trap of building a CUDA-compatible translation layer. By forcing adherence to its proprietary TopsRider full-stack platform—optimized specifically for open-source models like DeepSeek and Qwen—Enflame is constructing a high-switching-cost moat.

Yet, Enflame's path to its projected 2026 profitability relies heavily on state-sponsored macroeconomic tailwinds. The company currently benefits from a 15% preferential tax rate, massive R&D super-deductions, and direct government subsidies. If domestic policymakers tighten these fiscal incentives, Enflame currently lacks the cost-pass-through mechanisms required to force price increases onto mega-clients like Tencent. Ultimately, Enflame's transition from a 1.7% market share challenger to a sovereign AI infrastructure leader hinges on whether its localized supply chain can achieve advanced node parity before its institutional liquidity runway evaporates.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier provider of institutional market intelligence, specializing in deep-dive fundamental analysis of global semiconductor supply chains, geopolitical macroeconomic policy, and advanced computing infrastructure.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*