Small-Scale GTL Market Hits Commercialization Trough: Greenway Technologies Signals Solvency Crisis with $14M Working Capital Deficit

Date : 2026-04-24

Reading : 80

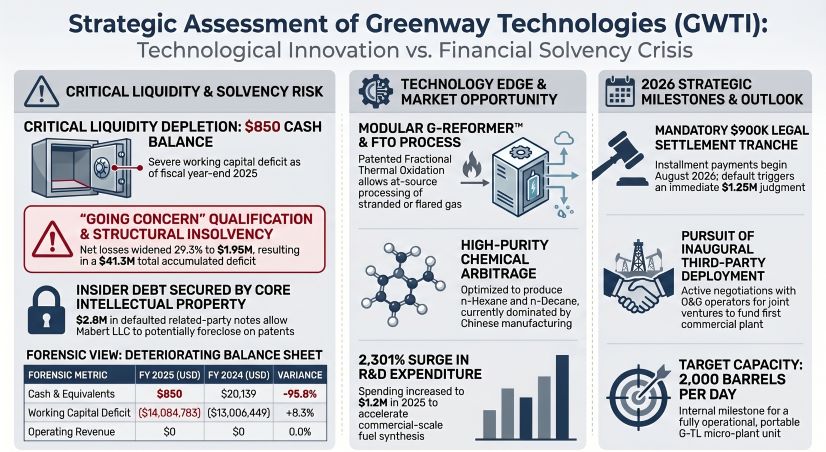

Greenway Technologies, Inc. (OTC: GWTI) faces an existential liquidity crisis entering 2026, ending the fiscal year with a depleted cash position of merely $850 at its Arlington, Texas headquarters. Despite a 2,300% year-over-year surge in R&D expenditures at the Conrad Greer Laboratory (UTA), the pre-revenue company failed to commercialize its proprietary G-Reformer™ micro-plants. Trapped by a $14.08 million working capital deficit and lacking viable operational revenue, GWTI’s core intellectual property is now critically vulnerable to foreclosure by insider-controlled debt entities amid a stalling small-scale gas-to-liquids (GTL) deployment cycle.

Financial Health & Operational Moats: The "Asset-Light" Illusion and Toxic Leverage

Greenway’s FY2025 financial disclosures reveal a structural insolvency loop rather than a functional business model. The company recorded $0 in capital expenditures (CAPEX) alongside $0 in revenues for the second consecutive year. Instead, management executed a massive, highly dilutive pivot toward intangible asset formation, expensing $1.2 million in R&D (a 2,301.67% YoY increase) strictly under ASC 730-10 accounting standards.

This aggressive R&D capitalization without operational cost-pass-through mechanisms has driven the accumulated deficit to $41.33 million. While management secured a one-time liquidity lifeline via a $1.7 million forfeited deposit from a failed 2025 customer deployment, this "income illusion" masks a terminal fundamental flaw: the company’s capital structure is overwhelmingly encumbered by insider debt.

The structural moat—six U.S. patents detailing its Fractional Thermal Oxidation™ (FTO) process—is actively weaponized against common equity holders. Mabert LLC, an entity controlled by Executive Vice President Robert K. Jones, holds $2.05 million in heavily concentrated debt (yielding 10% to 18%). Crucially, these notes are in default and secured by a UCC-1 filing against GWTI's core patents. With the company's valuation deeply distressed, GWTI remains entirely untouchable for accretive acquisitions by midstream energy players; any prospective buyer would immediately trigger poison-pill debt covenants held by the C-suite.

Figure Strategic Assessment of Greenway Technologies (GWTl)

Supply Chain Pivot: The Single-Node Bottleneck

Supply Chain Pivot: The Single-Node Bottleneck

GWTI’s operational strategy relies on the modularity of its 2,000-barrel-per-day G-Reformer units, explicitly designed to bypass the massive footprint of legacy Steam Methane Reformation (SMR) facilities. However, the company has entirely ignored vertical integration, outsourcing 100% of its base refractory equipment manufacturing to a single, unnamed heavy equipment fabricator in Texas.

This hyper-localized supply chain poses a binary execution risk. The 2025 Annual Report explicitly acknowledges that replicating this bespoke manufacturing capability would cause indefinite delays. While the company aggressively pitches its synthesized high-value output (e.g., n-Hexane, n-Decane) as a geopolitical hedge against Chinese chemical supply chain dominance, its input reality is deeply fragile. GWTI holds zero long-term purchase obligations with this sole fabricator, leaving the company heavily exposed to regional cost inflation and manufacturer deprioritization.

HDIN Institutional Perspective: Arbitrage Sensitivity and Sector Cyclicality

From a macroeconomic vantage point, GWTI is attempting to disrupt the wellhead gas monetization sector at a highly precarious moment. The broader petrochemical industry is currently undergoing massive inventory de-stocking, forcing macro-refineries to grapple with acute margin compression.

GWTI’s theoretical economic viability is entirely anchored to the arbitrage spread between stranded natural gas input costs and crude oil output prices. Management’s own models require WTI/Brent crude to hover between $30 and $60 per barrel to maintain competitive profitability against traditional refining. Should commodity volatility narrow this spread, the adoption incentive for third-party operators vaporizes. Furthermore, GWTI faces an impending legal liquidity cliff—a mandatory $900,000 settlement payout beginning August 2026. Without immediate, highly dilutive equity financing (evidenced by the 9.97 million restricted shares already issued in Q1 2026), GWTI is positioned not as a disruptive tech pioneer, but as a cautionary tale of outsourced R&D collapsing under the weight of related-party leverage.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier institutional market intelligence firm specializing in forensic financial analysis, supply chain vulnerabilities, and geopolitical macroeconomic benchmarking. We transform opaque regulatory disclosures into actionable strategic alpha for global institutional investors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The "Asset-Light" Illusion and Toxic Leverage

Greenway’s FY2025 financial disclosures reveal a structural insolvency loop rather than a functional business model. The company recorded $0 in capital expenditures (CAPEX) alongside $0 in revenues for the second consecutive year. Instead, management executed a massive, highly dilutive pivot toward intangible asset formation, expensing $1.2 million in R&D (a 2,301.67% YoY increase) strictly under ASC 730-10 accounting standards.

This aggressive R&D capitalization without operational cost-pass-through mechanisms has driven the accumulated deficit to $41.33 million. While management secured a one-time liquidity lifeline via a $1.7 million forfeited deposit from a failed 2025 customer deployment, this "income illusion" masks a terminal fundamental flaw: the company’s capital structure is overwhelmingly encumbered by insider debt.

The structural moat—six U.S. patents detailing its Fractional Thermal Oxidation™ (FTO) process—is actively weaponized against common equity holders. Mabert LLC, an entity controlled by Executive Vice President Robert K. Jones, holds $2.05 million in heavily concentrated debt (yielding 10% to 18%). Crucially, these notes are in default and secured by a UCC-1 filing against GWTI's core patents. With the company's valuation deeply distressed, GWTI remains entirely untouchable for accretive acquisitions by midstream energy players; any prospective buyer would immediately trigger poison-pill debt covenants held by the C-suite.

Figure Strategic Assessment of Greenway Technologies (GWTl)

Supply Chain Pivot: The Single-Node BottleneckGWTI’s operational strategy relies on the modularity of its 2,000-barrel-per-day G-Reformer units, explicitly designed to bypass the massive footprint of legacy Steam Methane Reformation (SMR) facilities. However, the company has entirely ignored vertical integration, outsourcing 100% of its base refractory equipment manufacturing to a single, unnamed heavy equipment fabricator in Texas.

This hyper-localized supply chain poses a binary execution risk. The 2025 Annual Report explicitly acknowledges that replicating this bespoke manufacturing capability would cause indefinite delays. While the company aggressively pitches its synthesized high-value output (e.g., n-Hexane, n-Decane) as a geopolitical hedge against Chinese chemical supply chain dominance, its input reality is deeply fragile. GWTI holds zero long-term purchase obligations with this sole fabricator, leaving the company heavily exposed to regional cost inflation and manufacturer deprioritization.

HDIN Institutional Perspective: Arbitrage Sensitivity and Sector Cyclicality

From a macroeconomic vantage point, GWTI is attempting to disrupt the wellhead gas monetization sector at a highly precarious moment. The broader petrochemical industry is currently undergoing massive inventory de-stocking, forcing macro-refineries to grapple with acute margin compression.

GWTI’s theoretical economic viability is entirely anchored to the arbitrage spread between stranded natural gas input costs and crude oil output prices. Management’s own models require WTI/Brent crude to hover between $30 and $60 per barrel to maintain competitive profitability against traditional refining. Should commodity volatility narrow this spread, the adoption incentive for third-party operators vaporizes. Furthermore, GWTI faces an impending legal liquidity cliff—a mandatory $900,000 settlement payout beginning August 2026. Without immediate, highly dilutive equity financing (evidenced by the 9.97 million restricted shares already issued in Q1 2026), GWTI is positioned not as a disruptive tech pioneer, but as a cautionary tale of outsourced R&D collapsing under the weight of related-party leverage.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) is a premier institutional market intelligence firm specializing in forensic financial analysis, supply chain vulnerabilities, and geopolitical macroeconomic benchmarking. We transform opaque regulatory disclosures into actionable strategic alpha for global institutional investors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*