ENVue Medical Accelerates U.S. Supply Chain Pivot as FY2025 Margins Compress to 6.0% Amid Geopolitical Friction

Date : 2026-04-25

Reading : 97

Following its 2025 reverse merger, ENVue Medical reported a severe gross margin compression to 6.0% on stagnant $2.55 million revenues, triggering an $11.15 million asset impairment. To insulate its "razor-and-blade" enteral feeding ecosystem from Middle Eastern geopolitical volatility, the company is aggressively shifting its manufacturing base from Nesher, Israel, to U.S.-based contract manufacturers. This supply chain pivot aims to stabilize deeply negative cash flows—operating losses hit $(22.89) million—while the firm battles a $2.3 million arbitration liability and navigates institutional procurement roadblocks against legacy incumbents like Cardinal Health and Avanos Medical.

Financial Health & Operational Moats: The Cost of Commercial Scaling

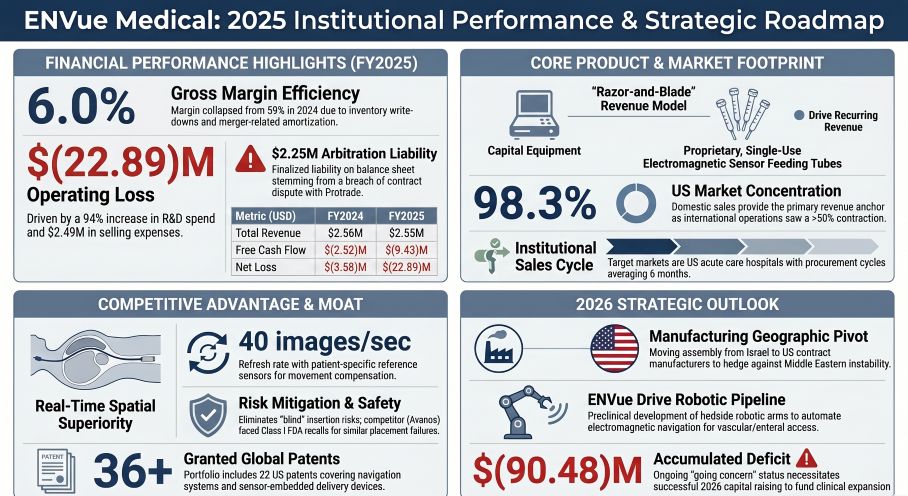

ENVue’s FY2025 Form 10-K illustrates the severe structural dual-pressure of transitioning a clinical-stage medical device portfolio into commercial viability. Revenue stagnated at $2.55 million (-0.2% YoY), while aggressive selling and marketing (S&M) expenditures surged to $2.49 million—consuming 98% of total revenue. This top-line stagnation, coupled with heavily discounted third-party distribution agreements (which account for 98% of sales), drove a catastrophic gross margin compression from 59.0% in 2024 down to just 6.0% in 2025.

The balance sheet reflects a highly asymmetric capital allocation strategy. The February 2025 reverse merger, initially capitalized at $42.45 million, ultimately failed to materialize as an immediately accretive acquisition. The company was forced to record a massive $11.15 million non-cash impairment charge, writing down legacy goodwill and long-lived assets. With capital expenditures running at a nominal $60,000 against $1.76 million in R&D, the firm operates an ultra-lean, asset-light model. However, an unproven proxy Customer Lifetime Value (LTV) relative to ballooning acquisition costs (CAC) has resulted in a deeply negative Free Cash Flow of $(9.43) million, triggering a formal "going concern" warning from management.

Figure ENVue Medical 2025 Institutional Performance & Strategic Roadmap

Supply Chain Pivot: Hedging Geopolitical Alpha

Supply Chain Pivot: Hedging Geopolitical Alpha

ENVue's operational epicenter in Nesher, Israel, currently faces existential macroeconomic and geopolitical risks stemming from regional military conflicts. Lacking true vertical integration, the company outsources critical component fabrication on an uncontracted, "as-needed" basis to distinct single-node suppliers such as B Star, Inc. and Plastic One.

To hedge against catastrophic supply chain paralysis, ENVue is executing a structural geographic realignment. Management is migrating proprietary disposable kit assembly to a U.S.-based Contract Manufacturer while utilizing Arlington Heights, Illinois, as its centralized North American logistics hub. This transition is essential not just for risk mitigation, but to establish reliable cost-pass-through mechanisms and stabilize the sourcing of highly specialized polyurethane feeding tubes, which remain a severe global bottleneck for the ENVue System.

Regulatory Arbitrage & Inventory De-Stocking Realities

The MedTech sector’s regulatory apparatus routinely functions as a double-edged sword, a dynamic acutely visible in ENVue's 2025 audit. On the defensive front, the company suffered a $346,000 inventory write-down linked directly to forced inventory de-stocking. Management halted future sales of the PainShield MD Plus device upon discovering inaccuracies in its 2022 FDA 510(k) application. This commercial withdrawal cascaded into a $2.25 million accrued arbitration liability against legacy distributor Protrade Systems, effectively vaporizing near-term balance sheet liquidity. Furthermore, consecutive reimbursement denials by the Centers for Medicare & Medicaid Services (CMS) have forced the company to pivot commercial targeting toward the Veterans Health Care network and the UK's National Health Service (NHS).

Conversely, ENVue is strategically weaponizing its competitors' regulatory failures. Avanos Medical’s competing Cortrak 2 electromagnetic system suffered a Class I FDA recall in 2022 due to fatal blind-insertion injuries. ENVue leverages this incumbent failure by anchoring its unique selling proposition (USP) on its real-time, 40-frames-per-second patient-specific airway deviation alerts, positioning its proprietary disposable tubes as the de facto risk-mitigation standard for hospital Value Analysis Committees.

HDIN Institutional Perspective

ENVue Medical represents a classic "Razor-and-Blade" inflection play currently trapped in a liquidity trough. The fundamental enterprise value is entirely tethered to the proprietary ENVue System and its upcoming pediatric and robotic (ENVue Drive) line extensions. However, the legacy NanoVibronix division (accounting for 72.7% of current revenues) is acting as a margin dilutive anchor rather than a cash cow.

The firm's heavy reliance on a single third-party distributor, Ultra Pain Products Inc. (31% of revenue), masks the underlying lack of direct institutional penetration. For ENVue to cure its "going concern" status and justify future equity dilution, management must definitively prove that its U.S. manufacturing pivot can resuscitate gross margins beyond the 50% threshold, while simultaneously securing localized GPO (Group Purchasing Organization) contracts to offset the crippling S&M cash burn. Until these unit economics flip, ENVue remains a high-beta intellectual property vault rather than a scalable commercial enterprise.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

Discover more institutional-grade market intelligence and SEC filing deconstructions at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cost of Commercial Scaling

ENVue’s FY2025 Form 10-K illustrates the severe structural dual-pressure of transitioning a clinical-stage medical device portfolio into commercial viability. Revenue stagnated at $2.55 million (-0.2% YoY), while aggressive selling and marketing (S&M) expenditures surged to $2.49 million—consuming 98% of total revenue. This top-line stagnation, coupled with heavily discounted third-party distribution agreements (which account for 98% of sales), drove a catastrophic gross margin compression from 59.0% in 2024 down to just 6.0% in 2025.

The balance sheet reflects a highly asymmetric capital allocation strategy. The February 2025 reverse merger, initially capitalized at $42.45 million, ultimately failed to materialize as an immediately accretive acquisition. The company was forced to record a massive $11.15 million non-cash impairment charge, writing down legacy goodwill and long-lived assets. With capital expenditures running at a nominal $60,000 against $1.76 million in R&D, the firm operates an ultra-lean, asset-light model. However, an unproven proxy Customer Lifetime Value (LTV) relative to ballooning acquisition costs (CAC) has resulted in a deeply negative Free Cash Flow of $(9.43) million, triggering a formal "going concern" warning from management.

Figure ENVue Medical 2025 Institutional Performance & Strategic Roadmap

Supply Chain Pivot: Hedging Geopolitical AlphaENVue's operational epicenter in Nesher, Israel, currently faces existential macroeconomic and geopolitical risks stemming from regional military conflicts. Lacking true vertical integration, the company outsources critical component fabrication on an uncontracted, "as-needed" basis to distinct single-node suppliers such as B Star, Inc. and Plastic One.

To hedge against catastrophic supply chain paralysis, ENVue is executing a structural geographic realignment. Management is migrating proprietary disposable kit assembly to a U.S.-based Contract Manufacturer while utilizing Arlington Heights, Illinois, as its centralized North American logistics hub. This transition is essential not just for risk mitigation, but to establish reliable cost-pass-through mechanisms and stabilize the sourcing of highly specialized polyurethane feeding tubes, which remain a severe global bottleneck for the ENVue System.

Regulatory Arbitrage & Inventory De-Stocking Realities

The MedTech sector’s regulatory apparatus routinely functions as a double-edged sword, a dynamic acutely visible in ENVue's 2025 audit. On the defensive front, the company suffered a $346,000 inventory write-down linked directly to forced inventory de-stocking. Management halted future sales of the PainShield MD Plus device upon discovering inaccuracies in its 2022 FDA 510(k) application. This commercial withdrawal cascaded into a $2.25 million accrued arbitration liability against legacy distributor Protrade Systems, effectively vaporizing near-term balance sheet liquidity. Furthermore, consecutive reimbursement denials by the Centers for Medicare & Medicaid Services (CMS) have forced the company to pivot commercial targeting toward the Veterans Health Care network and the UK's National Health Service (NHS).

Conversely, ENVue is strategically weaponizing its competitors' regulatory failures. Avanos Medical’s competing Cortrak 2 electromagnetic system suffered a Class I FDA recall in 2022 due to fatal blind-insertion injuries. ENVue leverages this incumbent failure by anchoring its unique selling proposition (USP) on its real-time, 40-frames-per-second patient-specific airway deviation alerts, positioning its proprietary disposable tubes as the de facto risk-mitigation standard for hospital Value Analysis Committees.

HDIN Institutional Perspective

ENVue Medical represents a classic "Razor-and-Blade" inflection play currently trapped in a liquidity trough. The fundamental enterprise value is entirely tethered to the proprietary ENVue System and its upcoming pediatric and robotic (ENVue Drive) line extensions. However, the legacy NanoVibronix division (accounting for 72.7% of current revenues) is acting as a margin dilutive anchor rather than a cash cow.

The firm's heavy reliance on a single third-party distributor, Ultra Pain Products Inc. (31% of revenue), masks the underlying lack of direct institutional penetration. For ENVue to cure its "going concern" status and justify future equity dilution, management must definitively prove that its U.S. manufacturing pivot can resuscitate gross margins beyond the 50% threshold, while simultaneously securing localized GPO (Group Purchasing Organization) contracts to offset the crippling S&M cash burn. Until these unit economics flip, ENVue remains a high-beta intellectual property vault rather than a scalable commercial enterprise.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

Discover more institutional-grade market intelligence and SEC filing deconstructions at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*