Ultra-Premium Spirits Cycle Hits Trough: Kweichow Moutai Signals Inventory De-stocking as FY2025 Core Revenue Contracts 1.2%

Date : 2026-04-23

Reading : 174

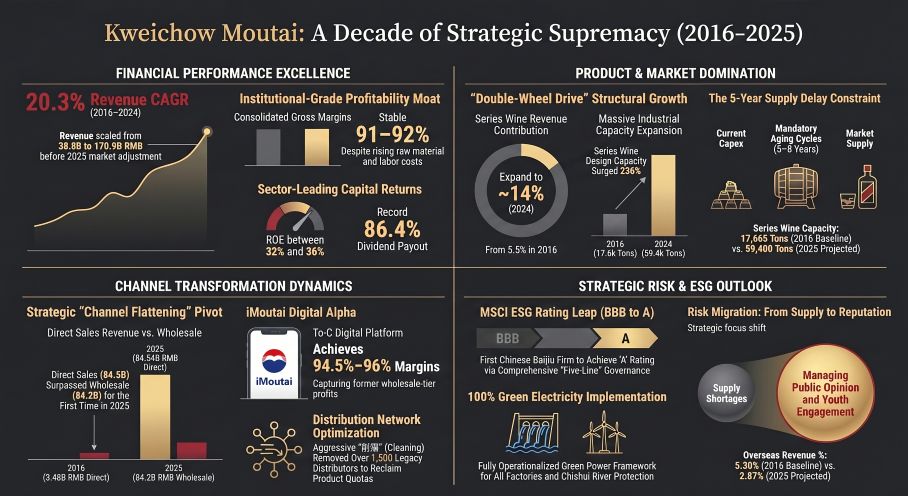

Kweichow Moutai (SHA: 600519) reported its first top-line contraction in a decade during its FY2025 audit, posting a 1.21% revenue decline to RMB 168.84 billion amid a broader domestic macroeconomic reset. Operating out of its Chishui River manufacturing hub, the distiller’s data exposes severe channel pressures as it draws down multi-billion-yuan distributor contract liabilities to smooth earnings. This inflection point forces a structural pivot from pure supply-scarcity wholesale toward direct-to-consumer vertical integration, strategically engineered to insulate its unprecedented 91.23% gross margins against shifting consumer demographics.

Financial Health & Operational Moats: The "iMoutai" Vertical Integration

Kweichow Moutai’s financial architecture is undergoing a radical stress test. After maintaining a 20.3% revenue CAGR from 2016 to 2024, the FY2025 print reveals a net profit dip of 4.53% to RMB 82.32 billion. However, the raw figures mask a sophisticated margin defense mechanism. To stave off margin compression amidst rising raw material (sorghum/wheat) and direct labor costs, management accelerated its vertical integration via the "iMoutai" direct-to-consumer (DTC) digital ecosystem.

By FY2025, DTC revenue (RMB 84.54 billion) officially eclipsed the traditional wholesale proxy (RMB 84.23 billion). Operating at a 95.07% gross margin compared to the wholesale segment's 87.37%, this channel restructuring acts as an internal cost-pass-through mechanism. By reclaiming the premium previously captured by regional distributors, Moutai effectively neutralized upstream inflationary pressures without requiring headline-grabbing factory gate price hikes.

Yet, institutional scrutiny must center on the balance sheet's "Contract Liabilities." Historically operating as a massive interest-free liquidity reservoir where distributors prepaid for allocations, this line item plummeted by 32.09% to RMB 9.59 billion in late 2024. This aggressive liquidation of the earnings buffer signals that downstream distributors lack the cash velocity to maintain traditional inventory stockpiles, pointing toward an extended period of inventory de-stocking across the broader luxury spirits tier.

Figure Kweichow Moutai: A Decade of Strategic Supremacy (2016-2025)

Supply Chain Pivot: Capex Cycles and The Five-Year Collision

Supply Chain Pivot: Capex Cycles and The Five-Year Collision

Moutai’s localized supply chain rests entirely within a 15.03-square-kilometer ecologically protected zone along the Chishui River. The company is currently executing the RMB 15.52 billion "14th Five-Year" Moutai liquor capacity expansion project in the Zhonghua area, alongside an RMB 8.38 billion CAPEX allocation for a 30,000-ton Series Liquor facility (targeting the mid-tier market).

The institutional risk lies in the immutable physical laws of the product: base liquor requires a mandatory five-year maturation cycle before commercial release. Therefore, CAPEX deployed today determines market supply in 2030. Between 2016 and 2025, actual production of flagship Moutai base liquor operated consistently above 115% of designed capacity (hitting 58,473 tons in 2025). As these massive, lagging capacity additions come online, they risk colliding with a structurally altered, lower-growth Chinese consumer market. The company’s inability to dynamically scale production down in real-time creates a rigid supply curve that could test the brand's pricing elasticity over the next half-decade.

HDIN Institutional Perspective: Yield Over Expansion

Kweichow Moutai's FY2025 audit serves as the ultimate macro barometer for Chinese elite consumption. The transition from a supply-constrained monopoly to a demand-rationing consumer goods entity is now mathematically verifiable. Rather than seeking accretive acquisitions to patch near-term growth gaps, newly appointed Chairman Chen Hua has anchored the equity narrative around unprecedented shareholder returns.

For FY2025, the company deployed a combined special and interim dividend strategy yielding over RMB 71.15 billion—an 86.43% payout ratio. This aggressive capital return profile, coupled with an upgraded MSCI ESG rating to 'A' driven by 100% green electricity adoption and vast local ecological funding, transitions SHA:600519 from a pure-play growth juggernaut into a defensive, high-yield cash cow. The Street must re-rate Moutai not on its capacity to expand output, but on its ability to enforce strict market quotas while bleeding off excess distributor inventory through its proprietary digital nodes.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in dissecting corporate filings and macroeconomic shifts to deliver actionable, data-dense strategies for global asset managers. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The "iMoutai" Vertical Integration

Kweichow Moutai’s financial architecture is undergoing a radical stress test. After maintaining a 20.3% revenue CAGR from 2016 to 2024, the FY2025 print reveals a net profit dip of 4.53% to RMB 82.32 billion. However, the raw figures mask a sophisticated margin defense mechanism. To stave off margin compression amidst rising raw material (sorghum/wheat) and direct labor costs, management accelerated its vertical integration via the "iMoutai" direct-to-consumer (DTC) digital ecosystem.

By FY2025, DTC revenue (RMB 84.54 billion) officially eclipsed the traditional wholesale proxy (RMB 84.23 billion). Operating at a 95.07% gross margin compared to the wholesale segment's 87.37%, this channel restructuring acts as an internal cost-pass-through mechanism. By reclaiming the premium previously captured by regional distributors, Moutai effectively neutralized upstream inflationary pressures without requiring headline-grabbing factory gate price hikes.

Yet, institutional scrutiny must center on the balance sheet's "Contract Liabilities." Historically operating as a massive interest-free liquidity reservoir where distributors prepaid for allocations, this line item plummeted by 32.09% to RMB 9.59 billion in late 2024. This aggressive liquidation of the earnings buffer signals that downstream distributors lack the cash velocity to maintain traditional inventory stockpiles, pointing toward an extended period of inventory de-stocking across the broader luxury spirits tier.

Figure Kweichow Moutai: A Decade of Strategic Supremacy (2016-2025)

Supply Chain Pivot: Capex Cycles and The Five-Year CollisionMoutai’s localized supply chain rests entirely within a 15.03-square-kilometer ecologically protected zone along the Chishui River. The company is currently executing the RMB 15.52 billion "14th Five-Year" Moutai liquor capacity expansion project in the Zhonghua area, alongside an RMB 8.38 billion CAPEX allocation for a 30,000-ton Series Liquor facility (targeting the mid-tier market).

The institutional risk lies in the immutable physical laws of the product: base liquor requires a mandatory five-year maturation cycle before commercial release. Therefore, CAPEX deployed today determines market supply in 2030. Between 2016 and 2025, actual production of flagship Moutai base liquor operated consistently above 115% of designed capacity (hitting 58,473 tons in 2025). As these massive, lagging capacity additions come online, they risk colliding with a structurally altered, lower-growth Chinese consumer market. The company’s inability to dynamically scale production down in real-time creates a rigid supply curve that could test the brand's pricing elasticity over the next half-decade.

HDIN Institutional Perspective: Yield Over Expansion

Kweichow Moutai's FY2025 audit serves as the ultimate macro barometer for Chinese elite consumption. The transition from a supply-constrained monopoly to a demand-rationing consumer goods entity is now mathematically verifiable. Rather than seeking accretive acquisitions to patch near-term growth gaps, newly appointed Chairman Chen Hua has anchored the equity narrative around unprecedented shareholder returns.

For FY2025, the company deployed a combined special and interim dividend strategy yielding over RMB 71.15 billion—an 86.43% payout ratio. This aggressive capital return profile, coupled with an upgraded MSCI ESG rating to 'A' driven by 100% green electricity adoption and vast local ecological funding, transitions SHA:600519 from a pure-play growth juggernaut into a defensive, high-yield cash cow. The Street must re-rate Moutai not on its capacity to expand output, but on its ability to enforce strict market quotas while bleeding off excess distributor inventory through its proprietary digital nodes.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in dissecting corporate filings and macroeconomic shifts to deliver actionable, data-dense strategies for global asset managers. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.