Vystar Corporation Pivots to Web3 Ecosystem as FY2025 Core Revenue Collapses 59.7% Amid Terminal Liquidity Crunch

Date : 2026-04-26

Reading : 82

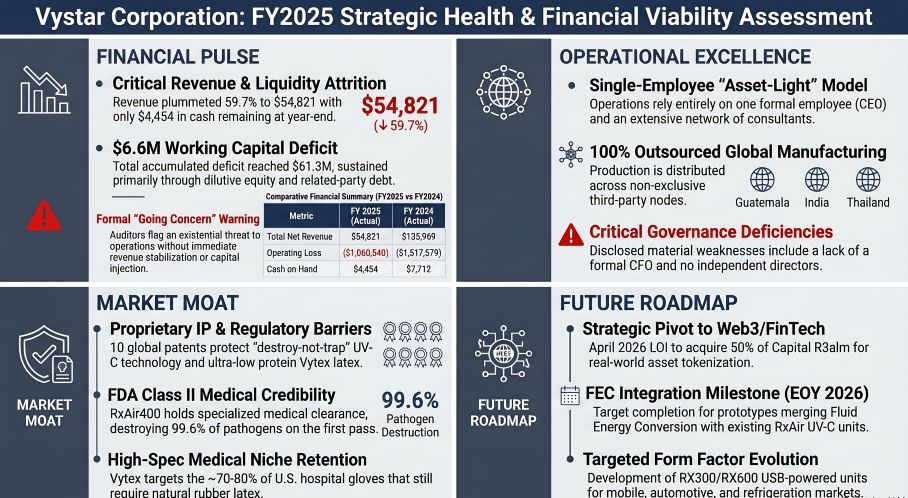

Micro-cap holding company Vystar Corporation (OTC: VYST) reported a devastating 59.7% top-line collapse to just $54,821 in its FY2025 SEC audit. Paralyzed by a terminal liquidity crisis—ending the year with a mere $4,454 in cash—and paralyzed B2B capital expenditure environments, the company is effectively abandoning its legacy advanced materials commercialization. In April 2026, Vystar executed a binding LOI to acquire 50% of digital asset firm Capital R3alm, Inc., signaling a desperate structural pivot to reposition its distressed public shell away from physical supply chains and into the decentralized finance sector.

Financial Health & Stranded Moats

A forensic audit of Vystar’s 2025 10-K reveals a corporate entity functioning fundamentally as a capital-starved public shell. While consolidated gross margins optically expanded to 58.0% (up from 51.2% in 2024), this metric is entirely distorted by a microscopic volume base. The loss of a primary customer evaporated demand, while operating cash flows bled an additional $180,393. The accumulated deficit now breaches $61.38 million.

Vystar possesses a theoretically robust intellectual property moat, yet it remains commercially stranded. The RxAir division retains its critical FDA Class II medical device clearance for the RxAir400 unit, backed by ViraTech technology proven to eradicate 99.6% of airborne pathogens. Similarly, its Vytex Natural Rubber Latex (NRL) strips antigenic proteins to virtually undetectable levels.

However, the "so what" here is regulatory and macroeconomic friction. The FDA’s persistent refusal to remove mandatory latex allergy labels from exam gloves utilizing Vytex neutralizes Vystar's primary marketing premium. Furthermore, in a tightened macroeconomic environment, heavy B2B rubber manufacturers simply will not deploy discretionary capital to retool their assembly lines for Vytex integration. With internal R&D expenditure effectively zeroed out to preserve cash, Vystar's legacy IP portfolio is trapped in a state of suspended animation.

Figure Vystar Corporation FY2025 Strategic Health & Financial Viability Assessment

Offshore Dependencies and Tariff Vulnerabilities

Offshore Dependencies and Tariff Vulnerabilities

Operating with exactly one official employee (CEO Jamie Rotman), Vystar completely lacks vertical integration. The company is exclusively reliant on an outsourced, highly fragmented matrix of international production nodes, including Revertex (Malaysia), Occidente (Guatemala), KAPVL (India), and Mardec-Yala (Thailand).

This asset-light model has morphed into a fatal liability. By outsourcing master distribution and manufacturing to CMC Global (Corrie MacColl Limited), Vystar has surrendered control over its own cost-pass-through mechanisms. Without direct control over manufacturing timelines, the company is highly exposed to ocean freight volatility, prolonged lead times, and the looming threat of U.S. tariff escalations on Asian imports. If raw latex commodity prices spike, Vystar lacks the scale to absorb the margin compression, heavily incentivizing downstream manufacturers to accelerate inventory de-stocking or pivot entirely to cheaper synthetic alternatives (e.g., ethylene or butadiene).

HDIN Institutional Perspective: The Micro-Cap Pivot Cycle

Vystar’s trajectory serves as a textbook leading indicator for the broader micro-cap industrial cycle. When access to highly dilutive retail equity funding evaporates, hardware and materials companies with protracted commercialization timelines inevitably face a binary outcome: bankruptcy or a radical sector pivot.

The April 2026 binding LOI to acquire 50% of Capital R3alm, Inc.—an ecosystem geared toward tokenized real-world assets and AI-powered financial intelligence—is not an organic extension of Vystar’s core competencies. Rather, it is a distressed corporate shell maneuver. Management is betting that integrating a Web3 narrative will serve as an accretive acquisition to resuscitate its OTC equity liquidity. This marks a definitive cyclical trough for Vystar’s legacy physical goods divisions, as the entity attempts to outrun a "Going Concern" audit qualification by transforming into a digital asset holding company.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic market intelligence firm specializing in institutional-grade financial deconstruction, forensic SEC filing analysis, and macroeconomic thesis generation. We provide alpha-generating insights for hedge funds, private equity, and institutional capital allocators worldwide. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Stranded Moats

A forensic audit of Vystar’s 2025 10-K reveals a corporate entity functioning fundamentally as a capital-starved public shell. While consolidated gross margins optically expanded to 58.0% (up from 51.2% in 2024), this metric is entirely distorted by a microscopic volume base. The loss of a primary customer evaporated demand, while operating cash flows bled an additional $180,393. The accumulated deficit now breaches $61.38 million.

Vystar possesses a theoretically robust intellectual property moat, yet it remains commercially stranded. The RxAir division retains its critical FDA Class II medical device clearance for the RxAir400 unit, backed by ViraTech technology proven to eradicate 99.6% of airborne pathogens. Similarly, its Vytex Natural Rubber Latex (NRL) strips antigenic proteins to virtually undetectable levels.

However, the "so what" here is regulatory and macroeconomic friction. The FDA’s persistent refusal to remove mandatory latex allergy labels from exam gloves utilizing Vytex neutralizes Vystar's primary marketing premium. Furthermore, in a tightened macroeconomic environment, heavy B2B rubber manufacturers simply will not deploy discretionary capital to retool their assembly lines for Vytex integration. With internal R&D expenditure effectively zeroed out to preserve cash, Vystar's legacy IP portfolio is trapped in a state of suspended animation.

Figure Vystar Corporation FY2025 Strategic Health & Financial Viability Assessment

Offshore Dependencies and Tariff VulnerabilitiesOperating with exactly one official employee (CEO Jamie Rotman), Vystar completely lacks vertical integration. The company is exclusively reliant on an outsourced, highly fragmented matrix of international production nodes, including Revertex (Malaysia), Occidente (Guatemala), KAPVL (India), and Mardec-Yala (Thailand).

This asset-light model has morphed into a fatal liability. By outsourcing master distribution and manufacturing to CMC Global (Corrie MacColl Limited), Vystar has surrendered control over its own cost-pass-through mechanisms. Without direct control over manufacturing timelines, the company is highly exposed to ocean freight volatility, prolonged lead times, and the looming threat of U.S. tariff escalations on Asian imports. If raw latex commodity prices spike, Vystar lacks the scale to absorb the margin compression, heavily incentivizing downstream manufacturers to accelerate inventory de-stocking or pivot entirely to cheaper synthetic alternatives (e.g., ethylene or butadiene).

HDIN Institutional Perspective: The Micro-Cap Pivot Cycle

Vystar’s trajectory serves as a textbook leading indicator for the broader micro-cap industrial cycle. When access to highly dilutive retail equity funding evaporates, hardware and materials companies with protracted commercialization timelines inevitably face a binary outcome: bankruptcy or a radical sector pivot.

The April 2026 binding LOI to acquire 50% of Capital R3alm, Inc.—an ecosystem geared toward tokenized real-world assets and AI-powered financial intelligence—is not an organic extension of Vystar’s core competencies. Rather, it is a distressed corporate shell maneuver. Management is betting that integrating a Web3 narrative will serve as an accretive acquisition to resuscitate its OTC equity liquidity. This marks a definitive cyclical trough for Vystar’s legacy physical goods divisions, as the entity attempts to outrun a "Going Concern" audit qualification by transforming into a digital asset holding company.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier strategic market intelligence firm specializing in institutional-grade financial deconstruction, forensic SEC filing analysis, and macroeconomic thesis generation. We provide alpha-generating insights for hedge funds, private equity, and institutional capital allocators worldwide. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*