Polyurethane Cycle Hits Trough: Wanhua Chemical Counters Petrochemical Margin Compression with Battery Materials Pivot in $28.3B FY2025 Audit

Date : 2026-04-23

Reading : 353

In its FY2025 audit, global isocyanate giant Wanhua Chemical (SHA: 600309) reported an 11.62% revenue surge to $28.28 billion, paradoxically coupled with a 3.88% net profit contraction to $1.74 billion. This structural decoupling exposes a brutal macroeconomic trough characterized by tariff barriers and sluggish downstream demand. To defend its oligopolistic positioning, the Yantai-headquartered firm is executing a massive supply chain pivot, leveraging its proprietary 8th-generation MDI technology and commercializing Europe's first Lithium Iron Phosphate (LFP) battery facility at its BorsodChem hub to neutralize geopolitical friction and regionalized trade fragmentation.

Financial Health & Operational Moats: The Cash Flow Disconnect

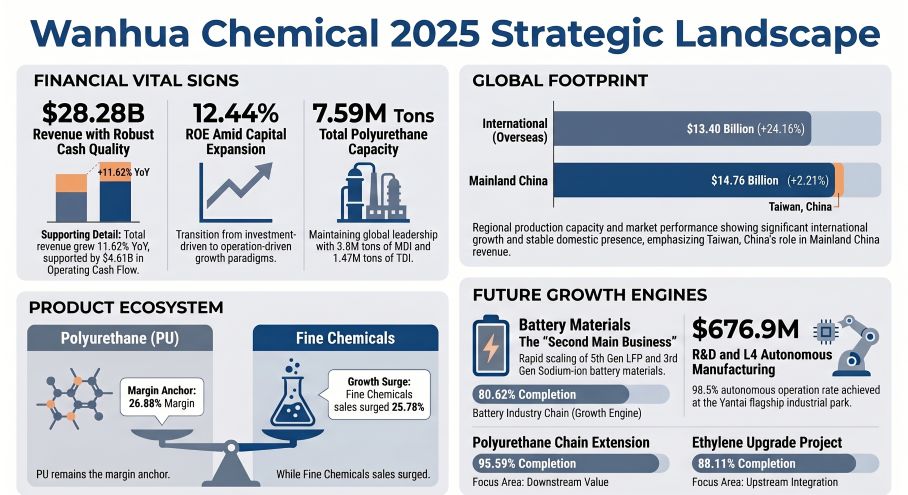

A surface-level reading of Wanhua’s FY2025 income statement suggests vulnerability, but a forensic examination of the balance sheet reveals a formidable operational moat. The company’s weighted average ROE declined to 12.44%, a mathematical inevitability driven by $4.27 billion in heavy capital expenditures entering the asset base.

However, Wanhua generated a staggering $4.61 billion in operating cash flow (OCF)—outpacing reported net profit by a factor of 2.6x. This cash conversion machinery is fueled by $2.03 billion in non-cash depreciation and aggressive supply chain financing.

Segment divergence is stark. The Polyurethane (PU) division remains the ultimate cash cow. Despite a 1.04% revenue dip, gross margins actually expanded by 0.73 percentage points to 26.88%. This anomaly underscores Wanhua’s pricing power and highly effective cost-pass-through mechanisms in the MDI/TDI oligopoly. Conversely, the Petrochemical segment acts as a revenue engine but a margin anchor; revenues surged 16.11% to $11.72 billion, yet gross margins plummeted to a razor-thin 0.58%. This reflects a localized bloodbath in Chinese petrochemicals, where overcapacity has entirely eroded profitability, forcing Wanhua to rely on volume to cover fixed costs.

Figure Wanhua Chemical 2025 Strategic Landscape

Supply Chain Pivot: Decentralization and "Agile Procurement"

Supply Chain Pivot: Decentralization and "Agile Procurement"

Facing a fragmented global trade environment and severe raw material volatility, Wanhua has aggressively restructured its manufacturing footprint. The company is actively shifting away from a China-centric export model toward localized vertical integration.

The cornerstone of this pivot is the BorsodChem (BC Company) facility in Hungary. By deploying its 8th-generation MDI technology and advancing the European continent’s first LFP battery materials project, Wanhua is building a localized fortress against escalating EU tariff barriers.

On the feedstock front, the company has engineered structural flexibility. The Yantai Phase I plant completed a critical raw material diversification upgrade, enabling a 100% ethane feed. Coupled with derivative financial instruments—specifically LPG and natural gas swap contracts—and an "agile procurement" strategy that increased 5-day delivery rates to 76%, Wanhua is structurally insulating its cost base. Furthermore, the company supplemented its organic growth with accretive acquisitions, notably acquiring the HDI adduct business from Vencorex France SAS to consolidate its specialty isocyanate market share.

HDIN Institutional Perspective: Signaling the Macro Trough

Wanhua’s FY2025 performance is not merely a corporate earnings report; it is a macro-diagnostic tool for the global chemical sector. The near-zero margin (0.58%) in Wanhua’s Petrochemical division, despite the commissioning of the massive Yantai Phase II and Penglai POCHP plants, signals that the broader ethylene and propylene cycle has hit absolute bottom. We anticipate aggressive inventory de-stocking across Tier-2 and Tier-3 global competitors in 2026, as operators lacking Wanhua’s scale are forced into margin calls or capacity shutdowns.

Furthermore, management’s highly conservative R&D accounting dictates attention. Wanhua expensed 100% of its $676.90 million R&D budget in 2025, refusing to capitalize any of it. This ruthless balance sheet management absorbs the financial hit today, clearing the deck for future profitability. The deployment of "AI for Science" frameworks and L4 autonomous manufacturing (reaching a 98.5% automation rate in Yantai) indicates that Wanhua is no longer competing solely on capacity scale; it is fundamentally altering the unit economics of chemical manufacturing.

By pivoting its "Second Main Business" into silicon-carbon anodes and battery materials, Wanhua is aggressively positioning itself for the next supercycle, leaving legacy petrochemical pure-plays stranded at the bottom of the curve.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) provides institutional-grade market intelligence, specializing in macroeconomic cycles, deep-value supply chain analysis, and strategic equity research across global industrial and chemical sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: The Cash Flow Disconnect

A surface-level reading of Wanhua’s FY2025 income statement suggests vulnerability, but a forensic examination of the balance sheet reveals a formidable operational moat. The company’s weighted average ROE declined to 12.44%, a mathematical inevitability driven by $4.27 billion in heavy capital expenditures entering the asset base.

However, Wanhua generated a staggering $4.61 billion in operating cash flow (OCF)—outpacing reported net profit by a factor of 2.6x. This cash conversion machinery is fueled by $2.03 billion in non-cash depreciation and aggressive supply chain financing.

Segment divergence is stark. The Polyurethane (PU) division remains the ultimate cash cow. Despite a 1.04% revenue dip, gross margins actually expanded by 0.73 percentage points to 26.88%. This anomaly underscores Wanhua’s pricing power and highly effective cost-pass-through mechanisms in the MDI/TDI oligopoly. Conversely, the Petrochemical segment acts as a revenue engine but a margin anchor; revenues surged 16.11% to $11.72 billion, yet gross margins plummeted to a razor-thin 0.58%. This reflects a localized bloodbath in Chinese petrochemicals, where overcapacity has entirely eroded profitability, forcing Wanhua to rely on volume to cover fixed costs.

Figure Wanhua Chemical 2025 Strategic Landscape

Supply Chain Pivot: Decentralization and "Agile Procurement"Facing a fragmented global trade environment and severe raw material volatility, Wanhua has aggressively restructured its manufacturing footprint. The company is actively shifting away from a China-centric export model toward localized vertical integration.

The cornerstone of this pivot is the BorsodChem (BC Company) facility in Hungary. By deploying its 8th-generation MDI technology and advancing the European continent’s first LFP battery materials project, Wanhua is building a localized fortress against escalating EU tariff barriers.

On the feedstock front, the company has engineered structural flexibility. The Yantai Phase I plant completed a critical raw material diversification upgrade, enabling a 100% ethane feed. Coupled with derivative financial instruments—specifically LPG and natural gas swap contracts—and an "agile procurement" strategy that increased 5-day delivery rates to 76%, Wanhua is structurally insulating its cost base. Furthermore, the company supplemented its organic growth with accretive acquisitions, notably acquiring the HDI adduct business from Vencorex France SAS to consolidate its specialty isocyanate market share.

HDIN Institutional Perspective: Signaling the Macro Trough

Wanhua’s FY2025 performance is not merely a corporate earnings report; it is a macro-diagnostic tool for the global chemical sector. The near-zero margin (0.58%) in Wanhua’s Petrochemical division, despite the commissioning of the massive Yantai Phase II and Penglai POCHP plants, signals that the broader ethylene and propylene cycle has hit absolute bottom. We anticipate aggressive inventory de-stocking across Tier-2 and Tier-3 global competitors in 2026, as operators lacking Wanhua’s scale are forced into margin calls or capacity shutdowns.

Furthermore, management’s highly conservative R&D accounting dictates attention. Wanhua expensed 100% of its $676.90 million R&D budget in 2025, refusing to capitalize any of it. This ruthless balance sheet management absorbs the financial hit today, clearing the deck for future profitability. The deployment of "AI for Science" frameworks and L4 autonomous manufacturing (reaching a 98.5% automation rate in Yantai) indicates that Wanhua is no longer competing solely on capacity scale; it is fundamentally altering the unit economics of chemical manufacturing.

By pivoting its "Second Main Business" into silicon-carbon anodes and battery materials, Wanhua is aggressively positioning itself for the next supercycle, leaving legacy petrochemical pure-plays stranded at the bottom of the curve.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research (www.hdinresearch.com) provides institutional-grade market intelligence, specializing in macroeconomic cycles, deep-value supply chain analysis, and strategic equity research across global industrial and chemical sectors.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*