Bodycote (LON: BOY) Accelerates Aerospace CAPEX to $101M as European Industrial Margin Compression Forces Structural Re-rating

Date : 2026-04-26

Reading : 55

Following its FY2025 audit, thermal processing giant Bodycote plc (LON: BOY) is aggressively redirecting $101.58 million in CAPEX toward North American Aerospace & Defence (A&D) nodes and Asian greenfield sites. To offset a 130-basis-point margin compression triggered by European automotive cyclicality, management is divesting non-core assets while executing a $105.54 million share buyback. This strategic pivot capitalizes on an easing A&D supply chain and tightening global carbon regulations, transforming the 80% of processing still handled via in-house OEM furnaces into a captive target market for Bodycote’s proprietary, zero-emission technologies.

Pricing Power Amidst Margin Compression

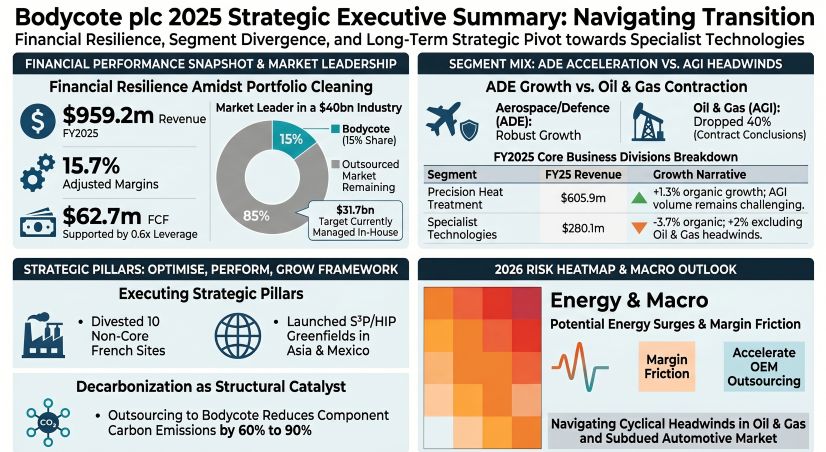

Bodycote’s FY2025 financial disclosures reveal a stark bifurcation in end-market dynamics. While total revenue contracted 4.0% to $959.19 million, effectively masking the underlying strength of the enterprise, a deeper forensic analysis indicates highly deliberate portfolio pruning.

Faced with severe cyclical headwinds and low asset utilization in the Automotive & General Industrial (AGI) sectors, Bodycote experienced friction in its cost-pass-through mechanisms. Utility costs edged up to $92.74 million despite a 4.2% drop in energy consumption, leading to a headline operating margin contraction to 15.7%. Rather than absorb this structural inefficiency, management initiated its "Optimise" restructuring program—aggressively divesting 10 non-core, automotive-heavy facilities in France for $25.46 million and retiring older, carbon-intensive assets.

This short-term top-line sacrifice fundamentally hardens the company's economic moat. By retaining a highly defensive balance sheet (Net Debt/EBITDA of just 0.6x) and clearing legacy impairments, Bodycote successfully maintained its 30.34 US cents per share dividend and initiated a new $105.54 million share buyback extending to 2027. Furthermore, the bolt-on accretive acquisition of Spectrum Thermal Processing in Rhode Island immediately captures high-margin, Nadcap-accredited market share in the US aerospace sector, effectively trading low-margin European automotive revenue for highly defensible A&D yield.

Figure Bodycote plc 2025 Strategic Executive Summary

Nearshoring and the "Zero-Emission" Premium

Nearshoring and the "Zero-Emission" Premium

The 2026–2027 operational outlook hinges on capitalizing on regional supply chain shifts and stringent decarbonization mandates. Bodycote is explicitly aligning its asset base to intersect with OEM nearshoring and vertical disintegration trends.

Key capital allocation targets include:

* Capacity Expansion in Peak-Utilization Nodes: A&D supply chain constraints have materially improved, triggering a surge in throughput. Bodycote is funding major US capacity upgrades, including Hot Isostatic Pressing (HIP) expansions, and utilizing lean manufacturing processes that recently saved 500 square feet of floor space at its Cincinnati aerospace site.

* Emerging Market Greenfield Deployment: The firm is deploying its proprietary Specialty Stainless Steel Processes (S³P) into the Asian market via a new greenfield facility (commissioning late 2026/early 2027), addressing the stark disparity where Emerging Markets currently represent only $9.50 million of Specialist Technologies revenue.

* Nearshoring via Mexico: A new greenfield site in Mexico is slated to capture North American automotive and industrial supply chain re-alignment, generating meaningful revenue by 2027.

Crucially, Bodycote has weaponized ESG compliance as a commercial lever. The company stress-tested an internal carbon price of $131.92/tonne. With the looming threat of cross-border carbon mechanisms (e.g., CBAM), OEMs operating inefficient in-house furnaces face massive compliance liabilities. Bodycote’s deployment of 100% electrified, zero-emission pathfinder plants in Derby and Rotherham allows OEMs to outsource their thermal processing and instantly reduce component carbon footprints by up to 60%, fully backed by Bureau Veritas-verified product carbon footprint data.

HDIN Institutional Perspective: The In-House TAM Unlock

The street is mispricing Bodycote as a pure-play industrial cyclical. HDIN Research views the FY2025 data not as a signal of deterioration, but as the trough of a deliberate transition cycle. The true alpha lies in the ~80% of the $39.58 billion global thermal processing market that remains in-house.

As energy price volatility threatens the viability of captive OEM furnaces, the capital hurdle for OEMs to upgrade legacy equipment to meet Scope 1 and 2 emissions mandates becomes prohibitive. This environment accelerates the transition from in-house processing to outsourced specialist partners. Bodycote’s integration of Emmanuelle Dubu—a seasoned metallurgist and former manufacturing CEO—onto its Board signals a tightened grip on advanced technical governance.

While a buildup in Work-in-Progress (WIP) inventory (spiking 72% to $6.60 million) and a lengthening in accounts receivable aging (>120 days doubling to $5.67 million) indicate residual friction in legacy industrial segments, the underlying transition toward Aerospace and Specialist Technologies is intact. If Bodycote successfully leverages its exclusive processes (Nivox® for nuclear, HVOF replacing toxic hexavalent chrome in aviation) to capture just a fraction of the migrating in-house OEM capacity, management’s aggressive target of >20% adjusted operating margins by 2028 is highly credible.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research (www.hdinresearch.com) is a premier global provider of institutional market intelligence, specializing in deep-dive corporate governance, financial forensics, and strategic supply chain analysis.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Pricing Power Amidst Margin Compression

Bodycote’s FY2025 financial disclosures reveal a stark bifurcation in end-market dynamics. While total revenue contracted 4.0% to $959.19 million, effectively masking the underlying strength of the enterprise, a deeper forensic analysis indicates highly deliberate portfolio pruning.

Faced with severe cyclical headwinds and low asset utilization in the Automotive & General Industrial (AGI) sectors, Bodycote experienced friction in its cost-pass-through mechanisms. Utility costs edged up to $92.74 million despite a 4.2% drop in energy consumption, leading to a headline operating margin contraction to 15.7%. Rather than absorb this structural inefficiency, management initiated its "Optimise" restructuring program—aggressively divesting 10 non-core, automotive-heavy facilities in France for $25.46 million and retiring older, carbon-intensive assets.

This short-term top-line sacrifice fundamentally hardens the company's economic moat. By retaining a highly defensive balance sheet (Net Debt/EBITDA of just 0.6x) and clearing legacy impairments, Bodycote successfully maintained its 30.34 US cents per share dividend and initiated a new $105.54 million share buyback extending to 2027. Furthermore, the bolt-on accretive acquisition of Spectrum Thermal Processing in Rhode Island immediately captures high-margin, Nadcap-accredited market share in the US aerospace sector, effectively trading low-margin European automotive revenue for highly defensible A&D yield.

Figure Bodycote plc 2025 Strategic Executive Summary

Nearshoring and the "Zero-Emission" PremiumThe 2026–2027 operational outlook hinges on capitalizing on regional supply chain shifts and stringent decarbonization mandates. Bodycote is explicitly aligning its asset base to intersect with OEM nearshoring and vertical disintegration trends.

Key capital allocation targets include:

* Capacity Expansion in Peak-Utilization Nodes: A&D supply chain constraints have materially improved, triggering a surge in throughput. Bodycote is funding major US capacity upgrades, including Hot Isostatic Pressing (HIP) expansions, and utilizing lean manufacturing processes that recently saved 500 square feet of floor space at its Cincinnati aerospace site.

* Emerging Market Greenfield Deployment: The firm is deploying its proprietary Specialty Stainless Steel Processes (S³P) into the Asian market via a new greenfield facility (commissioning late 2026/early 2027), addressing the stark disparity where Emerging Markets currently represent only $9.50 million of Specialist Technologies revenue.

* Nearshoring via Mexico: A new greenfield site in Mexico is slated to capture North American automotive and industrial supply chain re-alignment, generating meaningful revenue by 2027.

Crucially, Bodycote has weaponized ESG compliance as a commercial lever. The company stress-tested an internal carbon price of $131.92/tonne. With the looming threat of cross-border carbon mechanisms (e.g., CBAM), OEMs operating inefficient in-house furnaces face massive compliance liabilities. Bodycote’s deployment of 100% electrified, zero-emission pathfinder plants in Derby and Rotherham allows OEMs to outsource their thermal processing and instantly reduce component carbon footprints by up to 60%, fully backed by Bureau Veritas-verified product carbon footprint data.

HDIN Institutional Perspective: The In-House TAM Unlock

The street is mispricing Bodycote as a pure-play industrial cyclical. HDIN Research views the FY2025 data not as a signal of deterioration, but as the trough of a deliberate transition cycle. The true alpha lies in the ~80% of the $39.58 billion global thermal processing market that remains in-house.

As energy price volatility threatens the viability of captive OEM furnaces, the capital hurdle for OEMs to upgrade legacy equipment to meet Scope 1 and 2 emissions mandates becomes prohibitive. This environment accelerates the transition from in-house processing to outsourced specialist partners. Bodycote’s integration of Emmanuelle Dubu—a seasoned metallurgist and former manufacturing CEO—onto its Board signals a tightened grip on advanced technical governance.

While a buildup in Work-in-Progress (WIP) inventory (spiking 72% to $6.60 million) and a lengthening in accounts receivable aging (>120 days doubling to $5.67 million) indicate residual friction in legacy industrial segments, the underlying transition toward Aerospace and Specialist Technologies is intact. If Bodycote successfully leverages its exclusive processes (Nivox® for nuclear, HVOF replacing toxic hexavalent chrome in aviation) to capture just a fraction of the migrating in-house OEM capacity, management’s aggressive target of >20% adjusted operating margins by 2028 is highly credible.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research (www.hdinresearch.com) is a premier global provider of institutional market intelligence, specializing in deep-dive corporate governance, financial forensics, and strategic supply chain analysis.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.