Pop Mart (HKG: 9992) Pivots to Plush Collectibles as Proprietary IP Matrix Drives 184.7% Revenue Surge in FY2025 Audit

Date : 2026-04-24

Reading : 175

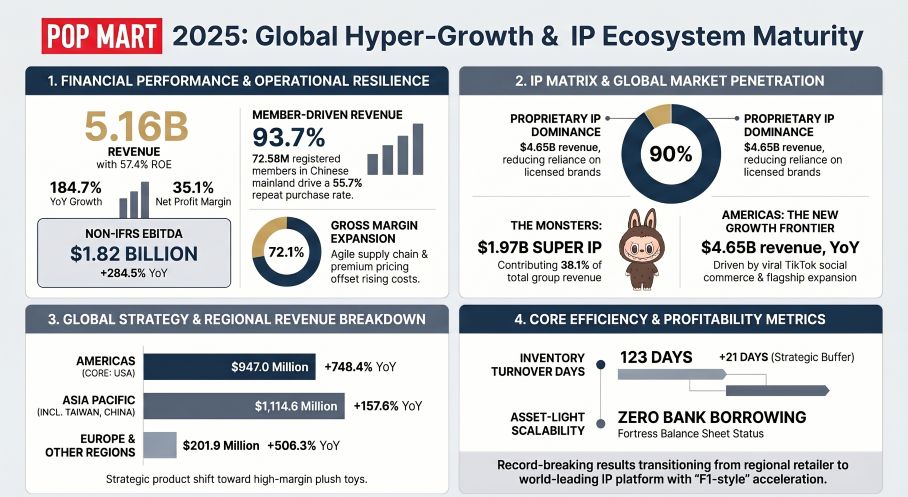

In its audited FY2025 results, Pop Mart International Group (HKG: 9992) reported an unprecedented $5.16 billion (RMB 37.12 billion) in global revenue, marking a 184.7% year-over-year surge. The Beijing-headquartered cultural entertainment enterprise successfully pivoted from traditional hard-plastic figurines to high-margin interactive plush toys, leveraging the viral global dominance of its proprietary THE MONSTERS IP. This hyper-growth was distinctly catalyzed by a 748.4% revenue explosion in the Americas, heavily driven by cross-border TikTok commerce, establishing a formidable global footprint that fundamentally redefines the lifecycle economics of the collectible toy sector.

Financial Health & Operational Moats: Defying Sector-Wide Margin Compression

While the broader discretionary consumer sector grapples with stagnant pricing power, Pop Mart demonstrated an exceptional ability to execute cost-pass-through mechanisms. Gross margins expanded by 5.3 percentage points to 72.1%, driving a Non-IFRS adjusted net profit of $1.82 billion (+284.5% YoY) and an astronomical 57.4% Return on Equity (ROE).

This margin expansion is not an accounting artifact but a structural byproduct of two strategic moats. First, a deliberate geographic revenue mix shift: overseas markets, which inherently command higher retail price points, grew to account for 43.8% of total revenue. Second, a fundamental category pivot. Plush toys bypassed traditional blind boxes to become the dominant revenue engine, generating $2.60 billion (50.4% of total group revenue). By heavily monetizing the LABUBU character via plush formats, Pop Mart drastically enhanced daily consumer utility and emotional stickiness, insulating the brand from the traditional "fad decay" curve of rigid art collectibles.

Furthermore, capital allocation in FY2025 was highly disciplined. The company utilized its pristine balance sheet (holding $2.39 billion in cash equivalents with zero bank borrowings) to execute a series of accretive acquisitions, buying out minority stakes in key joint ventures across Singapore (Pop Mart South Asia Pte. Ltd. for SGD 20.0 million), Japan, and Thailand. Crucially, these consolidation moves triggered zero goodwill impairment, underscoring the intrinsic cash-generating capability of its localized retail assets.

Figure POP MART 2025: Global Hyper-Growth & lP Ecosystem Maturity

Supply Chain Pivot: Managing Global Freight Volatility

Supply Chain Pivot: Managing Global Freight Volatility

Pop Mart’s supply chain infrastructure is undergoing a stress test induced by its own hyper-growth. The company actively rejects vertical integration, operating a 100% outsourced manufacturing model via selected third-party factories. While this maintains an asset-light production base, the aggressive expansion of 109 net new global retail stores required a massive structural inventory buffering.

Inventories surged 259.0% to $761.4 million, extending turnover days from 102 to 123. Concurrently, transportation and logistics expenses skyrocketed 280.3% to $247.4 million. This indicates a delayed near-term inventory de-stocking cycle; the company is absorbing higher trans-pacific freight premiums and extending lead times to ensure uninterrupted supply for its booming Direct-to-Consumer (DTC) channels in the Americas (which saw online sales surge 1,094.9%). While inventory impairment provisions remain negligible at 0.39% ($2.95 million), this ballooning working capital requirement represents a latent cyclical risk if IP engagement unexpectedly cools.

To mitigate regulatory headwinds and chemical safety risks in these new territories, Pop Mart deployed a rigorous "design for compliance" protocol. The phase-out of polycarbonate (PC) plastics in favor of BPA-free PCT-G, alongside achieving 100% FSC-certified packaging, ensures seamless penetration into stringent regulatory environments like the EU (REACH) and California (Proposition 65).

HDIN Institutional Perspective: The "Pit Lane" Consolidation of 2026

A critical signal for institutional investors lies in management’s forward guidance. Chairman Wang Ning explicitly characterized 2026 as a year to "pause in the pit lane to refuel and replace tyres."

This language marks a structural peak in Pop Mart's "F1-style" land-grab phase. For the sector at large, this signals a transition from hyper-growth distribution rollouts to mature IP holding-company economics (akin to early-stage Sanrio or Disney). Future CAPEX will be heavily redirected from raw physical retail expansion toward deeper ecosystem extraction. We anticipate significant capital deployment into global supply chain automation, AI-driven digital CRM infrastructure (managing its 72.58 million registered mainland members), and the physical capacity upgrade of the POP LAND theme park in Beijing.

Pop Mart is no longer just a blind-box retailer; it is a proprietary IP oligopoly. By restricting third-party licensed IP revenue to a mere 9.1% and maintaining absolute control over the commercialization rights of "One Dominant, Multiple Strong" artist IPs, Pop Mart has constructed a resilient global cultural ecosystem capable of withstanding macroeconomic cyclicality.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in cross-border strategic analysis, corporate financial forensics, and macroeconomic sector trends. For deeper industry insights, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Health & Operational Moats: Defying Sector-Wide Margin Compression

While the broader discretionary consumer sector grapples with stagnant pricing power, Pop Mart demonstrated an exceptional ability to execute cost-pass-through mechanisms. Gross margins expanded by 5.3 percentage points to 72.1%, driving a Non-IFRS adjusted net profit of $1.82 billion (+284.5% YoY) and an astronomical 57.4% Return on Equity (ROE).

This margin expansion is not an accounting artifact but a structural byproduct of two strategic moats. First, a deliberate geographic revenue mix shift: overseas markets, which inherently command higher retail price points, grew to account for 43.8% of total revenue. Second, a fundamental category pivot. Plush toys bypassed traditional blind boxes to become the dominant revenue engine, generating $2.60 billion (50.4% of total group revenue). By heavily monetizing the LABUBU character via plush formats, Pop Mart drastically enhanced daily consumer utility and emotional stickiness, insulating the brand from the traditional "fad decay" curve of rigid art collectibles.

Furthermore, capital allocation in FY2025 was highly disciplined. The company utilized its pristine balance sheet (holding $2.39 billion in cash equivalents with zero bank borrowings) to execute a series of accretive acquisitions, buying out minority stakes in key joint ventures across Singapore (Pop Mart South Asia Pte. Ltd. for SGD 20.0 million), Japan, and Thailand. Crucially, these consolidation moves triggered zero goodwill impairment, underscoring the intrinsic cash-generating capability of its localized retail assets.

Figure POP MART 2025: Global Hyper-Growth & lP Ecosystem Maturity

Supply Chain Pivot: Managing Global Freight VolatilityPop Mart’s supply chain infrastructure is undergoing a stress test induced by its own hyper-growth. The company actively rejects vertical integration, operating a 100% outsourced manufacturing model via selected third-party factories. While this maintains an asset-light production base, the aggressive expansion of 109 net new global retail stores required a massive structural inventory buffering.

Inventories surged 259.0% to $761.4 million, extending turnover days from 102 to 123. Concurrently, transportation and logistics expenses skyrocketed 280.3% to $247.4 million. This indicates a delayed near-term inventory de-stocking cycle; the company is absorbing higher trans-pacific freight premiums and extending lead times to ensure uninterrupted supply for its booming Direct-to-Consumer (DTC) channels in the Americas (which saw online sales surge 1,094.9%). While inventory impairment provisions remain negligible at 0.39% ($2.95 million), this ballooning working capital requirement represents a latent cyclical risk if IP engagement unexpectedly cools.

To mitigate regulatory headwinds and chemical safety risks in these new territories, Pop Mart deployed a rigorous "design for compliance" protocol. The phase-out of polycarbonate (PC) plastics in favor of BPA-free PCT-G, alongside achieving 100% FSC-certified packaging, ensures seamless penetration into stringent regulatory environments like the EU (REACH) and California (Proposition 65).

HDIN Institutional Perspective: The "Pit Lane" Consolidation of 2026

A critical signal for institutional investors lies in management’s forward guidance. Chairman Wang Ning explicitly characterized 2026 as a year to "pause in the pit lane to refuel and replace tyres."

This language marks a structural peak in Pop Mart's "F1-style" land-grab phase. For the sector at large, this signals a transition from hyper-growth distribution rollouts to mature IP holding-company economics (akin to early-stage Sanrio or Disney). Future CAPEX will be heavily redirected from raw physical retail expansion toward deeper ecosystem extraction. We anticipate significant capital deployment into global supply chain automation, AI-driven digital CRM infrastructure (managing its 72.58 million registered mainland members), and the physical capacity upgrade of the POP LAND theme park in Beijing.

Pop Mart is no longer just a blind-box retailer; it is a proprietary IP oligopoly. By restricting third-party licensed IP revenue to a mere 9.1% and maintaining absolute control over the commercialization rights of "One Dominant, Multiple Strong" artist IPs, Pop Mart has constructed a resilient global cultural ecosystem capable of withstanding macroeconomic cyclicality.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier provider of institutional-grade market intelligence, specializing in cross-border strategic analysis, corporate financial forensics, and macroeconomic sector trends. For deeper industry insights, visit www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*