Ophthalmic Giants See Diverging Margins: Alcon and J&J Consolidate Surgical Moats Amid Severe Bausch + Lomb Margin Compression

Date : 2026-04-24

Reading : 587

Following a forensic audit of FY2025 corporate filings, HDIN Research reveals that the top four eyecare manufacturers—Johnson & Johnson (NYSE: JNJ), Alcon (NYSE: ALC), CooperCompanies (NYSE: COO), and Bausch + Lomb (NYSE: BLCO)—generated over $10.4 billion in combined contact lens revenue. While EMEA drove baseline volume through Silicone Hydrogel (SiHy) adoption, severe structural margin compression and retail consolidation have sharply bifurcated the sector. J&J and Alcon are leveraging advanced surgical installed bases to defend pricing power, while highly leveraged pure-plays face liquidity crises heading into FY2026.

Financial Health & Operational Moats: The Solvency Bifurcation

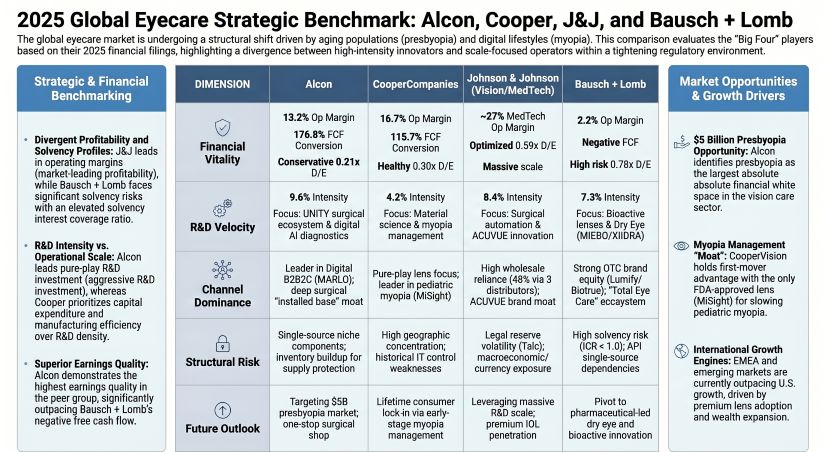

A rigorous deconstruction of core earnings across the cohort exposes a stark hierarchy in operational yields and cash flow generation. The prevailing industry narrative focuses on top-line growth driven by the $5 billion presbyopia total addressable market, but the balance sheets dictate a reality of aggressive cost-pass-through mechanisms separating the fortified from the vulnerable.

Johnson & Johnson commands a sector-leading 27.1% operating margin, insulated by the sheer scale of its $94.19 billion diversified portfolio. However, earnings quality demands scrutiny: JNJ’s FY2025 net income was heavily distorted by a $7.0 billion non-cash reversal of previously accrued talc litigation reserves. Stripping out this anomaly, JNJ’s underlying 73.5% Free Cash Flow (FCF) conversion remains robust, funding a massive $14.7 billion total R&D budget that effectively immunizes its MedTech Vision franchise from localized macroeconomic shocks.

Conversely, Bausch + Lomb acts as the sector’s distressed canary. Burdened by a 0.27x Interest Coverage Ratio (ICR) and a $5.08 billion debt load, BLCO posted an operating margin of merely 2.2% and a negative FCF of $(66) million. The firm is suffering from acute margin compression driven by an inability to execute cost-pass-through mechanisms against consolidating retail channels and aggressive gross-to-net pricing deductions (representing 39.5% of gross product sales).

Between these extremes, Alcon generated an exceptional 176.8% FCF conversion rate ($1.73 billion). Alcon’s 13.2% operating margin is structurally defended by its surgical installed base (e.g., Centurion and Unity CS consoles), which operates as an anchoring moat to drive high-margin, recurring consumable pull-through.

Figure 2025 Global Eyecare Strategic Benchmark: Alcon, Cooper, J&J, and Bausch + Lomb

Supply Chain Pivot: "Local-for-Local" Capacity Realignment

Supply Chain Pivot: "Local-for-Local" Capacity Realignment

To mitigate exposure to reciprocating tariffs, supply chain vulnerabilities, and the volatile reliance on single-source third-party silicone macromer suppliers, the sector is aggressively pivoting toward "local-for-local" vertical integration and capacity regionalization.

Rather than injecting M&A capital into contact lens acquisitions, manufacturers are deploying intensive CAPEX into physical footprints to front-run inventory de-stocking risks:

* Alcon committed over $276 million in PPE, executing a $162 million expansion at its Grosswallstadt, Germany facility (targeting 2027 completion) and a $220 million build-out in Johns Creek, Georgia (completion 2028/2029) to internalize SiHy manufacturing.

* Bausch + Lomb deployed a targeted $75 million upfront cash payment to acquire manufacturing equipment and assume a facility lease in Mexico, desperately attempting to unlock regional capacity and repair its fractured cost structure.

* The Cooper Companies, which exhibited the slowest inventory turnover cycle at ~219 days, directed $362.4 million in CAPEX globally, heavily committing to automated distribution hubs in Puerto Rico and Costa Rica to manage its sprawling SKU portfolio.

R&D Intensity & Accretive Acquisitions

Strategic capital allocation in FY2025 highlighted a fundamental divergence in innovation betting. M&A capital was entirely diverted away from the contact lens space, focusing instead on accretive acquisitions in clinical-stage therapeutics.

Alcon (leading pure-play R&D intensity at 9.6%) deployed $486 million to acquire a 99% stake in Aurion Biotech and $124 million for LumiThera. These maneuvers aim to capture the regenerative medicine and dry AMD markets, building a "Total Eye Care" ecosystem.

Alternatively, CooperCompanies (lowest R&D intensity at 4.2%) proved that hyper-elevated R&D is not a prerequisite for niche dominance. Cooper relies on its structural first-mover advantage with the *MiSight 1 day* lens—the sole FDA, NMPA, and MHLW-approved pediatric myopia management lens—locking in a lifetime consumer base from age 8 without the capital drag of surgical hardware development.

HDIN Institutional Perspective

The 2026 ophthalmic outlook is defined by a hard ceiling on standard corrective technologies. As e-commerce and Direct-to-Consumer (DTC) channels cannibalize traditional B2B Optometrist networks, pure vision correction is facing rapid commoditization.

We view Bausch + Lomb's structural distress as indicative of a broader cyclical trough for mid-tier optical hardware lacking surgical or pharmaceutical integration. To survive the margin compression inherent to the current retail environment, manufacturers must transition patients to premium modalities (e.g., Alcon's DAILIES TOTAL1 or Cooper's MyDay) while aggressively automating production to lower the cost of goods sold. The true alpha in this $37 billion market will not be generated by volume growth in spherical lenses, but by locking hospital networks into proprietary digital surgical ecosystems and capitalizing on the therapeutic pivot toward pediatric myopia control.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier independent strategic intelligence and equity research firm. We specialize in forensic financial auditing, supply chain deconstruction, and deep-tier market modeling to provide institutional investors with actionable, data-driven conviction. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."

Financial Health & Operational Moats: The Solvency Bifurcation

A rigorous deconstruction of core earnings across the cohort exposes a stark hierarchy in operational yields and cash flow generation. The prevailing industry narrative focuses on top-line growth driven by the $5 billion presbyopia total addressable market, but the balance sheets dictate a reality of aggressive cost-pass-through mechanisms separating the fortified from the vulnerable.

Johnson & Johnson commands a sector-leading 27.1% operating margin, insulated by the sheer scale of its $94.19 billion diversified portfolio. However, earnings quality demands scrutiny: JNJ’s FY2025 net income was heavily distorted by a $7.0 billion non-cash reversal of previously accrued talc litigation reserves. Stripping out this anomaly, JNJ’s underlying 73.5% Free Cash Flow (FCF) conversion remains robust, funding a massive $14.7 billion total R&D budget that effectively immunizes its MedTech Vision franchise from localized macroeconomic shocks.

Conversely, Bausch + Lomb acts as the sector’s distressed canary. Burdened by a 0.27x Interest Coverage Ratio (ICR) and a $5.08 billion debt load, BLCO posted an operating margin of merely 2.2% and a negative FCF of $(66) million. The firm is suffering from acute margin compression driven by an inability to execute cost-pass-through mechanisms against consolidating retail channels and aggressive gross-to-net pricing deductions (representing 39.5% of gross product sales).

Between these extremes, Alcon generated an exceptional 176.8% FCF conversion rate ($1.73 billion). Alcon’s 13.2% operating margin is structurally defended by its surgical installed base (e.g., Centurion and Unity CS consoles), which operates as an anchoring moat to drive high-margin, recurring consumable pull-through.

Figure 2025 Global Eyecare Strategic Benchmark: Alcon, Cooper, J&J, and Bausch + Lomb

Supply Chain Pivot: "Local-for-Local" Capacity Realignment To mitigate exposure to reciprocating tariffs, supply chain vulnerabilities, and the volatile reliance on single-source third-party silicone macromer suppliers, the sector is aggressively pivoting toward "local-for-local" vertical integration and capacity regionalization.

Rather than injecting M&A capital into contact lens acquisitions, manufacturers are deploying intensive CAPEX into physical footprints to front-run inventory de-stocking risks:

* Alcon committed over $276 million in PPE, executing a $162 million expansion at its Grosswallstadt, Germany facility (targeting 2027 completion) and a $220 million build-out in Johns Creek, Georgia (completion 2028/2029) to internalize SiHy manufacturing.

* Bausch + Lomb deployed a targeted $75 million upfront cash payment to acquire manufacturing equipment and assume a facility lease in Mexico, desperately attempting to unlock regional capacity and repair its fractured cost structure.

* The Cooper Companies, which exhibited the slowest inventory turnover cycle at ~219 days, directed $362.4 million in CAPEX globally, heavily committing to automated distribution hubs in Puerto Rico and Costa Rica to manage its sprawling SKU portfolio.

R&D Intensity & Accretive Acquisitions

Strategic capital allocation in FY2025 highlighted a fundamental divergence in innovation betting. M&A capital was entirely diverted away from the contact lens space, focusing instead on accretive acquisitions in clinical-stage therapeutics.

Alcon (leading pure-play R&D intensity at 9.6%) deployed $486 million to acquire a 99% stake in Aurion Biotech and $124 million for LumiThera. These maneuvers aim to capture the regenerative medicine and dry AMD markets, building a "Total Eye Care" ecosystem.

Alternatively, CooperCompanies (lowest R&D intensity at 4.2%) proved that hyper-elevated R&D is not a prerequisite for niche dominance. Cooper relies on its structural first-mover advantage with the *MiSight 1 day* lens—the sole FDA, NMPA, and MHLW-approved pediatric myopia management lens—locking in a lifetime consumer base from age 8 without the capital drag of surgical hardware development.

HDIN Institutional Perspective

The 2026 ophthalmic outlook is defined by a hard ceiling on standard corrective technologies. As e-commerce and Direct-to-Consumer (DTC) channels cannibalize traditional B2B Optometrist networks, pure vision correction is facing rapid commoditization.

We view Bausch + Lomb's structural distress as indicative of a broader cyclical trough for mid-tier optical hardware lacking surgical or pharmaceutical integration. To survive the margin compression inherent to the current retail environment, manufacturers must transition patients to premium modalities (e.g., Alcon's DAILIES TOTAL1 or Cooper's MyDay) while aggressively automating production to lower the cost of goods sold. The true alpha in this $37 billion market will not be generated by volume growth in spherical lenses, but by locking hospital networks into proprietary digital surgical ecosystems and capitalizing on the therapeutic pivot toward pediatric myopia control.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under "Related Topics" to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research

HDIN Research is a premier independent strategic intelligence and equity research firm. We specialize in forensic financial auditing, supply chain deconstruction, and deep-tier market modeling to provide institutional investors with actionable, data-driven conviction. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."