Cardiovascular MedTech Giants See Diverging Margins: Boston Scientific and Edwards Lifesciences Execute $18B in Accretive M&A Amid Aggressive Asian Import Substitution

Date : 2026-04-24

Reading : 300

In FY2025, global cardiovascular device manufacturers initiated a brutal cycle of portfolio rationalization, responding to deep margin compression driven by China’s Volume-Based Procurement (VBP) and systemic EU Medical Device Regulation (MDR) bottlenecks. While Medtronic (NYSE: MDT) and Abbott (NYSE: ABT) battle $350 million localized tariff headwinds, Boston Scientific (NYSE: BSX) and Edwards Lifesciences (NYSE: EW) have deployed over $18 billion in accretive acquisitions to monopolize high-margin Pulsed Field Ablation (PFA) and structural heart arenas. Simultaneously, Chinese regional mid-caps are deploying aggressive capital expenditures to bypass domestic pricing caps, establishing Sino-European manufacturing loops ahead of 2026.

Financial Health & Operational Moats: The Cost of Category Monopolies

A forensic audit of FY2025 10-K and annual filings reveals a stark bifurcation in quality of earnings and capital allocation between diversified legacy conglomerates and structural "pure-plays."

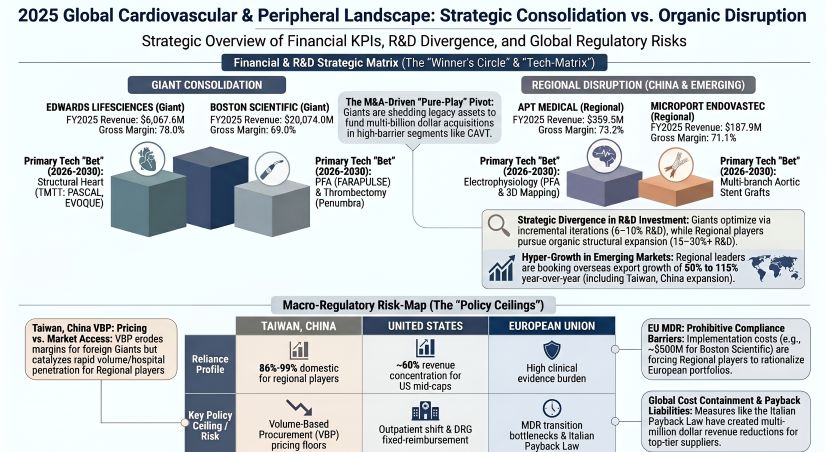

Edwards Lifesciences (NYSE: EW) stands as a stark outlier in operational moats. By deliberately running a massive 17.8% R&D intensity ($1.079 billion), the firm effectively operates with biotech-level capital dynamics. The "so what" for institutional investors is clear: this is not incremental lifecycle management. This capital deployment drove a 56.4% revenue surge in Transcatheter Mitral and Tricuspid Therapies (TMTT), anchored by the EVOQUE and PASCAL systems, successfully locking in a 78.0% gross margin. To fund this, Edwards executed textbook portfolio rationalization, divesting its $4.2 billion Critical Care unit to Becton Dickinson, cementing an impenetrable IP fortress around structural heart procedures.

Conversely, Boston Scientific (NYSE: BSX) relies on external capital deployment to defend against commoditization. With a tightly controlled 10.2% organic R&D intensity, BSX utilized its pristine 1.57x Operating Cash Flow-to-Net Income ratio to swallow Penumbra (NYSE: PEN) in a $14.5 billion mega-merger. This accretive acquisition immediately grants BSX dominance in Computer Assisted Vacuum Thrombectomy (CAVT)—neutralizing competitors in the ischemic stroke and pulmonary embolism markets while supplementing the explosive $3.3 billion revenue generated by its FARAPULSE PFA system.

Down the capitalization ladder, solvency metrics expose critical vulnerabilities. Teleflex (NYSE: TFX) exhibits severe financial strain with a 0.85x Debt-to-Equity ratio and a razor-thin 1.18x interest coverage multiple, compounded by a $964.1 million loss from discontinued operations. Similarly, Artivion (NYSE: AORT) is masking operational inefficiencies through bloated working capital; the firm accumulated $54.5 million in highly subjective "Deferred Preservation Costs" for biologic tissues, a red flag for impending inventory write-downs should procedural demand soften.

Figure 2025 Global Cardiovascular & Peripheral Landscape Strategic Consolidation vs Organic Disruption

Supply Chain Pivot: Tariffs, VBP, and the Sino-European Realignment

Supply Chain Pivot: Tariffs, VBP, and the Sino-European Realignment

Geopolitical friction and regional cost-containment mandates are fundamentally rewriting cardiovascular supply chains. In Asia, China's centralized Volume-Based Procurement (VBP) is no longer a localized risk; it has catalyzed a massive manufacturing arms race.

Instead of absorbing margin decay, top-tier Chinese regional players are utilizing strict cost-pass-through mechanisms and backward vertical integration to trade price for sheer volume. APT Medical (HKEX: 6696) maintained a formidable 73.2% gross margin despite VBP, backed by a CNY 137.8 million CAPEX deployment into an automated Smart Manufacturing Center.

More critically, to hedge against future US-Sino trade decoupling—which Medtronic explicitly modeled in its 10-K as a $200 million to $350 million net tariff exposure for FY2026—Chinese mid-caps are securing foreign beachheads. Zylox-Tonbridge (HKEX: 2190) announced the strategic acquisition of Germany's Optimed in early 2026. This allows the firm to bypass EU MDR Notified Body bottlenecks and establish a "China R&D + Sino-German Manufacturing" loop, shielding its high-growth peripheral drug-coated balloon (DCB) portfolios from sovereign tariff retaliation. Meanwhile, Penumbra is hedging stateside manufacturing reliance by deploying a $58 million CAPEX allocation to a dedicated facility in Costa Rica, targeting strict supply chain continuity for its Lightning Flash 3.0 algorithms.

HDIN Institutional Perspective: The Commoditization Trough and the PFA Super-Cycle

The cardiovascular sector is exiting a prolonged cyclical trough in baseline stenting and entering a hyper-concentrated technological super-cycle. The era of competing on incremental delivery system tweaks is over. The $46 million intangible asset impairment BSX recorded on its legacy Cryterion cryoablation platforms signals the permanent obsolescence of thermal ablation, entirely cannibalized by the PFA paradigm shift.

Furthermore, global macro-ceilings, such as the Italian Constitutional Court upholding the Payback Law—which forced a $90 million localized revenue reduction for Medtronic and widespread reserve adjustments for Teleflex—will force aggressive inventory de-stocking across Western Europe throughout 2026.

We view the current ecosystem as highly hostile to mid-cap entities lacking category-defining clinical data. Firms reliant on basic percutaneous coronary intervention (PCI) consumables will suffer relentless margin compression. The undeniable strategic imperative for 2026–2030 requires abandoning generalist hardware portfolios to command closed-loop, high-switching-cost ecosystems, exemplified by Medtronic’s AiBLE spinal robotics or Sinomed's FDA-approved HT Supreme healing-targeted regimens.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier independent strategic advisory and financial intelligence firm. Our primary research models focus on forensic auditing of corporate disclosures, supply chain realignment, and geopolitical macro-analysis across global markets. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Health & Operational Moats: The Cost of Category Monopolies

A forensic audit of FY2025 10-K and annual filings reveals a stark bifurcation in quality of earnings and capital allocation between diversified legacy conglomerates and structural "pure-plays."

Edwards Lifesciences (NYSE: EW) stands as a stark outlier in operational moats. By deliberately running a massive 17.8% R&D intensity ($1.079 billion), the firm effectively operates with biotech-level capital dynamics. The "so what" for institutional investors is clear: this is not incremental lifecycle management. This capital deployment drove a 56.4% revenue surge in Transcatheter Mitral and Tricuspid Therapies (TMTT), anchored by the EVOQUE and PASCAL systems, successfully locking in a 78.0% gross margin. To fund this, Edwards executed textbook portfolio rationalization, divesting its $4.2 billion Critical Care unit to Becton Dickinson, cementing an impenetrable IP fortress around structural heart procedures.

Conversely, Boston Scientific (NYSE: BSX) relies on external capital deployment to defend against commoditization. With a tightly controlled 10.2% organic R&D intensity, BSX utilized its pristine 1.57x Operating Cash Flow-to-Net Income ratio to swallow Penumbra (NYSE: PEN) in a $14.5 billion mega-merger. This accretive acquisition immediately grants BSX dominance in Computer Assisted Vacuum Thrombectomy (CAVT)—neutralizing competitors in the ischemic stroke and pulmonary embolism markets while supplementing the explosive $3.3 billion revenue generated by its FARAPULSE PFA system.

Down the capitalization ladder, solvency metrics expose critical vulnerabilities. Teleflex (NYSE: TFX) exhibits severe financial strain with a 0.85x Debt-to-Equity ratio and a razor-thin 1.18x interest coverage multiple, compounded by a $964.1 million loss from discontinued operations. Similarly, Artivion (NYSE: AORT) is masking operational inefficiencies through bloated working capital; the firm accumulated $54.5 million in highly subjective "Deferred Preservation Costs" for biologic tissues, a red flag for impending inventory write-downs should procedural demand soften.

Figure 2025 Global Cardiovascular & Peripheral Landscape Strategic Consolidation vs Organic Disruption

Supply Chain Pivot: Tariffs, VBP, and the Sino-European RealignmentGeopolitical friction and regional cost-containment mandates are fundamentally rewriting cardiovascular supply chains. In Asia, China's centralized Volume-Based Procurement (VBP) is no longer a localized risk; it has catalyzed a massive manufacturing arms race.

Instead of absorbing margin decay, top-tier Chinese regional players are utilizing strict cost-pass-through mechanisms and backward vertical integration to trade price for sheer volume. APT Medical (HKEX: 6696) maintained a formidable 73.2% gross margin despite VBP, backed by a CNY 137.8 million CAPEX deployment into an automated Smart Manufacturing Center.

More critically, to hedge against future US-Sino trade decoupling—which Medtronic explicitly modeled in its 10-K as a $200 million to $350 million net tariff exposure for FY2026—Chinese mid-caps are securing foreign beachheads. Zylox-Tonbridge (HKEX: 2190) announced the strategic acquisition of Germany's Optimed in early 2026. This allows the firm to bypass EU MDR Notified Body bottlenecks and establish a "China R&D + Sino-German Manufacturing" loop, shielding its high-growth peripheral drug-coated balloon (DCB) portfolios from sovereign tariff retaliation. Meanwhile, Penumbra is hedging stateside manufacturing reliance by deploying a $58 million CAPEX allocation to a dedicated facility in Costa Rica, targeting strict supply chain continuity for its Lightning Flash 3.0 algorithms.

HDIN Institutional Perspective: The Commoditization Trough and the PFA Super-Cycle

The cardiovascular sector is exiting a prolonged cyclical trough in baseline stenting and entering a hyper-concentrated technological super-cycle. The era of competing on incremental delivery system tweaks is over. The $46 million intangible asset impairment BSX recorded on its legacy Cryterion cryoablation platforms signals the permanent obsolescence of thermal ablation, entirely cannibalized by the PFA paradigm shift.

Furthermore, global macro-ceilings, such as the Italian Constitutional Court upholding the Payback Law—which forced a $90 million localized revenue reduction for Medtronic and widespread reserve adjustments for Teleflex—will force aggressive inventory de-stocking across Western Europe throughout 2026.

We view the current ecosystem as highly hostile to mid-cap entities lacking category-defining clinical data. Firms reliant on basic percutaneous coronary intervention (PCI) consumables will suffer relentless margin compression. The undeniable strategic imperative for 2026–2030 requires abandoning generalist hardware portfolios to command closed-loop, high-switching-cost ecosystems, exemplified by Medtronic’s AiBLE spinal robotics or Sinomed's FDA-approved HT Supreme healing-targeted regimens.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research is a premier independent strategic advisory and financial intelligence firm. Our primary research models focus on forensic auditing of corporate disclosures, supply chain realignment, and geopolitical macro-analysis across global markets. (www.hdinresearch.com)

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.