Zhongji Innolight Executes $517M TeraHop Expansion as 101% FCF Conversion Signals Margin Immunity to Geopolitical Tariffs

Date : 2026-04-27

Reading : 1812

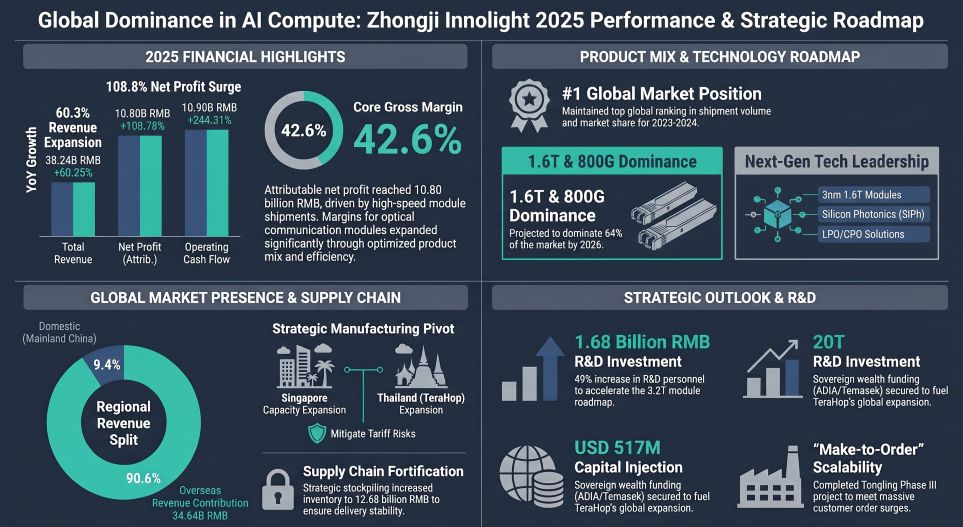

Zhongji Innolight (SZSE: 300308) has effectively insulated its 10.80 billion RMB profit engine from US-China trade friction by capitalizing its Singapore and Thailand-based TeraHop subsidiary with a $517 million injection backed by ADIA and Temasek. Driven by tier-1 CSP demand for 800G and 1.6T optical modules, overseas markets now account for 90.58% of total revenue. This strategic relocation to zero-tax Thai jurisdictions outmaneuvers tariff constraints while securing the manufacturing supply chain for the explosive global AI compute cycle.

Operating Leverage and Pristine Cash Economics

Beyond the top-line revenue beat of 38.24 billion RMB (+60.25% YoY), SZSE: 300308 is demonstrating textbook operating leverage. Net profit attributable to shareholders surged 108.78% to 10.80 billion RMB, driven by a highly favorable price-mix variance as AI data center topologies shift aggressively toward 800G and 1.6T architectures. This product-mix optimization expanded the core optical communication module gross margin by nearly 800 basis points, from 34.65% to 42.61% on 21.09 million units sold.

The true quality of these earnings is validated by the unit’s cash economics. Operating Cash Flow (OCF) skyrocketed by 244.31% to 10.90 billion RMB, translating to a 101% cash conversion ratio. This 1-to-1 conversion confirms that the hyper-growth trajectory is underwritten by actual cash collections from tier-1 Cloud Service Providers (CSPs), not aggressive revenue recognition. R&D-to-Moat translation is equally disciplined: despite allocating 1.676 billion RMB to advance Silicon Photonics (SiPh) and Linear Drive Pluggable Optics (LPO) architectures, management capitalized a mere 3.62% of this expenditure, keeping the balance sheet unburdened by inflated intangible assets. The firm’s capital structure remains fortress-like, with 10.98 billion RMB in liquid monetary funds dwarfing a negligible 811 million RMB in combined short and long-term borrowings.

Figure Global Dominance in Al Compute: Zhongji lnnolight 2025 Performance & Strategic Roadmap

Tactical Stockpiling vs. Geographic Arbitrage

Tactical Stockpiling vs. Geographic Arbitrage

To digest the exponential growth in global AI token consumption, SZSE: 300308 triggered a massive internal capital allocation shift. Construction in Progress (CIP) expanded from 52.53 million RMB to 1.42 billion RMB, punctuated by the completion of the domestic Tongling Innolight High-end Optical Module Industrial Park Phase III.

However, the company’s structural moat increasingly relies on offshore geographic arbitrage. The rapid scaling of TeraHop Pte. Ltd.—which generated 2.38 billion RMB in net profit and now holds 23.54 billion RMB in assets—provides a dual advantage: tariff circumvention and tax optimization. Operating under Singapore’s DEI framework (10% tax) and Thailand’s Board of Investment incentives (0% tax), the overseas network inherently structurally lifts the consolidated bottom line.

Operationally, the balance sheet reveals aggressive defensive stockpiling. Inventory balances swelled by 80% to 12.68 billion RMB (28.00% of total assets), with raw materials doubling to 4.60 billion RMB. Crucially, the inventory impairment provision remained flat at 297.82 million RMB. This divergence confirms that the working capital build is a strict "make-to-order" hedge against geopolitical chokepoints, deliberately front-loading imported 200G+ EML lasers and DSP chips to guarantee NPI (New Product Introduction) delivery targets.

HDIN Institutional Perspective

While management attributes the 105% physical inventory surge to robust AI-driven CSP order backlogs, the extreme dependency on a single upstream vendor—identified in filings as "Supplier A," absorbing 35.76% (8.89 billion RMB) of total procurement—exposes a critical vulnerability. SZSE: 300308 has successfully engineered tariff immunity via its Southeast Asian production nodes, but its technological moat remains held captive by Western DSP and EML laser chip chokepoints. Until the firm’s stated vertical integration strategy yields viable, in-house high-end optoelectronic alternatives, the fortress-like balance sheet serves merely as a liquidity buffer against impending hardware supply shocks, rather than a permanent structural advantage against upstream pricing power.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Access: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."

Operating Leverage and Pristine Cash Economics

Beyond the top-line revenue beat of 38.24 billion RMB (+60.25% YoY), SZSE: 300308 is demonstrating textbook operating leverage. Net profit attributable to shareholders surged 108.78% to 10.80 billion RMB, driven by a highly favorable price-mix variance as AI data center topologies shift aggressively toward 800G and 1.6T architectures. This product-mix optimization expanded the core optical communication module gross margin by nearly 800 basis points, from 34.65% to 42.61% on 21.09 million units sold.

The true quality of these earnings is validated by the unit’s cash economics. Operating Cash Flow (OCF) skyrocketed by 244.31% to 10.90 billion RMB, translating to a 101% cash conversion ratio. This 1-to-1 conversion confirms that the hyper-growth trajectory is underwritten by actual cash collections from tier-1 Cloud Service Providers (CSPs), not aggressive revenue recognition. R&D-to-Moat translation is equally disciplined: despite allocating 1.676 billion RMB to advance Silicon Photonics (SiPh) and Linear Drive Pluggable Optics (LPO) architectures, management capitalized a mere 3.62% of this expenditure, keeping the balance sheet unburdened by inflated intangible assets. The firm’s capital structure remains fortress-like, with 10.98 billion RMB in liquid monetary funds dwarfing a negligible 811 million RMB in combined short and long-term borrowings.

Figure Global Dominance in Al Compute: Zhongji lnnolight 2025 Performance & Strategic Roadmap

Tactical Stockpiling vs. Geographic ArbitrageTo digest the exponential growth in global AI token consumption, SZSE: 300308 triggered a massive internal capital allocation shift. Construction in Progress (CIP) expanded from 52.53 million RMB to 1.42 billion RMB, punctuated by the completion of the domestic Tongling Innolight High-end Optical Module Industrial Park Phase III.

However, the company’s structural moat increasingly relies on offshore geographic arbitrage. The rapid scaling of TeraHop Pte. Ltd.—which generated 2.38 billion RMB in net profit and now holds 23.54 billion RMB in assets—provides a dual advantage: tariff circumvention and tax optimization. Operating under Singapore’s DEI framework (10% tax) and Thailand’s Board of Investment incentives (0% tax), the overseas network inherently structurally lifts the consolidated bottom line.

Operationally, the balance sheet reveals aggressive defensive stockpiling. Inventory balances swelled by 80% to 12.68 billion RMB (28.00% of total assets), with raw materials doubling to 4.60 billion RMB. Crucially, the inventory impairment provision remained flat at 297.82 million RMB. This divergence confirms that the working capital build is a strict "make-to-order" hedge against geopolitical chokepoints, deliberately front-loading imported 200G+ EML lasers and DSP chips to guarantee NPI (New Product Introduction) delivery targets.

HDIN Institutional Perspective

While management attributes the 105% physical inventory surge to robust AI-driven CSP order backlogs, the extreme dependency on a single upstream vendor—identified in filings as "Supplier A," absorbing 35.76% (8.89 billion RMB) of total procurement—exposes a critical vulnerability. SZSE: 300308 has successfully engineered tariff immunity via its Southeast Asian production nodes, but its technological moat remains held captive by Western DSP and EML laser chip chokepoints. Until the firm’s stated vertical integration strategy yields viable, in-house high-end optoelectronic alternatives, the fortress-like balance sheet serves merely as a liquidity buffer against impending hardware supply shocks, rather than a permanent structural advantage against upstream pricing power.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Access: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."