Global Engineering Software Transition: NASDAQ: PTC and ETR: SIE Diverge on M&A Capital Allocation as $8.3B RPO Backlogs Define 2026 Outlook

Date : 2026-04-27

Reading : 306

The global industrial software sector is bifurcating as macroeconomic friction suppresses private-sector capital expenditure, forcing a strategic pivot toward sovereign infrastructure architectures. While NASDAQ: ADSK and NASDAQ: PTC exploit massive multi-year Enterprise Business Agreements to lock in $8.30 billion and $2.87 billion Remaining Performance Obligations (RPOs) respectively, Chinese pure-plays like SSE: 688083 (ZWSOFT) are accelerating R&D intensity past 51% to establish proprietary geometric kernels. This transatlantic divergence reflects a brutal reality: future margin expansion relies on Agentic AI M&A and supply-chain reshoring rather than organic seat growth.

Figure 2025 Global CAD/CAM/CAE Strategic Landscape

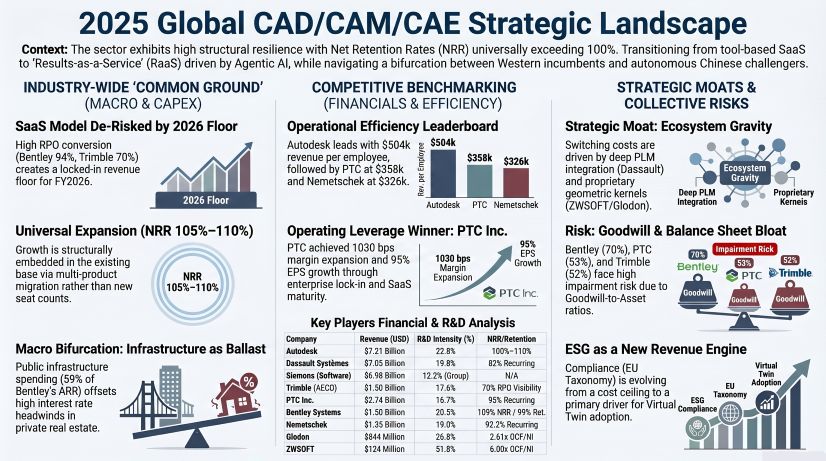

Operating Leverage, Unit Economics, and Balance Sheet Bloat

Operating Leverage, Unit Economics, and Balance Sheet Bloat

Operating leverage across the cohort is deeply bifurcated, driven by divergent commercial transition models. NASDAQ: PTC executed the most aggressive margin capture in FY2025, engineering a 1030 basis point operating margin expansion and a 95% EPS surge. This was structurally amplified by ASC 606 accounting dynamics, where longer-duration enterprise contracts injected high-margin upfront license revenue into the P&L without corresponding immediate cost increases.

On a unit-economic basis, NASDAQ: ADSK holds the gold standard for operational efficiency, generating $503,916 per employee via its direct-to-customer transaction model. By disintermediating channel partners, NASDAQ: ADSK transfers historical reseller discounts directly to its Non-GAAP operating profit. Conversely, localized challengers are absorbing severe friction to capture market share; SSE: 688083 operates at a highly compressed $69,767 per employee, requiring massive upfront direct sales investments to penetrate state-owned enterprise accounts.

The sector's aggressive substitution of internal R&D with M&A as "Synthetic CapEx" has introduced severe balance sheet vulnerabilities. NASDAQ: BSY and NASDAQ: TRMB now operate with Goodwill-to-Assets ratios of 69.8% and 51.7%, respectively. If integration of recent programmatic acquisitions into the iTwin Platform falters, or if 2026 public sector funding decelerates, these firms face immediate impairment risks—a reality already materializing for NASDAQ: TRMB ($12.8 million right-of-use impairment) and SSE: 688083 ($4.6 million realization on its Beijing BoChao acquisition).

Furthermore, a forensic quality-of-earnings review highlights localized accounting anomalies. While the Western standard is to expense nearly 100% of R&D (as demonstrated by EPA: DSY and XTRA: NEM), SZSE: 002410 (Glodon) capitalized $32.6 million—14.41% of its total R&D spend—artificially boosting near-term Net Income and masking the underlying erosion in its domestic construction market.

Geographic Resiliency and Kernel Autonomy

The sector’s defensive moat is no longer defined by simple workflow utility, but by regionalized data gravity and insulation from cyclical destocking. Global manufacturing conglomerates face high cyclical volatility; ETR: SIE explicitly notes that shifting US tariff frameworks and semiconductor supply chain decoupling heavily disrupt downstream automation CapEx. To insulate its growth, ETR: SIE deployed $10.7 billion to acquire Altair Engineering, pivoting its moat away from physical hardware toward AI-driven electronic design automation (EDA).

In contrast, AEC firms overweight in infrastructure exhibit counter-cyclical resilience. NASDAQ: BSY, deriving 59% of its ARR from Public Works/Utilities, relies on sovereign capital (such as Saudi Arabia’s Vision 2030 or US reindustrialization) to maintain an implied gross retention rate of 99%.

Geopolitics has fundamentally altered the technological supply chain. EPA: DSY shields its European aerospace and defense clients via its OUTSCALE sovereign cloud brand, leveraging SecNumCloud 3.2 certification to block extra-territorial data extraction. Meanwhile, Chinese challengers view Western third-party component interdependency as a critical supply chain "chokehold." SSE: 688083 relies on its proprietary Overdrive 3D geometric modeling kernel, while SZSE: 002410 deploys its fourth-generation GDMP 3D graphics platform. For these entities, autonomous codebases are non-negotiable strategic imperatives required to secure state-level domestic substitution contracts.

HDIN Institutional Perspective

The Street is fundamentally mispricing the execution risks embedded in the sector's $15 billion M&A binge. While consensus applauds the strategic shift toward generative design and the 3DEXPERIENCE "Generative Economy," the underlying structural bloat is alarming. Heavy reliance on $8.3 billion unbilled backlog structures masks the fact that net new seat growth has effectively stalled under a global "Macro Ceiling" of elevated interest rates. Furthermore, while the market penalizes Chinese equities for domestic macroeconomic contraction, it ignores the structural reality that SZSE: 002410 and SSE: 688083 are utilizing "pressure-style" R&D investments to construct localized platform moats. True FY2026 outperformance will belong strictly to entities that can monetize AI-driven "Results-as-a-Service" (RaaS) without requiring debt-funded, ecosystem-diluting acquisitions.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Figure 2025 Global CAD/CAM/CAE Strategic Landscape

Operating Leverage, Unit Economics, and Balance Sheet BloatOperating leverage across the cohort is deeply bifurcated, driven by divergent commercial transition models. NASDAQ: PTC executed the most aggressive margin capture in FY2025, engineering a 1030 basis point operating margin expansion and a 95% EPS surge. This was structurally amplified by ASC 606 accounting dynamics, where longer-duration enterprise contracts injected high-margin upfront license revenue into the P&L without corresponding immediate cost increases.

On a unit-economic basis, NASDAQ: ADSK holds the gold standard for operational efficiency, generating $503,916 per employee via its direct-to-customer transaction model. By disintermediating channel partners, NASDAQ: ADSK transfers historical reseller discounts directly to its Non-GAAP operating profit. Conversely, localized challengers are absorbing severe friction to capture market share; SSE: 688083 operates at a highly compressed $69,767 per employee, requiring massive upfront direct sales investments to penetrate state-owned enterprise accounts.

The sector's aggressive substitution of internal R&D with M&A as "Synthetic CapEx" has introduced severe balance sheet vulnerabilities. NASDAQ: BSY and NASDAQ: TRMB now operate with Goodwill-to-Assets ratios of 69.8% and 51.7%, respectively. If integration of recent programmatic acquisitions into the iTwin Platform falters, or if 2026 public sector funding decelerates, these firms face immediate impairment risks—a reality already materializing for NASDAQ: TRMB ($12.8 million right-of-use impairment) and SSE: 688083 ($4.6 million realization on its Beijing BoChao acquisition).

Furthermore, a forensic quality-of-earnings review highlights localized accounting anomalies. While the Western standard is to expense nearly 100% of R&D (as demonstrated by EPA: DSY and XTRA: NEM), SZSE: 002410 (Glodon) capitalized $32.6 million—14.41% of its total R&D spend—artificially boosting near-term Net Income and masking the underlying erosion in its domestic construction market.

Geographic Resiliency and Kernel Autonomy

The sector’s defensive moat is no longer defined by simple workflow utility, but by regionalized data gravity and insulation from cyclical destocking. Global manufacturing conglomerates face high cyclical volatility; ETR: SIE explicitly notes that shifting US tariff frameworks and semiconductor supply chain decoupling heavily disrupt downstream automation CapEx. To insulate its growth, ETR: SIE deployed $10.7 billion to acquire Altair Engineering, pivoting its moat away from physical hardware toward AI-driven electronic design automation (EDA).

In contrast, AEC firms overweight in infrastructure exhibit counter-cyclical resilience. NASDAQ: BSY, deriving 59% of its ARR from Public Works/Utilities, relies on sovereign capital (such as Saudi Arabia’s Vision 2030 or US reindustrialization) to maintain an implied gross retention rate of 99%.

Geopolitics has fundamentally altered the technological supply chain. EPA: DSY shields its European aerospace and defense clients via its OUTSCALE sovereign cloud brand, leveraging SecNumCloud 3.2 certification to block extra-territorial data extraction. Meanwhile, Chinese challengers view Western third-party component interdependency as a critical supply chain "chokehold." SSE: 688083 relies on its proprietary Overdrive 3D geometric modeling kernel, while SZSE: 002410 deploys its fourth-generation GDMP 3D graphics platform. For these entities, autonomous codebases are non-negotiable strategic imperatives required to secure state-level domestic substitution contracts.

HDIN Institutional Perspective

The Street is fundamentally mispricing the execution risks embedded in the sector's $15 billion M&A binge. While consensus applauds the strategic shift toward generative design and the 3DEXPERIENCE "Generative Economy," the underlying structural bloat is alarming. Heavy reliance on $8.3 billion unbilled backlog structures masks the fact that net new seat growth has effectively stalled under a global "Macro Ceiling" of elevated interest rates. Furthermore, while the market penalizes Chinese equities for domestic macroeconomic contraction, it ignores the structural reality that SZSE: 002410 and SSE: 688083 are utilizing "pressure-style" R&D investments to construct localized platform moats. True FY2026 outperformance will belong strictly to entities that can monetize AI-driven "Results-as-a-Service" (RaaS) without requiring debt-funded, ecosystem-diluting acquisitions.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.