Pony AI Asset-Light Pivot as Robotaxi Unit Breakeven Signals Structural Margin Expansion in Tier-1 China

Date : 2026-04-27

Reading : 161

Pony AI is executing a structural transition from capital-intensive fleet operations to an asset-light licensing framework, shifting CAPEX burdens to joint venture partners like GAC Toyota Motor Co., Ltd. (GTMC). This pivot, synchronized with reaching city-wide unit economics breakeven in Shenzhen and Guangzhou, insulates the firm against escalating U.S.-China technology export controls and domestic data localization mandates. Supported by a $1.16 billion liquidity buffer, this operational realignment fundamentally de-risks the deployment of 3,000 Gen-7 autonomous vehicles across international markets by late 2026.

Financial Forensic

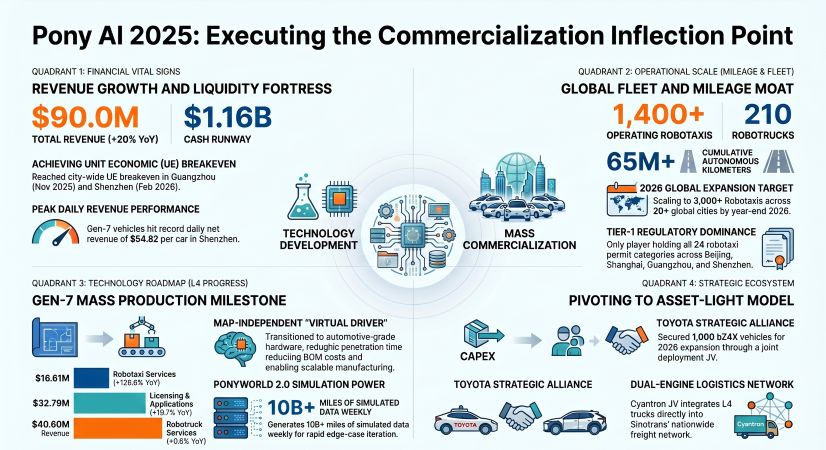

A forensic audit of the 2025 top-line growth ($90.0 million, +20.0% YoY) reveals a highly optimized revenue mix driving operating leverage. Gross margins expanded to 15.7% (up from 15.2%), catalyzed by a 128.6% surge in high-margin Robotaxi services ($16.61 million). However, the statutory GAAP net loss narrowing of 72.1% (to $76.76 million) is optically misleading—it was manufactured by a $128.03 million non-operating fair value gain triggered by the IPO of a GPU R&D investee.

Stripping out non-recurring windfalls, the Non-GAAP Adjusted Net Loss actually widened by 31.5% to $173.99 million. This underscores an intentional, steep operational deficit designed to front-load technological iteration and market share capture. Free Cash Flow (FCF) conversion remains deeply negative with a $208.8 million annual burn rate. Yet, capitalization is not a near-term headwind; dual-listing proceeds have fortified the balance sheet with $1.165 billion in high-liquidity reserves, guaranteeing an implied 5.5-year cash runway to execute its 2026 rollout without dilutive equity financing.

Figure Pony Al 2025: Executing the Commercialization Inflection Point

Operational Moat & Supply Chain

Operational Moat & Supply Chain

NASDAQ: PONY is systemically dismantling the historical constraints of Level 4 geographic scaling. The proprietary PonyWorld 2.0 world model and End-to-End (E2E) architecture have engineered a "Learnable Metric Space," deliberately degrading the system's reliance on high-definition mapping and compressing the time-to-market for new city penetration from six months to 15 days.

On the hardware front, the Gen-7 autonomous driving kit marks a definitive supply chain transition from industrial-grade components to automotive-grade integration. Mass production partnerships utilizing the Toyota bZ-4X and BAIC Alpha-T5 platforms have effectively minimized hardware depreciation, which now accounts for a negligible 1.7% of total COGS. Supply chain disclosures explicitly highlight deep integration with the NVIDIA DRIVE Orin compute platform and Robosense LiDAR arrays. Concurrently, the Cyantron joint venture with Sinotrans defends the $40.60 million Robotruck baseline, generating critical cross-domain R&D synergies where 80% of the underlying logic is shared across passenger and freight segments.

HDIN Institutional Perspective

While management aggressively promotes its 72% narrowing of statutory net loss, the underlying financial reality is far more capital-consumptive. The $173.99 million Non-GAAP operational deficit exposes the harsh truth of Level 4 autonomous scaling: the core business is intentionally burning cash to subsidize fleet density and algorithmic dominance.

Furthermore, the strategic pivot to an asset-light JV model with Toyota successfully offloads depreciation risks, but trades immediate balance sheet relief for long-term margin sharing. Peak daily net revenues of $54.82 per Gen-7 vehicle in Shenzhen validate the unit economics, but total corporate viability remains anchored to talent retention. With 44.6% of headcount dedicated strictly to R&D—and heavily compensated via $30.80 million in share-based awards—NASDAQ: PONY must prove its E2E architecture can achieve true algorithmic lock-in before intense industry poaching or equity market volatility compromises its engineering core.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Financial Forensic

A forensic audit of the 2025 top-line growth ($90.0 million, +20.0% YoY) reveals a highly optimized revenue mix driving operating leverage. Gross margins expanded to 15.7% (up from 15.2%), catalyzed by a 128.6% surge in high-margin Robotaxi services ($16.61 million). However, the statutory GAAP net loss narrowing of 72.1% (to $76.76 million) is optically misleading—it was manufactured by a $128.03 million non-operating fair value gain triggered by the IPO of a GPU R&D investee.

Stripping out non-recurring windfalls, the Non-GAAP Adjusted Net Loss actually widened by 31.5% to $173.99 million. This underscores an intentional, steep operational deficit designed to front-load technological iteration and market share capture. Free Cash Flow (FCF) conversion remains deeply negative with a $208.8 million annual burn rate. Yet, capitalization is not a near-term headwind; dual-listing proceeds have fortified the balance sheet with $1.165 billion in high-liquidity reserves, guaranteeing an implied 5.5-year cash runway to execute its 2026 rollout without dilutive equity financing.

Figure Pony Al 2025: Executing the Commercialization Inflection Point

Operational Moat & Supply ChainNASDAQ: PONY is systemically dismantling the historical constraints of Level 4 geographic scaling. The proprietary PonyWorld 2.0 world model and End-to-End (E2E) architecture have engineered a "Learnable Metric Space," deliberately degrading the system's reliance on high-definition mapping and compressing the time-to-market for new city penetration from six months to 15 days.

On the hardware front, the Gen-7 autonomous driving kit marks a definitive supply chain transition from industrial-grade components to automotive-grade integration. Mass production partnerships utilizing the Toyota bZ-4X and BAIC Alpha-T5 platforms have effectively minimized hardware depreciation, which now accounts for a negligible 1.7% of total COGS. Supply chain disclosures explicitly highlight deep integration with the NVIDIA DRIVE Orin compute platform and Robosense LiDAR arrays. Concurrently, the Cyantron joint venture with Sinotrans defends the $40.60 million Robotruck baseline, generating critical cross-domain R&D synergies where 80% of the underlying logic is shared across passenger and freight segments.

HDIN Institutional Perspective

While management aggressively promotes its 72% narrowing of statutory net loss, the underlying financial reality is far more capital-consumptive. The $173.99 million Non-GAAP operational deficit exposes the harsh truth of Level 4 autonomous scaling: the core business is intentionally burning cash to subsidize fleet density and algorithmic dominance.

Furthermore, the strategic pivot to an asset-light JV model with Toyota successfully offloads depreciation risks, but trades immediate balance sheet relief for long-term margin sharing. Peak daily net revenues of $54.82 per Gen-7 vehicle in Shenzhen validate the unit economics, but total corporate viability remains anchored to talent retention. With 44.6% of headcount dedicated strictly to R&D—and heavily compensated via $30.80 million in share-based awards—NASDAQ: PONY must prove its E2E architecture can achieve true algorithmic lock-in before intense industry poaching or equity market volatility compromises its engineering core.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.