Meituan Cannibalizes Operating Margins as $14.32B Marketing Outlay Signals Aggressive J-Curve Reset

Date : 2026-04-29

Reading : 124

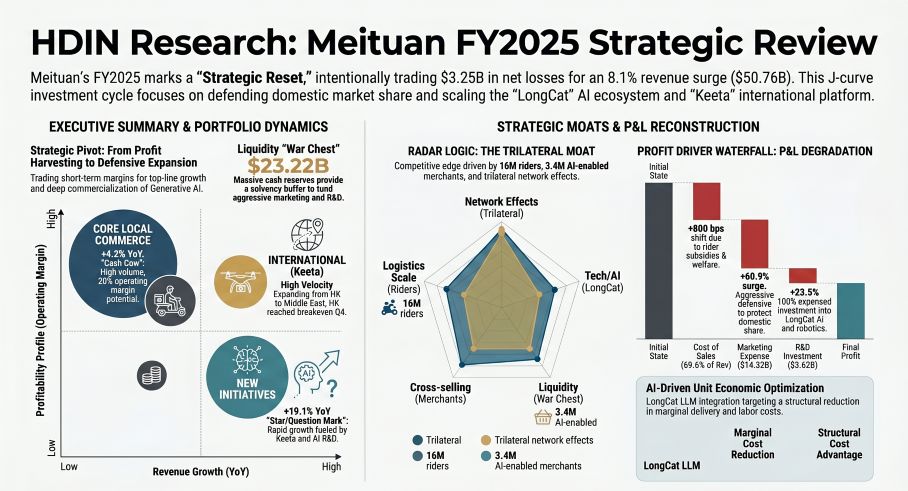

Meituan (HKG: 3690) reported a GAAP net loss of $3.25 billion in FY2025 as management deliberately dismantled its short-term operating margins to fund a dual-front expansion. The 60.9% surge in sales and marketing to $14.32 billion reflects a brutal defensive war against local competitors in mainland China, while concurrently subsidizing Keeta’s aggressive rollout across Riyadh and Kuwait. Constrained by macro headwinds and state directives to fund the $1.39 billion Tongzhou Fund for rider welfare, Meituan is weaponizing its $23.22 billion liquidity pool to force global market share consolidation.

Financial Forensic

A granular audit of the FY2025 P&L reveals a structural decoupling of top-line revenue ($50.76 billion, +8.1% YoY) from unit-level profitability. The Cost of Sales expanded by 800 basis points to 69.6% of total revenue ($35.31 billion), driven almost entirely by variable fulfillment costs and the mandatory integration of commercial occupational injury insurance for its 16 million delivery riders.

Despite the compressed gross margins and the headline -$3.25 billion net loss, the underlying cash-conversion metrics indicate deliberate capital allocation rather than operational distress. Non-cash drag—including $1.38 billion in depreciation and $835 million in share-based compensation—masks an inherently cash-generative core. Meituan is aggressively redirecting surplus capital from its Core Local Commerce into a high-risk, high-TAM R&D pipeline. The company deployed $3.62 billion (+23.5% YoY) into R&D, implementing a highly conservative 100% expensing model with zero capitalization of intangible assets. Notably, administrative operating leverage remains elite; General & Administrative (G&A) expenses were held to exactly 3.3% of revenue ($1.66 billion) for the second consecutive year, proving the back-office architecture can scale transaction volume without linear headcount bloat.

Figure Meituan FY2025 Strategic Review

Operational Moat

Operational Moat

To neutralize the inflationary pressure of gig-economy labor, Meituan is attempting a high-capex transition from variable labor logistics to a fixed-cost autonomous fulfillment network. The integration of its proprietary large language model, LongCat (龙猫), and the Xiao Mei consumer AI assistant is designed to optimize algorithmic dispatch and shift user queries to demand-driven conversational commerce.

Geographically, the capital deployed into overseas market acquisition is yielding early structural validation. The international delivery brand, Keeta, achieved positive unit economics and operating profitability in Hong Kong by Q4 2025, providing a blueprint for its current aggressive rollouts across the Middle East (Jeddah, Mecca, Qatar, UAE). Domestically, Meituan is actively offsetting the rigid labor costs associated with its Tongzhou commitments by scaling its proprietary L4 Autonomous Vehicles (over 5.5 million completed orders in Beijing and Shenzhen) and its fourth-generation delivery drones (over 780,000 orders across 70 routes).

HDIN Institutional Perspective

We challenge the Street’s immediate bearish reaction to Meituan's GAAP net loss, but remain skeptical of the timeline for its "Retail + Technology" cost-deflation narrative. Management is executing a classic J-curve investment cycle, utilizing a fortress $23.22 billion balance sheet to suffocate undercapitalized rivals. However, the 22.2% YoY spike in physical fulfillment costs underscores that Meituan remains structurally tethered to blue-collar wage inflation and regulatory compliance. Until the L4 autonomous fleet scales beyond geo-fenced pilot zones in Shenzhen to handle a material percentage of the aggregate transaction volume, the heavy $3.62 billion R&D spend functions primarily as an entry ticket to the AI race rather than a near-term margin catalyst. The critical metric for 2H2026 will not be total revenue growth, but whether the Keeta Middle East expansion can replicate the Hong Kong breakeven velocity before the domestic marketing subsidy war exhausts organic cash flows.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Financial Forensic

A granular audit of the FY2025 P&L reveals a structural decoupling of top-line revenue ($50.76 billion, +8.1% YoY) from unit-level profitability. The Cost of Sales expanded by 800 basis points to 69.6% of total revenue ($35.31 billion), driven almost entirely by variable fulfillment costs and the mandatory integration of commercial occupational injury insurance for its 16 million delivery riders.

Despite the compressed gross margins and the headline -$3.25 billion net loss, the underlying cash-conversion metrics indicate deliberate capital allocation rather than operational distress. Non-cash drag—including $1.38 billion in depreciation and $835 million in share-based compensation—masks an inherently cash-generative core. Meituan is aggressively redirecting surplus capital from its Core Local Commerce into a high-risk, high-TAM R&D pipeline. The company deployed $3.62 billion (+23.5% YoY) into R&D, implementing a highly conservative 100% expensing model with zero capitalization of intangible assets. Notably, administrative operating leverage remains elite; General & Administrative (G&A) expenses were held to exactly 3.3% of revenue ($1.66 billion) for the second consecutive year, proving the back-office architecture can scale transaction volume without linear headcount bloat.

Figure Meituan FY2025 Strategic Review

Operational MoatTo neutralize the inflationary pressure of gig-economy labor, Meituan is attempting a high-capex transition from variable labor logistics to a fixed-cost autonomous fulfillment network. The integration of its proprietary large language model, LongCat (龙猫), and the Xiao Mei consumer AI assistant is designed to optimize algorithmic dispatch and shift user queries to demand-driven conversational commerce.

Geographically, the capital deployed into overseas market acquisition is yielding early structural validation. The international delivery brand, Keeta, achieved positive unit economics and operating profitability in Hong Kong by Q4 2025, providing a blueprint for its current aggressive rollouts across the Middle East (Jeddah, Mecca, Qatar, UAE). Domestically, Meituan is actively offsetting the rigid labor costs associated with its Tongzhou commitments by scaling its proprietary L4 Autonomous Vehicles (over 5.5 million completed orders in Beijing and Shenzhen) and its fourth-generation delivery drones (over 780,000 orders across 70 routes).

HDIN Institutional Perspective

We challenge the Street’s immediate bearish reaction to Meituan's GAAP net loss, but remain skeptical of the timeline for its "Retail + Technology" cost-deflation narrative. Management is executing a classic J-curve investment cycle, utilizing a fortress $23.22 billion balance sheet to suffocate undercapitalized rivals. However, the 22.2% YoY spike in physical fulfillment costs underscores that Meituan remains structurally tethered to blue-collar wage inflation and regulatory compliance. Until the L4 autonomous fleet scales beyond geo-fenced pilot zones in Shenzhen to handle a material percentage of the aggregate transaction volume, the heavy $3.62 billion R&D spend functions primarily as an entry ticket to the AI race rather than a near-term margin catalyst. The critical metric for 2H2026 will not be total revenue growth, but whether the Keeta Middle East expansion can replicate the Hong Kong breakeven velocity before the domestic marketing subsidy war exhausts organic cash flows.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*