L4 Autonomous Driving Commercialization: Pony AI and WeRide Diverge on Asset-Light Execution as Peak CapEx Defines 2026 Outlook

Date : 2026-04-29

Reading : 326

The 2025 financial disclosures of Pony AI and WeRide reveal a critical pivot from venture-backed algorithmic validation to public-market-funded fleet commercialization. Driven by US-China geopolitical decoupling and the U.S. Department of Commerce's prohibitive Vehicle Connectivity System (VCS) rules, both entities have abandoned North American deployment to concentrate strictly on domestic Tier-1 cities and Middle Eastern hubs like Abu Dhabi. Despite symmetrical ~$174M underlying operational deficits, an aggressive combined CapEx surge of $78.5M signals peak internal capital intensity as both firms utilize their balance sheets to prove unit economics.

Unmasking Quality of Earnings and the 2026 CapEx Spike

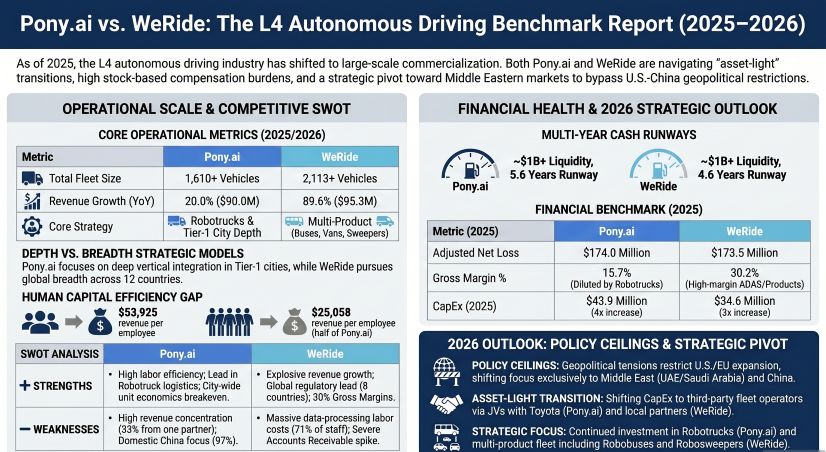

A forensic audit of 2025 GAAP net income reveals exceptionally low earnings quality across the sector, heavily distorted by non-cash investment artifacts and massive share-based compensation. Pony AI reported a GAAP Net Loss of $76.8M, artificially inflated by a $128.0M non-cash fair value gain on trading securities. Stripping this away exposes an Operating Cash Flow (OCF) drain of $165.0M. Similarly, WeRide posted a $230.2M GAAP Net Loss, translating to an OCF burn of $183.9M. When normalized for Non-GAAP metrics, the core operational deficits of both companies are eerily symmetrical: ~$174.0M for Pony AI and ~$173.5M for WeRide.

However, the divergence in top-line quality requires heightened institutional scrutiny. WeRide delivered explosive 89.6% year-over-year revenue growth ($95.25M), yet this was accompanied by a severe 83% spike in Accounts Receivable to $64.29M. With AR constituting roughly 67% of its total 2025 revenue, WeRide is exhibiting aggressive channel stuffing or highly lenient credit extensions to stimulate sales. Conversely, Pony AI's AR decreased to $23.6M on $90.0M in revenue, yet it suffers from extreme customer concentration, heavily relying on a $29.6M related-party transaction (32.9% of total revenue) via its joint venture with Sinotrans.

Both firms have initiated a synchronized, massive scale-up in Capital Expenditures. Pony AI's CapEx surged almost 4x to $43.9M to deploy its Gen-7 vehicle platforms, while WeRide mirrored this with a nearly 3x increase to $34.6M to rollout its GXR fleet. This capital lock-in confirms that the industry has entered a peak "commercialization chasm"—forcing software developers to fund their own mass-produced hardware deployments before traditional OEMs will assume the balance sheet risk.

Figure Pony ai vs WeRide: The L4 Autonomous Driving Benchmark Report (2025-2026)

Geographic Arbitrage and Architectural Defensibility

Geographic Arbitrage and Architectural Defensibility

The competitive moat between the two entities is defined by a clash between human capital efficiency and gross margin maximization.

WeRide currently commands superior pricing power, printing a 30.2% gross margin via an aggressive "asset-light" international strategy. By utilizing local partners in the UAE and Saudi Arabia for dispatch and maintenance, WeRide monetizes its technology stack without holding heavy localized physical assets. To mitigate U.S. export controls on advanced semiconductors, the company engineered its proprietary HPC 3.0 high-performance computing platform, structurally reducing its hardware bill of materials by 50%. However, this comes at a severe operational cost: WeRide requires a massive brute-force backend, employing 2,694 R&D data processing personnel, which crushes its human capital efficiency to a mere $25,058 in revenue per employee.

Pony AI operates on a significantly tighter 15.7% aggregate gross margin, deliberately absorbing the low-margin drag of its early-stage B2B commercial freight division. Yet, its organizational scaling efficiency is structurally superior, generating $53,925 per employee due to an AI-automated data labeling pipeline and a lean 1,669 total headcount. Technologically, rather than outright replacing restricted foreign chips, Pony AI relies on its bespoke in-house Autonomous Driving Computation Unit (ADCU) to maximize the throughput of existing automotive-grade NVIDIA processors. The firm's moat rests on depth over breadth, successfully achieving unit economic breakeven for Robotaxis in Guangzhou and Shenzhen by generating peak daily net revenues of $54.80 per vehicle.

HDIN Institutional Perspective

Management teams across the autonomous sector continuously market an imminent "asset-light" future, yet their 2025 balance sheets outright contradict this rhetoric. The synchronized $78M CapEx surge confirms that third-party fleet operators refuse to bear the capital expenditure of buying robotaxis until AI developers absorb the upfront financial damage of proving city-level viability.

While WeRide demonstrates superior global deployment velocity, its balance sheet carries distinct governance risks—specifically the procurement of $9.29M in mapping data via Guangzhou Yuji, an entity controlled by the CEO's sibling, layered on top of alarming AR accumulations. Conversely, Pony AI's cleaner cash-conversion cycle is offset by a precarious dependency on a single domestic freight partner. Ultimately, both companies successfully leveraged dual listings in Hong Kong to construct ~$1B liquidity runways, securing roughly 5 years of survival. The sector is entering a definitive 'trough-discovery' phase: the winner in 2026 will not be dictated by algorithmic superiority, but by who can successfully transition their self-funded Gen-7 and GXR fleets off their own balance sheets and onto the balance sheets of Middle Eastern sovereign partners and Tier-1 OEMs.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."

Unmasking Quality of Earnings and the 2026 CapEx Spike

A forensic audit of 2025 GAAP net income reveals exceptionally low earnings quality across the sector, heavily distorted by non-cash investment artifacts and massive share-based compensation. Pony AI reported a GAAP Net Loss of $76.8M, artificially inflated by a $128.0M non-cash fair value gain on trading securities. Stripping this away exposes an Operating Cash Flow (OCF) drain of $165.0M. Similarly, WeRide posted a $230.2M GAAP Net Loss, translating to an OCF burn of $183.9M. When normalized for Non-GAAP metrics, the core operational deficits of both companies are eerily symmetrical: ~$174.0M for Pony AI and ~$173.5M for WeRide.

However, the divergence in top-line quality requires heightened institutional scrutiny. WeRide delivered explosive 89.6% year-over-year revenue growth ($95.25M), yet this was accompanied by a severe 83% spike in Accounts Receivable to $64.29M. With AR constituting roughly 67% of its total 2025 revenue, WeRide is exhibiting aggressive channel stuffing or highly lenient credit extensions to stimulate sales. Conversely, Pony AI's AR decreased to $23.6M on $90.0M in revenue, yet it suffers from extreme customer concentration, heavily relying on a $29.6M related-party transaction (32.9% of total revenue) via its joint venture with Sinotrans.

Both firms have initiated a synchronized, massive scale-up in Capital Expenditures. Pony AI's CapEx surged almost 4x to $43.9M to deploy its Gen-7 vehicle platforms, while WeRide mirrored this with a nearly 3x increase to $34.6M to rollout its GXR fleet. This capital lock-in confirms that the industry has entered a peak "commercialization chasm"—forcing software developers to fund their own mass-produced hardware deployments before traditional OEMs will assume the balance sheet risk.

Figure Pony ai vs WeRide: The L4 Autonomous Driving Benchmark Report (2025-2026)

Geographic Arbitrage and Architectural DefensibilityThe competitive moat between the two entities is defined by a clash between human capital efficiency and gross margin maximization.

WeRide currently commands superior pricing power, printing a 30.2% gross margin via an aggressive "asset-light" international strategy. By utilizing local partners in the UAE and Saudi Arabia for dispatch and maintenance, WeRide monetizes its technology stack without holding heavy localized physical assets. To mitigate U.S. export controls on advanced semiconductors, the company engineered its proprietary HPC 3.0 high-performance computing platform, structurally reducing its hardware bill of materials by 50%. However, this comes at a severe operational cost: WeRide requires a massive brute-force backend, employing 2,694 R&D data processing personnel, which crushes its human capital efficiency to a mere $25,058 in revenue per employee.

Pony AI operates on a significantly tighter 15.7% aggregate gross margin, deliberately absorbing the low-margin drag of its early-stage B2B commercial freight division. Yet, its organizational scaling efficiency is structurally superior, generating $53,925 per employee due to an AI-automated data labeling pipeline and a lean 1,669 total headcount. Technologically, rather than outright replacing restricted foreign chips, Pony AI relies on its bespoke in-house Autonomous Driving Computation Unit (ADCU) to maximize the throughput of existing automotive-grade NVIDIA processors. The firm's moat rests on depth over breadth, successfully achieving unit economic breakeven for Robotaxis in Guangzhou and Shenzhen by generating peak daily net revenues of $54.80 per vehicle.

HDIN Institutional Perspective

Management teams across the autonomous sector continuously market an imminent "asset-light" future, yet their 2025 balance sheets outright contradict this rhetoric. The synchronized $78M CapEx surge confirms that third-party fleet operators refuse to bear the capital expenditure of buying robotaxis until AI developers absorb the upfront financial damage of proving city-level viability.

While WeRide demonstrates superior global deployment velocity, its balance sheet carries distinct governance risks—specifically the procurement of $9.29M in mapping data via Guangzhou Yuji, an entity controlled by the CEO's sibling, layered on top of alarming AR accumulations. Conversely, Pony AI's cleaner cash-conversion cycle is offset by a precarious dependency on a single domestic freight partner. Ultimately, both companies successfully leveraged dual listings in Hong Kong to construct ~$1B liquidity runways, securing roughly 5 years of survival. The sector is entering a definitive 'trough-discovery' phase: the winner in 2026 will not be dictated by algorithmic superiority, but by who can successfully transition their self-funded Gen-7 and GXR fleets off their own balance sheets and onto the balance sheets of Middle Eastern sovereign partners and Tier-1 OEMs.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."