Cheetah Mobile Accelerates Hardware Pivot as 490-bps Gross Margin Expansion Signals Structural Unit-Economic Shift

Date : 2026-04-29

Reading : 92

Cheetah Mobile is aggressively shedding its legacy utility-app profile, redeploying capital into a highly fragmented US-Sino robotics supply chain via controlling stakes in Beijing OrionStar and UFACTORY. While top-line revenue expanded 42.6% to $160.06M in FY2025, the firm remains squeezed by a -20.44% net profit margin driven by heavy M&A amortization. Geopolitical export controls on advanced compute chips directly constrain the hardware pipeline, forcing management to offshore data infrastructure to AWS and Tencent Cloud to bypass regional compliance traps and preserve enterprise adoption.

Operating Leverage and Cash-Burn Realities

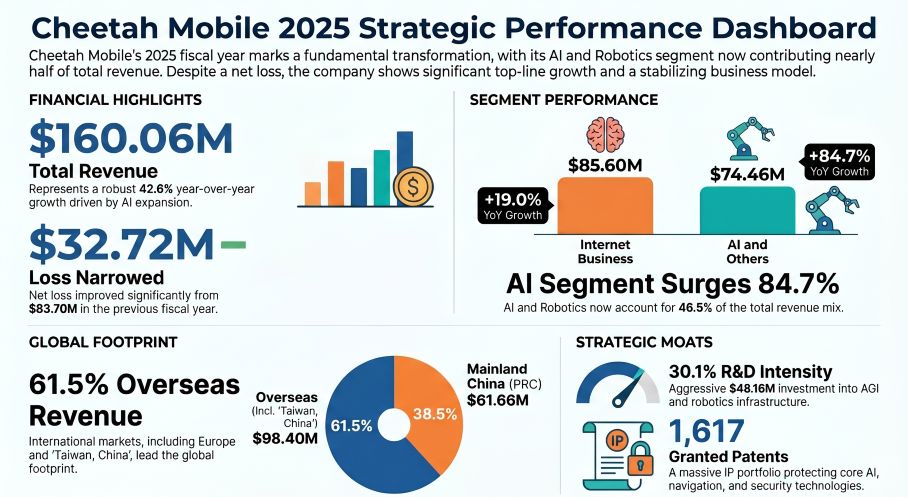

A forensic decomposition of NYSE: CMCM’s 2025 income statement reveals definitive, albeit early, signs of operating leverage. The company successfully uncoupled revenue growth from operating expenses, driving a 42.6% top-line surge ($160.06M) against a marginal 3.2% increase in OpEx ($141.01M). This scale absorption yielded a 490-basis-point gross margin expansion (to 72.5%) and compressed operating loss margins from -54.2% to -15.6%.

However, Free Cash Flow (FCF) conversion remains structurally impaired. The reported -$32.72M net loss understates the operational cash drain, though Operating Cash Flow (OCF) clocked in slightly better at -$23.97M, supported by a heavy $18.89M amortization add-back. Crucially, a $61.09M drain in working capital—specifically tied to shrinking accrued liabilities—demonstrates the immediate cash cost of transitioning from a zero-marginal-cost software model to a capital-intensive hardware supply chain. Furthermore, an aggressive $48.16M allocated to R&D (30.1% intensity) is less indicative of organic innovation and more reflective of the amortization weight from recently absorbed M&A targets.

Figure Cheetah Mobile 2025 Strategic Performance Dashboard

Hardware Integration and Open-Source Arbitrage

Hardware Integration and Open-Source Arbitrage

The strategic divestiture of the Live.me stake marks a definitive exit from legacy B2C models, funded by a sharp pivot into B2B Agentic AI and service robotics. Internally, a net 8.9% headcount reduction juxtaposed with a 56.5% surge in Revenue per Employee ($188,087) indicates a ruthless internal optimization.

Yet, the operational moat is heavily dependent on third-party architectures. Rather than bearing the capital-crushing load of training proprietary foundational Large Language Models (LLMs), management is executing an open-source arbitrage strategy. Products like EasyClaw and enterprise AI coworkers rely on external frameworks such as OpenClaw integrated with their legacy Blue Core software engine. On the hardware front, the integration of Beijing OrionStar ($37.39M cash equivalent) and UFACTORY ($13.84M) exposes the firm to severe supply-chain concentration risks. NYSE: CMCM’s robotics manufacturing is highly vulnerable to US Bureau of Industry and Security (BIS) export controls, which threaten the procurement of critical sub-components and advanced computing chips required for edge-AI processing.

HDIN Institutional Perspective

Management champions the 84.7% growth in the "AI and Others" segment as a vindication of its strategic pivot, but the structural reality reveals profound integration and regulatory tail risks. The massive $80.28M in combined goodwill booked from recent acquisitions severely bloats the asset base, rendering the firm's -12.45% ROE highly vulnerable to future impairment shocks if robotics adoption stalls.

Furthermore, NYSE: CMCM's underlying business architecture remains uncomfortably fragile. The firm is not building a deep-tech foundational moat; it is highly reliant on external frameworks and third-party contract manufacturers. With a balance sheet liability structure overwhelmingly skewed short-term (93.5% of total liabilities) and a latent exposure of $21.64M in unrecognized tax benefits, the company’s liquidity buffer of $209.62M is adequate but strictly defensive. Any geopolitical escalation restricting access to US-origin semiconductors will immediately paralyze their hardware pipeline, transforming the current M&A-driven revenue surge into a stalled, depreciating asset trap.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Operating Leverage and Cash-Burn Realities

A forensic decomposition of NYSE: CMCM’s 2025 income statement reveals definitive, albeit early, signs of operating leverage. The company successfully uncoupled revenue growth from operating expenses, driving a 42.6% top-line surge ($160.06M) against a marginal 3.2% increase in OpEx ($141.01M). This scale absorption yielded a 490-basis-point gross margin expansion (to 72.5%) and compressed operating loss margins from -54.2% to -15.6%.

However, Free Cash Flow (FCF) conversion remains structurally impaired. The reported -$32.72M net loss understates the operational cash drain, though Operating Cash Flow (OCF) clocked in slightly better at -$23.97M, supported by a heavy $18.89M amortization add-back. Crucially, a $61.09M drain in working capital—specifically tied to shrinking accrued liabilities—demonstrates the immediate cash cost of transitioning from a zero-marginal-cost software model to a capital-intensive hardware supply chain. Furthermore, an aggressive $48.16M allocated to R&D (30.1% intensity) is less indicative of organic innovation and more reflective of the amortization weight from recently absorbed M&A targets.

Figure Cheetah Mobile 2025 Strategic Performance Dashboard

Hardware Integration and Open-Source ArbitrageThe strategic divestiture of the Live.me stake marks a definitive exit from legacy B2C models, funded by a sharp pivot into B2B Agentic AI and service robotics. Internally, a net 8.9% headcount reduction juxtaposed with a 56.5% surge in Revenue per Employee ($188,087) indicates a ruthless internal optimization.

Yet, the operational moat is heavily dependent on third-party architectures. Rather than bearing the capital-crushing load of training proprietary foundational Large Language Models (LLMs), management is executing an open-source arbitrage strategy. Products like EasyClaw and enterprise AI coworkers rely on external frameworks such as OpenClaw integrated with their legacy Blue Core software engine. On the hardware front, the integration of Beijing OrionStar ($37.39M cash equivalent) and UFACTORY ($13.84M) exposes the firm to severe supply-chain concentration risks. NYSE: CMCM’s robotics manufacturing is highly vulnerable to US Bureau of Industry and Security (BIS) export controls, which threaten the procurement of critical sub-components and advanced computing chips required for edge-AI processing.

HDIN Institutional Perspective

Management champions the 84.7% growth in the "AI and Others" segment as a vindication of its strategic pivot, but the structural reality reveals profound integration and regulatory tail risks. The massive $80.28M in combined goodwill booked from recent acquisitions severely bloats the asset base, rendering the firm's -12.45% ROE highly vulnerable to future impairment shocks if robotics adoption stalls.

Furthermore, NYSE: CMCM's underlying business architecture remains uncomfortably fragile. The firm is not building a deep-tech foundational moat; it is highly reliant on external frameworks and third-party contract manufacturers. With a balance sheet liability structure overwhelmingly skewed short-term (93.5% of total liabilities) and a latent exposure of $21.64M in unrecognized tax benefits, the company’s liquidity buffer of $209.62M is adequate but strictly defensive. Any geopolitical escalation restricting access to US-origin semiconductors will immediately paralyze their hardware pipeline, transforming the current M&A-driven revenue surge into a stalled, depreciating asset trap.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*