Clinical Diagnostics Cycle Phase: LH Diverge from Genomic Challengers on Operating Leverage as Receivables Stress Defines 2026 Outlook

Date : 2026-04-30

Reading : 338

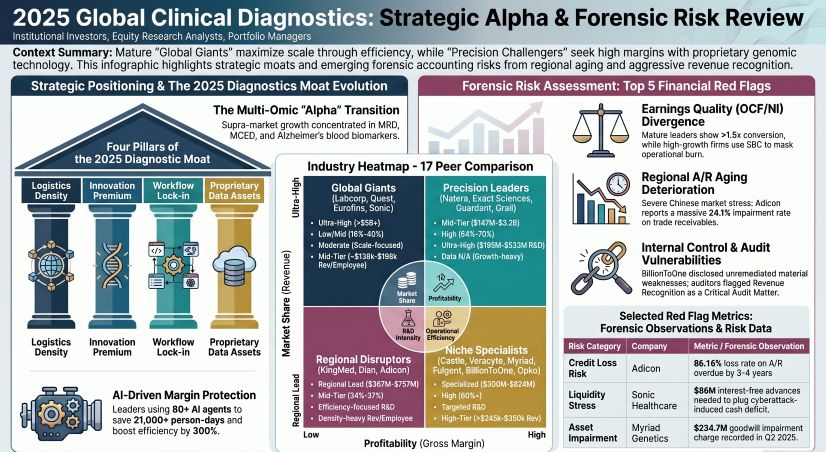

The clinical diagnostics sector is fracturing into two distinct economic realities. While global incumbents like NYSE: LH and NYSE: DGX deploy massive automation CapEx into facilities like the Durham mega-hub to offset U.S. wage inflation, regional pure-plays face critical working capital degradation. Driven by China's DRG/DIP payment reforms, operators like Adicon report a staggering 24.1% Accounts Receivable impairment rate ($57.1M), signaling a severe liquidity squeeze. For 2026, sector survival dictates a pivot from commoditized volume growth to AI-driven unit economics and stringent supply chain localization.

Operating Leverage and Unit Economic Divergence

A forensic audit of 2025 earnings quality reveals a widening chasm in Cash Conversion Cycles (CCC) and Operating Cash Flow to Net Income (OCF/NI) ratios. Scale generalists demonstrate superior cash realization; EPA: ERF achieved a 2.96x OCF/NI conversion, while NYSE: LH and NYSE: DGX maintain strict Days Sales Outstanding (DSO) caps of exactly 48 days, yielding >1.8x conversions.

Conversely, high-growth esoteric tiers rely heavily on proprietary ADLT and PLA coding to drive supreme revenue-per-employee metrics (e.g., NASDAQ: CSTL generating ~$389,800/head). However, their operational cash burn is frequently obscured by massive stock-based compensation (SBC) add-backs. NASDAQ: NTRA, for example, offset a $208.2M net loss with $354.4M in SBC to fund its Signatera franchise expansion.

Regional and mid-tier markets face severe balance sheet toxicity. Adicon’s Expected Credit Loss (ECL) matrix exposes an 86.16% loss rate on receivables aged 3-4 years. Concurrently, U.S. collections remain vulnerable to infrastructure shocks, evidenced by ASX: SHL being forced to absorb $86M in interest-free advances to plug a working capital deficit triggered by the Change Healthcare cyberattack. Despite this volatile reimbursement environment, newly public entities like NASDAQ: BTMD aggressively claim zero allowances for credit losses, a posture undermined by their formally disclosed material weaknesses in internal controls.

Figure 2025 Global Clinical Diagnostics: Strategic Alpha & Forensic Risk Review

CapEx Realignment and Vendor Oligopolies

CapEx Realignment and Vendor Oligopolies

Supply chain resilience defines the 2026 competitive moat. The molecular diagnostics segment suffers from acute vendor concentration, with NASDAQ: NTRA, NASDAQ: EXAS, and NASDAQ: GRAL critically dependent on NASDAQ: ILMN for Next-Generation Sequencing (NGS) platforms and Streck, Inc. for cell-free DNA blood collection tubes.

To hedge against this oligopoly, leaders are aggressively internalizing production. EPA: ERF is vertically integrating its In Vitro Diagnostics (IVD) Solutions division to manufacture ELISA and PCR kits in-house. In Greater China, structural domestic substitution is mandatory for margin defense; Adicon slashed reagent costs by 14% via localization, while SZSE: 300244 (Dian Diagnostics) scaled its self-developed IVD products to offset centralized procurement pressures.

Capital allocation is definitively shifting from capacity expansion to AI-driven workflow lock-in. NYSE: DGX is deploying $550M into Project Nova and leveraging AI for route optimization across its 83,000 daily logistics stops. Meanwhile, NASDAQ: EXAS is executing a $150M productivity plan via core automation to defend the margins of its Cologuard Plus and newly launched Cancerguard MCED portfolios. Those failing to match this digital CapEx cycle will suffer margin erosion as fixed labor costs outpace statutorily capped PAMA reimbursements.

HDIN Institutional Perspective

The clinical testing sector is entering a definitive "trough-discovery" phase regarding earnings quality. While management narratives universally emphasize AI-driven workflow optimization, the aggressive zero-allowance A/R provisioning by high-growth genomic firms—coupled with crippling $234.7M goodwill write-downs at NASDAQ: MYGN—suggests severe structural mispricing of underlying reimbursement risks. The widening spread in ROIC between asset-heavy incumbents executing digital revenue cycle efficiencies and esoteric challengers surviving on SBC-adjusted cash flows indicates a brutal 2H2026 margin squeeze for players unable to control their "last mile" collection cycles.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Operating Leverage and Unit Economic Divergence

A forensic audit of 2025 earnings quality reveals a widening chasm in Cash Conversion Cycles (CCC) and Operating Cash Flow to Net Income (OCF/NI) ratios. Scale generalists demonstrate superior cash realization; EPA: ERF achieved a 2.96x OCF/NI conversion, while NYSE: LH and NYSE: DGX maintain strict Days Sales Outstanding (DSO) caps of exactly 48 days, yielding >1.8x conversions.

Conversely, high-growth esoteric tiers rely heavily on proprietary ADLT and PLA coding to drive supreme revenue-per-employee metrics (e.g., NASDAQ: CSTL generating ~$389,800/head). However, their operational cash burn is frequently obscured by massive stock-based compensation (SBC) add-backs. NASDAQ: NTRA, for example, offset a $208.2M net loss with $354.4M in SBC to fund its Signatera franchise expansion.

Regional and mid-tier markets face severe balance sheet toxicity. Adicon’s Expected Credit Loss (ECL) matrix exposes an 86.16% loss rate on receivables aged 3-4 years. Concurrently, U.S. collections remain vulnerable to infrastructure shocks, evidenced by ASX: SHL being forced to absorb $86M in interest-free advances to plug a working capital deficit triggered by the Change Healthcare cyberattack. Despite this volatile reimbursement environment, newly public entities like NASDAQ: BTMD aggressively claim zero allowances for credit losses, a posture undermined by their formally disclosed material weaknesses in internal controls.

Figure 2025 Global Clinical Diagnostics: Strategic Alpha & Forensic Risk Review

CapEx Realignment and Vendor OligopoliesSupply chain resilience defines the 2026 competitive moat. The molecular diagnostics segment suffers from acute vendor concentration, with NASDAQ: NTRA, NASDAQ: EXAS, and NASDAQ: GRAL critically dependent on NASDAQ: ILMN for Next-Generation Sequencing (NGS) platforms and Streck, Inc. for cell-free DNA blood collection tubes.

To hedge against this oligopoly, leaders are aggressively internalizing production. EPA: ERF is vertically integrating its In Vitro Diagnostics (IVD) Solutions division to manufacture ELISA and PCR kits in-house. In Greater China, structural domestic substitution is mandatory for margin defense; Adicon slashed reagent costs by 14% via localization, while SZSE: 300244 (Dian Diagnostics) scaled its self-developed IVD products to offset centralized procurement pressures.

Capital allocation is definitively shifting from capacity expansion to AI-driven workflow lock-in. NYSE: DGX is deploying $550M into Project Nova and leveraging AI for route optimization across its 83,000 daily logistics stops. Meanwhile, NASDAQ: EXAS is executing a $150M productivity plan via core automation to defend the margins of its Cologuard Plus and newly launched Cancerguard MCED portfolios. Those failing to match this digital CapEx cycle will suffer margin erosion as fixed labor costs outpace statutorily capped PAMA reimbursements.

HDIN Institutional Perspective

The clinical testing sector is entering a definitive "trough-discovery" phase regarding earnings quality. While management narratives universally emphasize AI-driven workflow optimization, the aggressive zero-allowance A/R provisioning by high-growth genomic firms—coupled with crippling $234.7M goodwill write-downs at NASDAQ: MYGN—suggests severe structural mispricing of underlying reimbursement risks. The widening spread in ROIC between asset-heavy incumbents executing digital revenue cycle efficiencies and esoteric challengers surviving on SBC-adjusted cash flows indicates a brutal 2H2026 margin squeeze for players unable to control their "last mile" collection cycles.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*