Life Sciences Tool Trough Cycle: Illumina, Thermo Fisher, and MGI Tech Diverge on Supply Chain Localization as $1.52B CapEx Shift Defines 2026 Outlook

Date : 2026-04-30

Reading : 388

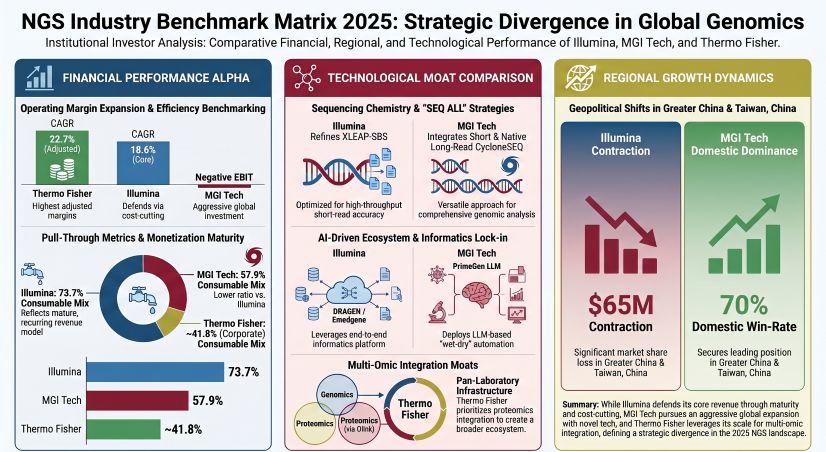

The global genomics sector faces a brutal geopolitical decoupling. NASDAQ: ILMN shed $65 million in Greater China revenue following its inclusion on China's Unreliable Entities List, while SHA: 688114 (MGI Tech) exploited domestic import substitution to capture 70% of public tenders. To circumvent the U.S. BIOSECURE Act and regional tariffs, manufacturers are abandoning globalized supply chains. NYSE: TMO directed $1.52 billion in CapEx toward U.S. localized sterile facilities, while MGI scaled "In-For-By" manufacturing in Latvia and San Jose. This massive capital realignment fundamentally depresses near-term sector operating margins.

Figure NGS Industry Benchmark Matrix 2025

Free Cash Flow Conversion and Unit Economic Fractures

Free Cash Flow Conversion and Unit Economic Fractures

A forensic audit of FY2025 financial disclosures reveals severe structural fractures in operating leverage and capital allocation across the cohort.

NYSE: TMO exhibits best-in-class economies of scale, generating a massive 1.17x Operating Cash Flow (OCF) to Net Income conversion rate ($7.81 billion OCF against $6.70 billion net income). Its sub-20% SG&A ratio confirms an optimized global infrastructure, further insulated by a $500 million annual cost-saving restructuring program executed in 2025.

For pure-play leader NASDAQ: ILMN, the legacy "razor-and-blades" model remains highly defensive. Consumables represent 73.7% of total sequencing revenue ($2.93 billion), driving an elite human capital yield of $502,080 revenue per employee. Furthermore, Illumina's balance sheet is highly insulated from the "higher-for-longer" rate environment; management intelligently locked in a 4.75% fixed rate on a $500 million 2030 note, pushing its interest coverage ratio (ICR) to a fortress-like 8.0x.

Conversely, SHA: 688114 is absorbing the margin penalty of a hyper-aggressive land-grab phase. MGI Tech's revenue per employee sits at a depressed $176,186, burdened by a bloated 41.3% total SG&A ratio necessary to maintain a global commercial footprint on a $386.73 million top line. Despite posting a net loss of -$30.91 million, MGI engineered a positive OCF of +$30.47 million strictly through aggressive receivables collection. However, forensic red flags exist: MGI’s Days Sales Outstanding (DSO) remains perilously high at 189 days, and the company aggressively inflated its R&D capitalization rate from 7.98% in 2024 to 11.67% in 2025, artificially padding its operating bottom line compared to ILMN and TMO, which strictly expense 100% of R&D as incurred.

Comparative Resilience Under Geopolitical Decoupling

The strategic imperative has shifted from raw high-throughput capacity to supply chain redundancy and platform interoperability.

NASDAQ: ILMN defends its moat via ecosystem lock-in, tightly coupling its XLEAP-SBS chemistry with the DRAGEN Bio-IT downstream informatics platform. However, the company faces elevated inventory obsolescence risk. The rollout of the production-scale NovaSeq X and the benchtop MiSeq i100 (featuring room-temperature reagents) inherently cannibalizes legacy platforms, forcing continuous inventory write-downs. Furthermore, Illumina's COGS structure remains uniquely vulnerable to supply chain shocks due to its reliance on single-source suppliers for critical precision mechanical and fluidic components.

SHA: 688114 is executing a high-risk, high-reward "Full-Read" (SEQ ALL) matrix. MGI's moat relies on combining short-read DNBSEQ tech with its emerging CycloneSEQ nanopore platform (unmasked in litigation footnotes as the stealth WT02 project). Faced with an impenetrable Western geopolitical wall, MGI executed a brilliant "License-out" maneuver. By selling its U.S. subsidiary Complete Genomics to Swiss Rockets AG for ~$50 million, MGI secured milestone and royalty streams for its CoolMPS and StandardMPS chemistries, monetizing Western markets without triggering direct regulatory backlash. MGI further secures its COGS through deep vertical integration, insourcing specialized upstream enzymes while strategically outsourcing low-value mechanical components.

NYSE: TMO operates an unmatched pan-laboratory ecosystem. By acquiring Olink Holding AB, Thermo Fisher bridges the gap between mass spectrometry and next-generation proteomics. Unlike the pure-play hardware manufacturers, Thermo's hybrid manufacturing model—mixing self-manufactured and third-party contract manufacturing—creates distinct tariff and macroeconomic exposure, which the firm actively mitigates via an aggressive multi-currency debt hedging strategy spanning USD, EUR, JPY, and CHF.

To navigate draconian data sovereignty mandates (e.g., GDPR, China’s Cybersecurity Law), technological architectures are fracturing. While Illumina relies on its centralized Illumina Connected Analytics cloud, MGI is forced into hardware isolation, utilizing offline-capable instruments and deploying its Zhi Ku Yun Shu federated learning platform to ensure no cross-border genomic data leakage.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase characterized by conflicting forward indicators. Management outlooks for 2026 are dangerously divergent. While MGI Tech aggressively calls for a return to "double-digit growth" driven by downstream clinical diagnostic approvals, we challenge this hyper-optimism. MGI's 127.6% YoY surge in deferred revenue—heavily padded by one-off licensing upfronts—masks structural volume exhaustion in public procurement.

Conversely, Illumina’s cautious guidance regarding constrained NIH budgets and delayed laboratory CapEx accurately reflects the macroeconomic reality. The fundamental issue is capital redundancy: as all three entities aggressively build out parallel, localized "In Region, For Region" supply chains to satisfy fragmented biosecurity laws, the industry is effectively duplicating capital expenditures without expanding the total addressable market. Consequently, we anticipate a structural margin squeeze and depressed return on invested capital (ROIC) across the broader peer group through 2H2026.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure NGS Industry Benchmark Matrix 2025

Free Cash Flow Conversion and Unit Economic FracturesA forensic audit of FY2025 financial disclosures reveals severe structural fractures in operating leverage and capital allocation across the cohort.

NYSE: TMO exhibits best-in-class economies of scale, generating a massive 1.17x Operating Cash Flow (OCF) to Net Income conversion rate ($7.81 billion OCF against $6.70 billion net income). Its sub-20% SG&A ratio confirms an optimized global infrastructure, further insulated by a $500 million annual cost-saving restructuring program executed in 2025.

For pure-play leader NASDAQ: ILMN, the legacy "razor-and-blades" model remains highly defensive. Consumables represent 73.7% of total sequencing revenue ($2.93 billion), driving an elite human capital yield of $502,080 revenue per employee. Furthermore, Illumina's balance sheet is highly insulated from the "higher-for-longer" rate environment; management intelligently locked in a 4.75% fixed rate on a $500 million 2030 note, pushing its interest coverage ratio (ICR) to a fortress-like 8.0x.

Conversely, SHA: 688114 is absorbing the margin penalty of a hyper-aggressive land-grab phase. MGI Tech's revenue per employee sits at a depressed $176,186, burdened by a bloated 41.3% total SG&A ratio necessary to maintain a global commercial footprint on a $386.73 million top line. Despite posting a net loss of -$30.91 million, MGI engineered a positive OCF of +$30.47 million strictly through aggressive receivables collection. However, forensic red flags exist: MGI’s Days Sales Outstanding (DSO) remains perilously high at 189 days, and the company aggressively inflated its R&D capitalization rate from 7.98% in 2024 to 11.67% in 2025, artificially padding its operating bottom line compared to ILMN and TMO, which strictly expense 100% of R&D as incurred.

Comparative Resilience Under Geopolitical Decoupling

The strategic imperative has shifted from raw high-throughput capacity to supply chain redundancy and platform interoperability.

NASDAQ: ILMN defends its moat via ecosystem lock-in, tightly coupling its XLEAP-SBS chemistry with the DRAGEN Bio-IT downstream informatics platform. However, the company faces elevated inventory obsolescence risk. The rollout of the production-scale NovaSeq X and the benchtop MiSeq i100 (featuring room-temperature reagents) inherently cannibalizes legacy platforms, forcing continuous inventory write-downs. Furthermore, Illumina's COGS structure remains uniquely vulnerable to supply chain shocks due to its reliance on single-source suppliers for critical precision mechanical and fluidic components.

SHA: 688114 is executing a high-risk, high-reward "Full-Read" (SEQ ALL) matrix. MGI's moat relies on combining short-read DNBSEQ tech with its emerging CycloneSEQ nanopore platform (unmasked in litigation footnotes as the stealth WT02 project). Faced with an impenetrable Western geopolitical wall, MGI executed a brilliant "License-out" maneuver. By selling its U.S. subsidiary Complete Genomics to Swiss Rockets AG for ~$50 million, MGI secured milestone and royalty streams for its CoolMPS and StandardMPS chemistries, monetizing Western markets without triggering direct regulatory backlash. MGI further secures its COGS through deep vertical integration, insourcing specialized upstream enzymes while strategically outsourcing low-value mechanical components.

NYSE: TMO operates an unmatched pan-laboratory ecosystem. By acquiring Olink Holding AB, Thermo Fisher bridges the gap between mass spectrometry and next-generation proteomics. Unlike the pure-play hardware manufacturers, Thermo's hybrid manufacturing model—mixing self-manufactured and third-party contract manufacturing—creates distinct tariff and macroeconomic exposure, which the firm actively mitigates via an aggressive multi-currency debt hedging strategy spanning USD, EUR, JPY, and CHF.

To navigate draconian data sovereignty mandates (e.g., GDPR, China’s Cybersecurity Law), technological architectures are fracturing. While Illumina relies on its centralized Illumina Connected Analytics cloud, MGI is forced into hardware isolation, utilizing offline-capable instruments and deploying its Zhi Ku Yun Shu federated learning platform to ensure no cross-border genomic data leakage.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase characterized by conflicting forward indicators. Management outlooks for 2026 are dangerously divergent. While MGI Tech aggressively calls for a return to "double-digit growth" driven by downstream clinical diagnostic approvals, we challenge this hyper-optimism. MGI's 127.6% YoY surge in deferred revenue—heavily padded by one-off licensing upfronts—masks structural volume exhaustion in public procurement.

Conversely, Illumina’s cautious guidance regarding constrained NIH budgets and delayed laboratory CapEx accurately reflects the macroeconomic reality. The fundamental issue is capital redundancy: as all three entities aggressively build out parallel, localized "In Region, For Region" supply chains to satisfy fragmented biosecurity laws, the industry is effectively duplicating capital expenditures without expanding the total addressable market. Consequently, we anticipate a structural margin squeeze and depressed return on invested capital (ROIC) across the broader peer group through 2H2026.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*