Corheart Medical Advances $169M STAR Market IPO as 74.8% Gross Margin Signals Sustainable Import Substitution in China

Date : 2026-05-01

Reading : 83

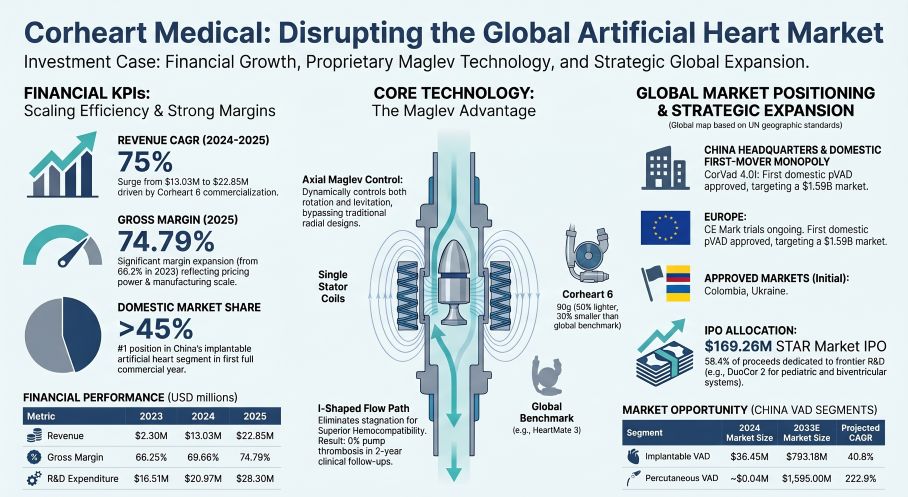

Corheart Medical’s 2025 disclosures reveal a hyper-growth trajectory, driven by the Shenzhen-based commercialization of the Corheart® 6 LVAD. Capturing over 45% domestic market share and displacing NYSE: ABT, the firm posted $22.85M in 2025 revenue. Yet, to circumvent geopolitical IP thickets dominated by NYSE: JNJ, Corheart is burning $1.66M monthly on localized R&D. The planned $169.25M STAR Market IPO is a critical capital bridge, necessary to fund its localized supply chain and navigate China’s impending Volume-Based Procurement (VBP) pricing caps.

Figure Corheart Medical: Disrupting the Global Artificial Heart Market

Operating Leverage & Unit Economics

Operating Leverage & Unit Economics

An audit of Corheart Medical’s pre-IPO financials reveals a stark dichotomy between robust top-line execution and fundamentally negative Free Cash Flow (FCF) conversion. Operating revenue grew 75.33% YoY in 2025 to $22.85M, driven entirely by the Corheart® 6 adoption curve. Scaling production efficiency expanded gross margins from 66.25% in 2023 to 74.79% in 2025.

However, a forensic look at the price-mix variance indicates underlying unit economic pressures. The Average Selling Price (ASP) contracted from $40,403 in 2023 to $33,419 in 2025. While management attributes this to strategic tier-discounting for centralized platform distributors, it limits gross profit generation ($17.09M) against a staggering $41.83M combined SG&A and R&D outlay.

Consequently, the path to profitability remains structurally delayed until at least 2030. Net margins sit at -104.92%, with a 2025 operating cash burn of $19.90M. The proposed $169.25M capital raise is an absolute liquidity imperative to stretch the current 3.2-year cash runway. Capital allocation is heavily skewed toward long-term asset accumulation, with $19.39M earmarked for a Shenzhen industrialization base capable of 4,100 annual mixed-device units, and $98.93M strictly ring-fenced for frontier pipeline R&D.

Supply Chain Localization & IP Architecture

Corheart’s R&D-to-Moat translation is the core driver of its enterprise value. The company has aggressively bypassed the radial magnetic levitation patents of NYSE: ABT (HeartMate 3) via an internationally original "time-sharing partitioned dynamic axial full magnetic levitation" technology. This architectural shift yielded the 90g Corheart® 6—roughly 50% lighter than global peers—establishing an exclusive domestic monopoly in pediatric LVAD indications. In the short-term percutaneous VAD (pVAD) market, the December 2025 approval of CorVad® 4.0 effectively breaks the domestic stranglehold of NYSE: JNJ (Abiomed’s Impella) using a proprietary miniaturized intravascular motor.

From a supply chain perspective, Corheart exhibits zero direct exposure to geopolitical feedstock disruptions. Procurement is hyper-localized; 100% of the top five suppliers for the $11.21M FY25 materials spend are mainland China entities (e.g., Shenzhen Jingzhu Mold). By vertically integrating core micro-machining and fluid dynamics while outsourcing low-value titanium casing and PCB placement (16.83% of procurement), the firm maintains a highly resilient, cost-pass-through efficient operational base.

HDIN Institutional Perspective

While management projects profitability by the end of the decade, the underlying unit economics suggest severe vulnerability to China's DRG and VBP frameworks. The ASP degradation from $40,403 to $33,419 in just 24 months—framed as a "distributor shift"—masks the structural reality that Corheart lacks long-term pricing power in a single-payer system. Furthermore, deploying nearly 60% of IPO proceeds into frontier R&D for the DuoCor® 2 biventricular system, rather than accelerating commercialization pathways for existing lines, risks deepening the $19.9M annual cash burn if domestic hospital admission rates stall. The firm has engineered a brilliant technological moat, but its financial architecture remains acutely fragile.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure Corheart Medical: Disrupting the Global Artificial Heart Market

Operating Leverage & Unit EconomicsAn audit of Corheart Medical’s pre-IPO financials reveals a stark dichotomy between robust top-line execution and fundamentally negative Free Cash Flow (FCF) conversion. Operating revenue grew 75.33% YoY in 2025 to $22.85M, driven entirely by the Corheart® 6 adoption curve. Scaling production efficiency expanded gross margins from 66.25% in 2023 to 74.79% in 2025.

However, a forensic look at the price-mix variance indicates underlying unit economic pressures. The Average Selling Price (ASP) contracted from $40,403 in 2023 to $33,419 in 2025. While management attributes this to strategic tier-discounting for centralized platform distributors, it limits gross profit generation ($17.09M) against a staggering $41.83M combined SG&A and R&D outlay.

Consequently, the path to profitability remains structurally delayed until at least 2030. Net margins sit at -104.92%, with a 2025 operating cash burn of $19.90M. The proposed $169.25M capital raise is an absolute liquidity imperative to stretch the current 3.2-year cash runway. Capital allocation is heavily skewed toward long-term asset accumulation, with $19.39M earmarked for a Shenzhen industrialization base capable of 4,100 annual mixed-device units, and $98.93M strictly ring-fenced for frontier pipeline R&D.

Supply Chain Localization & IP Architecture

Corheart’s R&D-to-Moat translation is the core driver of its enterprise value. The company has aggressively bypassed the radial magnetic levitation patents of NYSE: ABT (HeartMate 3) via an internationally original "time-sharing partitioned dynamic axial full magnetic levitation" technology. This architectural shift yielded the 90g Corheart® 6—roughly 50% lighter than global peers—establishing an exclusive domestic monopoly in pediatric LVAD indications. In the short-term percutaneous VAD (pVAD) market, the December 2025 approval of CorVad® 4.0 effectively breaks the domestic stranglehold of NYSE: JNJ (Abiomed’s Impella) using a proprietary miniaturized intravascular motor.

From a supply chain perspective, Corheart exhibits zero direct exposure to geopolitical feedstock disruptions. Procurement is hyper-localized; 100% of the top five suppliers for the $11.21M FY25 materials spend are mainland China entities (e.g., Shenzhen Jingzhu Mold). By vertically integrating core micro-machining and fluid dynamics while outsourcing low-value titanium casing and PCB placement (16.83% of procurement), the firm maintains a highly resilient, cost-pass-through efficient operational base.

HDIN Institutional Perspective

While management projects profitability by the end of the decade, the underlying unit economics suggest severe vulnerability to China's DRG and VBP frameworks. The ASP degradation from $40,403 to $33,419 in just 24 months—framed as a "distributor shift"—masks the structural reality that Corheart lacks long-term pricing power in a single-payer system. Furthermore, deploying nearly 60% of IPO proceeds into frontier R&D for the DuoCor® 2 biventricular system, rather than accelerating commercialization pathways for existing lines, risks deepening the $19.9M annual cash burn if domestic hospital admission rates stall. The firm has engineered a brilliant technological moat, but its financial architecture remains acutely fragile.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*