Global EDA Structural Bifurcation: NASDAQ: SNPS and NASDAQ: CDNS Diverge from APAC Challengers on Subscription Cash Conversion as $383K Revenue-Per-Employee Defines 2026 Outlook

Date : 2026-05-04

Reading : 414

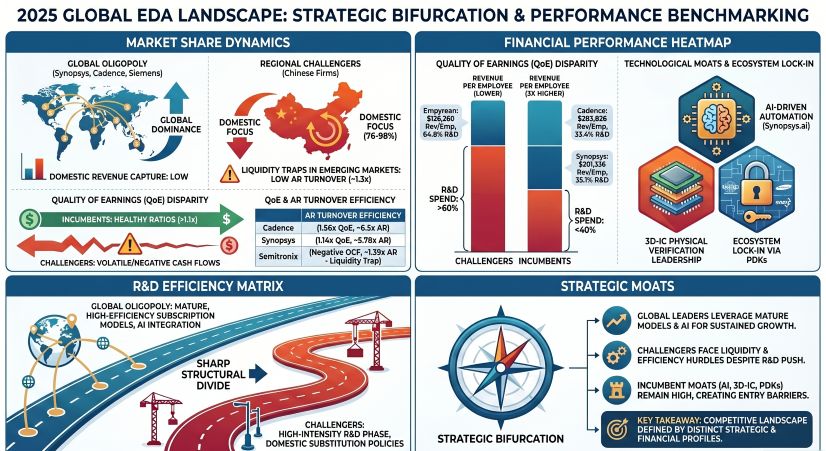

The 2025 global EDA sector exhibits a severe liquidity and margin polarization. While NASDAQ: CDNS and NASDAQ: SNPS monetize AI-driven hardware emulation (Palladium/ZeBu) to achieve exceptional 1.14x operating cash flow conversions, Chinese domestic providers like SZSE: 301095 (Semitronix) face catastrophic accounts receivable bloat, trapping 92% of 2025 revenue. This working capital divergence is catalyzed by US BIS export restrictions under ECCNs 3D991/3E991, which simultaneously force heavy APAC localized R&D build-outs but leave domestic challengers exposed to intense counterparty credit risks from regional Tier-2 foundries.

Figure 2025 GLOBAL EDA LANDSCAPE: STRATEGIC BIFURCATION & PERFORMANCE BENCHMARKING

Operating Leverage and the Quality of Earnings Disconnect

Operating Leverage and the Quality of Earnings Disconnect

The unit economics of the EDA oligopoly highlight massive scale advantages and structural leverage. NASDAQ: CDNS generates an industry-leading $383,826 in revenue per employee, underpinned by a 1.56x Quality of Earnings (QoE) ratio and a $934.4M deferred revenue backlog. NASDAQ: SNPS similarly leverages its $34.9B Ansys integration to achieve a 42.0% segment operating margin and a pristine 1.14x QoE. Both firms optimize capital structures by absorbing debt (e.g., NASDAQ: SNPS carrying an elevated 47.6% D/E ratio) to finance M&A, shielded by multi-billion-dollar recurring cash flows.

In stark contrast, Chinese domestic firms are sacrificing operating leverage to aggressively fund organic R&D. SZSE: 301269 (Empyrean) and SSE: 688206 (Primarius) deploy extreme R&D-to-revenue intensities of 64.84% ($119.5M) and 67.48% ($45.4M) respectively. However, this hyper-investment lacks near-term cash realization. SZSE: 301095 (Semitronix) exemplifies this margin squeeze, posting a $12.34M net profit against a negative -$16.94M operating cash flow, driven by a plummeting Accounts Receivable (AR) turnover ratio of 1.39x. This divergence indicates an unsustainable reliance on paper profits, subsidized by lenient credit terms offered to domestic foundries rather than sticky Software-as-a-Service (SaaS) cash cycles.

Ecosystem Lock-In and Export Control Vulnerabilities

Comparative resilience across the sector is dictated by geographic revenue exposure and foundry ecosystem integration. The U.S. incumbents maintain impenetrable moats via Design Technology Co-Optimization (DTCO) with top-tier global foundries (TSMC, Samsung, Intel) to optimize their Synopsys.ai and Intelligent System Design (ISD) platforms. However, geopolitical exposure remains their primary systemic vulnerability. NASDAQ: CDNS incurred a $140.6M penalty to the DOJ/BIS for unauthorized technology transfers, while NASDAQ: SNPS faces ongoing administrative subpoenas, structurally capping their Total Addressable Market (TAM) in APAC.

Conversely, domestic challengers operate within a highly localized closed-loop ecosystem. SZSE: 301269 (Empyrean) commands customized Process Design Kits (PDKs) covering >70% of Mainland China’s manufacturing nodes, shielding its $184.3M top-line from international competition. Yet, these firms exhibit fragile cash-conversion cycles and virtually zero subscription moats. While NASDAQ: SNPS boasts $2.62B in unearned deferred revenue locking in future cash flows, Chinese pure-plays rely heavily on milestone-based hardware sales and upfront technical consulting (e.g., Cellixsoft deriving 95.2% of its $34.50M revenue from project-based IC Analysis/Design). This structural discrepancy leaves the domestic cohort hyper-exposed to single-client budget contractions during localized semiconductor cycle downturns.

HDIN Institutional Perspective

The global EDA sector is entering a 'trough-discovery' phase regarding regional credit risks, disguised by AI-induced top-line euphoria. While NASDAQ: CDNS and NASDAQ: SNPS signal robust cycle resilience through AI-augmented digital twins (Millennium Multiphysics) and massive deferred revenue reserves, the aggressive R&D capitalization and exploding AR overhang among APAC challengers suggest an impending 2026 liquidity squeeze for the domestic group. The assumption that state-backed domestic substitution initiatives guarantee operational health is fundamentally flawed; without monopolistic pricing power and enforced 30-to-60-day payment terms, the Chinese EDA cohort is effectively financing the working capital of domestic foundries at the direct expense of their own balance sheet integrity.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 GLOBAL EDA LANDSCAPE: STRATEGIC BIFURCATION & PERFORMANCE BENCHMARKING

Operating Leverage and the Quality of Earnings DisconnectThe unit economics of the EDA oligopoly highlight massive scale advantages and structural leverage. NASDAQ: CDNS generates an industry-leading $383,826 in revenue per employee, underpinned by a 1.56x Quality of Earnings (QoE) ratio and a $934.4M deferred revenue backlog. NASDAQ: SNPS similarly leverages its $34.9B Ansys integration to achieve a 42.0% segment operating margin and a pristine 1.14x QoE. Both firms optimize capital structures by absorbing debt (e.g., NASDAQ: SNPS carrying an elevated 47.6% D/E ratio) to finance M&A, shielded by multi-billion-dollar recurring cash flows.

In stark contrast, Chinese domestic firms are sacrificing operating leverage to aggressively fund organic R&D. SZSE: 301269 (Empyrean) and SSE: 688206 (Primarius) deploy extreme R&D-to-revenue intensities of 64.84% ($119.5M) and 67.48% ($45.4M) respectively. However, this hyper-investment lacks near-term cash realization. SZSE: 301095 (Semitronix) exemplifies this margin squeeze, posting a $12.34M net profit against a negative -$16.94M operating cash flow, driven by a plummeting Accounts Receivable (AR) turnover ratio of 1.39x. This divergence indicates an unsustainable reliance on paper profits, subsidized by lenient credit terms offered to domestic foundries rather than sticky Software-as-a-Service (SaaS) cash cycles.

Ecosystem Lock-In and Export Control Vulnerabilities

Comparative resilience across the sector is dictated by geographic revenue exposure and foundry ecosystem integration. The U.S. incumbents maintain impenetrable moats via Design Technology Co-Optimization (DTCO) with top-tier global foundries (TSMC, Samsung, Intel) to optimize their Synopsys.ai and Intelligent System Design (ISD) platforms. However, geopolitical exposure remains their primary systemic vulnerability. NASDAQ: CDNS incurred a $140.6M penalty to the DOJ/BIS for unauthorized technology transfers, while NASDAQ: SNPS faces ongoing administrative subpoenas, structurally capping their Total Addressable Market (TAM) in APAC.

Conversely, domestic challengers operate within a highly localized closed-loop ecosystem. SZSE: 301269 (Empyrean) commands customized Process Design Kits (PDKs) covering >70% of Mainland China’s manufacturing nodes, shielding its $184.3M top-line from international competition. Yet, these firms exhibit fragile cash-conversion cycles and virtually zero subscription moats. While NASDAQ: SNPS boasts $2.62B in unearned deferred revenue locking in future cash flows, Chinese pure-plays rely heavily on milestone-based hardware sales and upfront technical consulting (e.g., Cellixsoft deriving 95.2% of its $34.50M revenue from project-based IC Analysis/Design). This structural discrepancy leaves the domestic cohort hyper-exposed to single-client budget contractions during localized semiconductor cycle downturns.

HDIN Institutional Perspective

The global EDA sector is entering a 'trough-discovery' phase regarding regional credit risks, disguised by AI-induced top-line euphoria. While NASDAQ: CDNS and NASDAQ: SNPS signal robust cycle resilience through AI-augmented digital twins (Millennium Multiphysics) and massive deferred revenue reserves, the aggressive R&D capitalization and exploding AR overhang among APAC challengers suggest an impending 2026 liquidity squeeze for the domestic group. The assumption that state-backed domestic substitution initiatives guarantee operational health is fundamentally flawed; without monopolistic pricing power and enforced 30-to-60-day payment terms, the Chinese EDA cohort is effectively financing the working capital of domestic foundries at the direct expense of their own balance sheet integrity.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*